Single-family mortgage originations are projected to hit $2.2 trillion in 2026, an 8% increase over 2025. That growth isn't evenly distributed. The lenders capturing it are the ones whose systems process loans faster, with fewer errors, at lower cost per file.

The difference between a 30-day close and a 45-day close isn't staff size. It's how well your data moves between systems. When your loan origination system, customer relationship management platform, pricing engine, and compliance tools share data automatically, every loan moves faster. When they don't, your team fills the gaps with manual work that slows everything down.

This article covers the three pillars of mortgage operational efficiency: data optimization, software integration, and the technology architecture that ties them together. It also covers how Access Business Technologies pulls those three pillars into one connected stack for the 750+ financial institutions whose Microsoft 365 tenants we manage, using MortgageExchange for the data layer, Mortgage BI for visibility, MortgageWorkSpace for the daily working environment, and M365 Guardian for the security and governance posture that examiners actually grade.

In This Article

Data Optimization: The Foundation

Clean Data Starts at Intake

Every data quality problem in your pipeline started at intake. A misspelled name. An income figure entered without cents. An address that doesn't match the credit report. These small errors cascade through your operation, triggering condition requests, disclosure amendments, and closing delays.

Data optimization means catching these issues at the point of entry. Validation rules on your borrower portal reject incomplete applications before they reach your processor. Field-level checks compare entered data against credit bureau records in real time.

Eliminate Duplicate Records

Most mortgage lenders have duplicate borrower records scattered across their loan origination system, customer relationship management platform, and servicing platforms. The same borrower exists as three different entries because each system created its own record independently.

Deduplication tools match records across systems using Social Security numbers, phone numbers, and email addresses. Clean records mean accurate reporting, better compliance, and a borrower experience that doesn't ask the same questions twice.

Standardize Data Formats

MISMO (Mortgage Industry Standards Maintenance Organization) defines the standard data formats for mortgage lending. When your systems use MISMO-compliant formats, data moves between platforms without transformation errors. For ABT's fuller take, see From Chaos to Clarity.

Non-standard formats require custom mapping for every connection. That mapping breaks when either system updates. MISMO compliance prevents this problem.

Integration Architecture: Connecting Your Stack

The Centralized LOS Integration Model

Most mortgage technology stacks work best with a centralized LOS integration model. Your loan origination system sits at the center. Every other system connects to it through APIs. Data flows out from the loan origination system to your customer relationship management platform, compliance engine, and document platform. Updates flow back.

This model works because the loan origination system is already your system of record for loan data. Making it the integration center means every connected system pulls from the same source of truth.

Event-Driven Architecture

Instead of checking for updates on a schedule, event-driven systems push data when something changes. A borrower uploads a document. The system notifies your processor. An appraiser completes a report. The system updates your file and triggers the next workflow step.

Event-driven architecture eliminates polling delays. Your team works with current data instead of information that was accurate 15 minutes ago.

Middleware for Legacy Connections

Not every system in your stack supports modern APIs. Middleware platforms handle the translation between legacy file-based systems and modern API-connected platforms.

Microsoft Azure Logic Apps and mortgage-specific middleware tools handle this translation layer. They monitor connections, retry failed transfers, and log every data exchange for compliance purposes.

Technology Decisions That Affect Every Loan

AI-Powered Document Processing

AI adoption among mortgage lenders jumped from 15% in 2023 to 38% in 2024. The most common deployment: document classification and data extraction. AI reads a W-2, identifies the income fields, and populates your loan origination system. What took a processor 15 minutes happens in seconds.

Lenders using AI document automation increased processing capacity by 3,000 applications per month without adding staff.

Open Banking APIs

Open banking APIs pull income, asset, and employment data directly from borrower financial institutions. No more chasing pay stubs. No more waiting for bank statements to arrive by email. The data flows directly into your verification engine. See also our breakdown of The Mortgage Industry's Best Kept Secret.

Verification time drops from 48 hours to under 4 hours. The data is more accurate because it comes from the source instead of a borrower-submitted PDF.

Automated Underwriting System Connections

Direct API connections to Fannie Mae Desktop Underwriter and Freddie Mac Loan Product Advisor process eligibility decisions in minutes. LPA users who maximize data interface usage see pull-through rates increase by 1.8%.

On a $500M annual production volume, that 1.8% improvement translates to $9M in additional funded loans.

How ABT Connects the Stack: MortgageExchange, Mortgage BI, MortgageWorkSpace, M365 Guardian

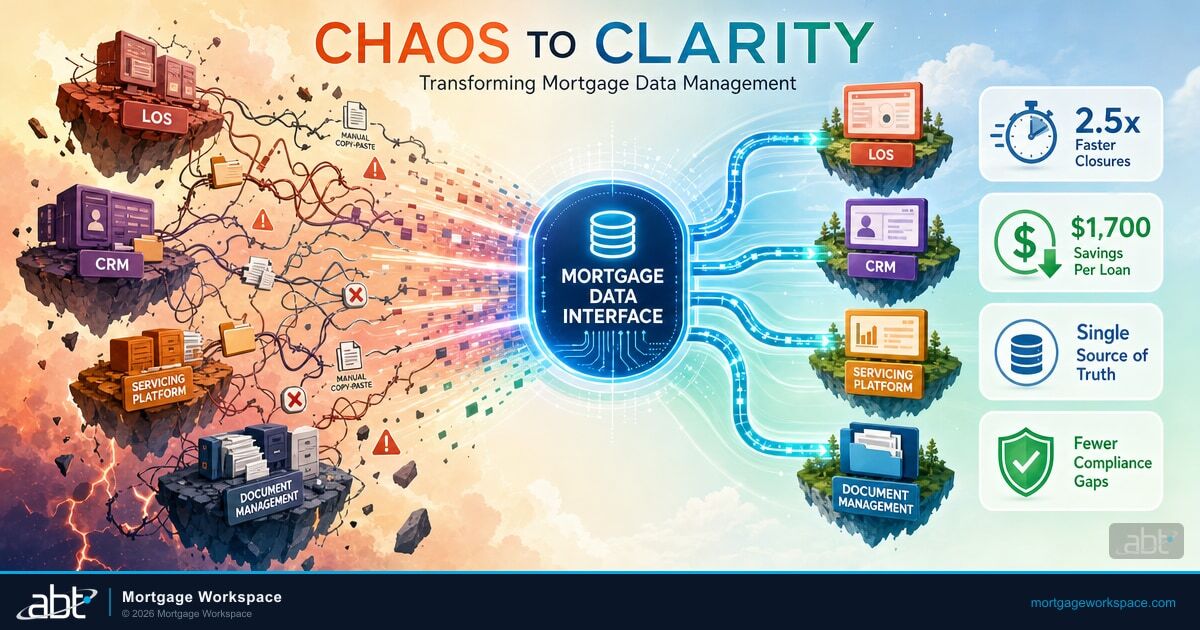

The patterns above describe what good mortgage operations look like in the abstract. The question every lender's COO asks next is who actually does the integration work and keeps it running. For the 750+ financial institutions whose Microsoft 365 tenants Access Business Technologies manages, four ABT products turn those patterns into a connected stack: MortgageExchange is the data optimization and integration layer, Mortgage BI is the visibility layer, MortgageWorkSpace is the daily working environment, and M365 Guardian is the security and governance posture that holds the whole stack to examiner expectations.

MortgageExchange is the data optimization and integration layer. It is the custom interface product that connects the loan origination system to the rest of the stack. MortgageExchange handles the LOS-to-AUS connection that drives Fannie Mae Desktop Underwriter and Freddie Mac Loan Product Advisor pull-through, the LOS-to-servicing handoff that closes the file without rekeying, and the LOS-to-CRM sync that keeps customer relationship management current with what the loan officer is actually working on. The interface is the data optimization layer in practice. It enforces MISMO-compliant formats, deduplicates records across systems, validates fields against credit bureau records, and moves data event-by-event so every connected platform sees the same source of truth without polling delays.

Mortgage BI is the visibility layer, MortgageWorkSpace is the daily working environment, and M365 Guardian is the governance posture. Once the data is moving cleanly through MortgageExchange, the next three questions a lending operation needs answered are who can see what is happening, where the team works, and how the whole footprint stays inside the rules. Mortgage BI is the business intelligence layer that builds dashboards on top of the loan pipeline: cost per loan, days to close, touches per file, error rate, pull-through rate, all read straight from the integrated stack rather than reconciled in spreadsheets. MortgageWorkSpace is the daily working environment for loan officers, processors, underwriters, and closers, the unified Microsoft 365 workspace that ties email, documents, Teams, and the LOS into one place a mortgage team actually uses. M365 Guardian is ABT's operating model on top of the Microsoft tenant, applying the Microsoft Entra ID, Microsoft Defender, Microsoft Purview, Microsoft Intune, and Microsoft Sentinel controls that keep customer non-public personal information protected and the firm's books-and-records evidence ready when an examiner asks for it. Together, the four products give a community bank, credit union, or independent mortgage banker the connected stack the article describes without having to assemble it from four different vendors. This connects closely to Migration Myths Busted.

Measuring the Results

Operational efficiency isn't a feeling. It's measurable. Track these metrics to know if your data optimization and integration investments are working:

- Cost per loan: The industry average is $11,800. Integrated lenders report savings of $1,700 per loan through digital tools and connected systems

- Days to close: Track the average time from application to funded loan. Integration should reduce this by 30-50%

- Touches per file: Count how many times a human touches each loan file. Fewer touches mean better automation

- Error rate: Track conditions requested due to data entry errors. Connected systems with validation rules should reduce this to near zero

- Pull-through rate: Percentage of applications that fund. Higher pull-through means fewer dropped loans and better pipeline management

Mortgage BI builds these metrics into the dashboards a lending operation actually uses. The numbers come straight from the integrated stack rather than a custom report build that takes weeks.

Talk to ABT About Connecting Your Mortgage Stack

MortgageExchange, Mortgage BI, MortgageWorkSpace, and M365 Guardian work together to turn the integration architecture this article describes into a connected operation that closes more loans with fewer errors. ABT manages Microsoft 365 tenants for 750+ financial institutions, including community banks, credit unions, and independent mortgage bankers. A 30-minute conversation maps your current LOS, AUS, servicing, and CRM stack, surfaces the integration gaps that are slowing your time-to-close, and outlines what an ABT-connected deployment would cover. No commitment, no quote, no obligation.

Frequently Asked Questions

Mortgage data optimization is the process of cleaning, standardizing, and connecting loan data across your origination platforms. It includes validation rules at intake, deduplication of borrower records across systems, MISMO-compliant data formatting, and automated quality checks that catch errors before they reach underwriting or closing. ABT's MortgageExchange product is the data optimization and integration layer that connects the loan origination system to the automated underwriting system, servicing platform, and customer relationship management platform so the same source of truth flows across the stack.

Freddie Mac's 2025 cost-to-originate study found that lenders using digital tools and connected systems saved up to $1,700 per loan against the industry average of $11,800. AI document processing increased capacity by 3,000 applications monthly without adding staff. Combined, these improvements deliver measurable cost reductions and revenue growth. Mortgage BI dashboards read those metrics straight from the integrated stack so a lending operation sees cost per loan, days to close, touches per file, and pull-through rate without building custom reports.

MISMO (Mortgage Industry Standards Maintenance Organization) defines standard data formats for the mortgage industry. When your systems use MISMO-compliant formats, data transfers between platforms without transformation errors. Non-standard formats require custom mapping for every connection, which breaks when systems update and creates ongoing maintenance costs. MortgageExchange enforces MISMO-compliant formats at the integration layer so the loan origination system, automated underwriting system, and servicing platform exchange data in a stable format.

Event-driven architecture in mortgage technology means systems push data automatically when changes occur instead of checking for updates on a schedule. When a borrower uploads a document, the system notifies your processor immediately. When an appraisal completes, it triggers the next workflow step. This eliminates polling delays and keeps every team working with current data. MortgageExchange operates on an event-driven model so every connected system in the stack reflects what just happened on the loan rather than what was true 15 minutes ago.

Open banking APIs pull income, asset, and employment data directly from borrower financial institutions into your verification engine. This reduces verification time from 48 hours to under 4 hours. The data is more accurate than borrower-submitted documents because it comes directly from the source financial institution without manual handling.

Access Business Technologies is a Tier-1 Microsoft Cloud Solution Provider that manages Microsoft 365 tenants for more than 750 financial institutions. For mortgage operations specifically, four ABT products connect the stack end-to-end. MortgageExchange is the data optimization and integration layer that connects the loan origination system to the automated underwriting system, servicing platform, and customer relationship management platform. Mortgage BI is the business intelligence layer that builds dashboards on top of the integrated pipeline. MortgageWorkSpace is the daily working environment that ties Microsoft 365 email, documents, Teams, and the loan origination system into one workspace mortgage teams actually use. M365 Guardian is ABT's operating model on top of the Microsoft tenant for security and governance, applying the Microsoft Entra ID, Microsoft Defender, Microsoft Purview, Microsoft Intune, and Microsoft Sentinel controls that keep customer non-public personal information protected and the firm's books-and-records evidence ready for an examiner.