A 2025 financial services cloud migration study found that 78% of organizations rate data migration as very challenging. That number drops fast when lenders work with a partner that has done it hundreds of times for the mortgage industry. Most of the fear around mortgage data migration comes from myths that no longer match reality, especially for lenders running Encompass, Calyx, MortgageBot, or any modern Loan Origination System tied into a core banking platform. The mechanics of moving loan files, borrower records, and integrations are well understood when the partner running the move has migrated 750+ financial institutions before.

In This Article

Cloud-first infrastructure is now a growth requirement for mortgage lenders. A McKinsey survey found cloud adoption can reduce operational costs by up to 30%. For mortgage companies still running on-premise servers, the question is not whether to migrate. It is when, and with whom. This guide breaks down the five most common mortgage data migration myths, replaces each one with what actually happens when the process is planned and executed by an experienced team, and explains the migration spine ABT uses to move mortgage workloads onto Microsoft Azure with MortgageExchange handling the LOS-to-core data flow.

Myth 1: Mortgage Data Migration Is Inherently Risky

This is the myth that stops conversations before they start. IT directors hear migration and immediately picture corrupted loan files, lost borrower records, and compliance violations. The reality is different. A phased migration with validation checkpoints at every stage carries less risk than keeping data on aging servers with expired warranties. Mortgage lenders that follow a structured approach report meaningful improvement in their recovery time objectives once their workloads run inside Microsoft Azure.

What reduces risk in practice:

- Pre-migration data integrity audits that flag inconsistencies before the move

- Parallel running of legacy and Azure-hosted systems during transition

- Automated validation that compares source and destination records field by field

- Rollback plans tested before any production data moves

- MortgageExchange interface contracts validated against the destination LOS and core banking system before cutover

ABT has migrated mortgage data for 750+ financial institutions on Microsoft Azure. The process is repeatable, documented, and tied directly into MortgageExchange so the integrations that depend on the moved data come back online with the data itself. Risk comes from improvising. Structure eliminates it.

Myth 2: Manual Migration Gives You More Control

Some IT teams prefer manual data transfers because they feel in control of every record. The problem is that feeling and reality diverge at scale. A 2025 study of financial cloud migration projects found that 61% of organizations reported significant data quality issues during migration. Most of those issues came from manual processes, including duplicated records, formatting mismatches, and missed entries that nobody caught until weeks later.

Automated migration tools apply consistent validation rules across every record. They do not skip fields at 4 PM on a Friday. They do not transpose digits in a loan number. They do not forget that the loan officer compensation tier changed on the third Tuesday of the prior month.

Where automation beats manual every time:

- Speed: Automated ETL processes handle millions of mortgage records in hours, not weeks

- Accuracy: Field-level validation catches mismatches before they become compliance problems

- Audit trails: Every transformation is logged in Microsoft Purview Audit for regulatory review

- Repeatability: The same process runs identically for test, staging, and production environments hosted on Microsoft Azure

Control does not come from touching every record by hand. It comes from building a process that validates itself, runs the same way every time, and writes its own audit trail.

Myth 3: Every Byte of Legacy Data Must Be Migrated

Mortgage companies accumulate data over decades. Loan files from 2004. Email archives from processors who left in 2012. Duplicate records created when two systems were merged in 2017. Moving all of it to a new environment is like packing every item from a warehouse into a new building without checking what is inside the boxes. You pay for storage, you slow down the migration, and you import data quality problems into a clean system.

A smarter approach uses three categories:

- Migrate: Active loan files, current borrower records, compliance-required documentation

- Archive: Closed loans within the retention window, historical reporting data

- Purge: Duplicate records, data past retention requirements, test files from old system implementations

Data cleansing before migration reduces storage costs and improves system performance. It also simplifies compliance because auditors review what exists in the system. Less clutter means faster audits and cleaner Purview retention policies on the records that actually need to be preserved. We cover Is Your Interface CFPB-Proof? What Mortgage Teams Need to Know About HMD in a companion piece.

Myth 4: Migration Can Be Rushed If You Have the Right Tools

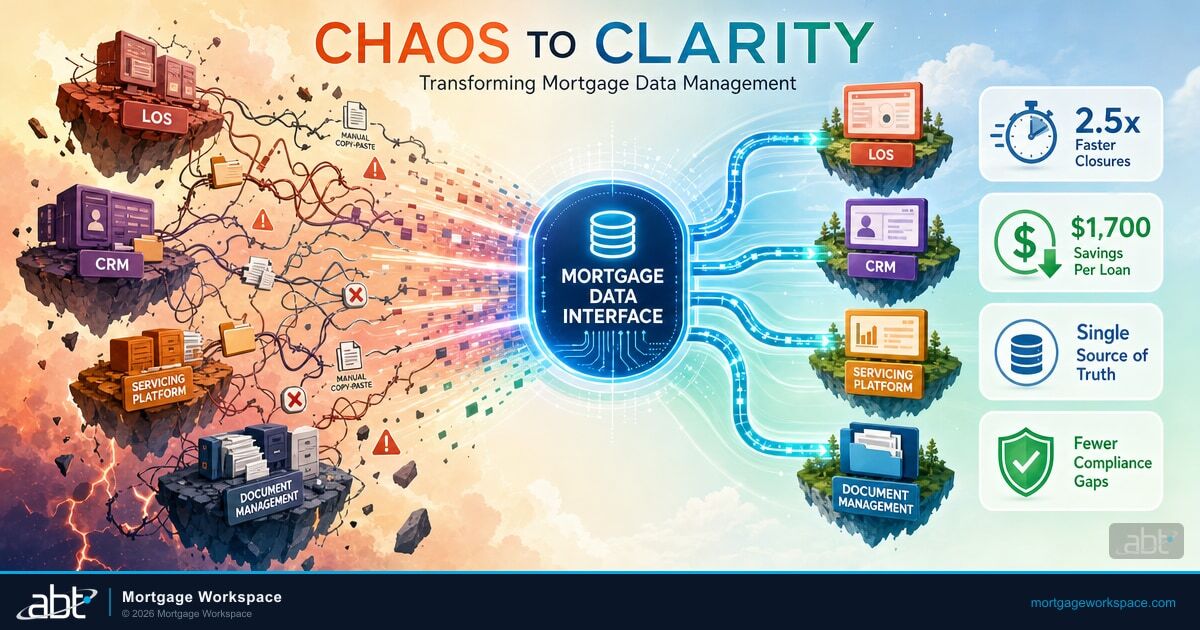

Tools matter. But a three-day migration of a decade of mortgage data will create more problems than it solves. Research on financial services cloud migration found that 86% of successful implementations followed a phased approach. Organizations that attempted to move everything at once spent 42% of their migration budget on application refactoring after the fact. See also our breakdown of From Chaos to Clarity.

A realistic mortgage migration timeline includes:

- Weeks 1-3: Discovery and assessment. Map all data sources, document dependencies, identify compliance requirements.

- Weeks 4-6: Pilot migration. Move a subset of non-critical data to validate the process inside Microsoft Azure.

- Weeks 7-10: Phased production migration. Move data in planned waves with validation between each wave.

- Weeks 11-12: Verification and cutover. Final validation, parallel running, and decommission of legacy systems.

Rushing skips the validation steps that catch problems early. A well-planned 10 to 12 week migration costs less than a botched 3-week attempt followed by months of cleanup.

Myth 5: Migration Happens in the Background Without Affecting Operations

This myth leads to the worst surprises. IT teams tell the business you will not notice anything, and then loan officers cannot access borrower files during a critical funding deadline. Any serious data migration will require some operational adjustments. The difference between a good migration and a bad one is whether those adjustments are planned or discovered in the moment.

How experienced teams manage operational impact:

- Schedule high-volume data moves during off-peak hours, including weekends and evenings

- Maintain read-only access to legacy systems during transition windows

- Set up failover routing so users access backup systems if the primary is unavailable

- Communicate specific timelines to every department before migration windows begin

- Stage MortgageExchange interfaces in dual-write mode so the LOS and core banking system stay in sync during cutover

Cloud-based migration tools with built-in failover can reduce planned downtime to under two hours for most mortgage operations. That is a Saturday morning, not a week of disruption.

What the Real Migration Process Looks Like

Forget the myths. Here is what a mortgage data migration actually involves when it is done by a team that has executed it hundreds of times.

Phase 1: Assessment. Inventory every data source. Document every integration between the Loan Origination System, the core banking platform, the document repository, and the servicing system. Identify every compliance requirement. This phase prevents surprises.

Phase 2: Architecture. Design the target environment on Microsoft Azure. Define data mapping rules. Build and test automated validation. Define how MortgageExchange will carry the LOS-to-core data flow inside the new environment. This phase prevents rework.

Phase 3: Pilot. Migrate a controlled subset. Validate every field. Fix any issues before touching production data. This phase builds confidence.

Phase 4: Execute. Phased production migration with validation between each wave. Parallel running of old and new systems. This phase delivers results.

Phase 5: Verify. Full reconciliation audit. User acceptance testing. Compliance sign-off. Decommission legacy systems. This phase closes the loop.

ABT has refined this process across 750+ financial institutions. Each migration follows a documented playbook that accounts for LOS integrations, compliance data, and the specific regulatory requirements of the mortgage industry. Our guide to The Secret to Effective Mortgage Operations goes deeper on this.

Productivity is the unlock. Audit readiness is the byproduct. Both show up on the same migration plan.

The Microsoft Azure + MortgageExchange Spine for Mortgage Workloads

For mortgage lenders, the move is not just to a generic cloud. It is to a Microsoft Azure environment that ABT hosts under the customer's own subscription and that ABT runs as the partner of record. Azure is where the lender's mortgage workloads live after the move, including the LOS database, document repositories, reporting warehouses, and any custom-built application that was previously stuck on aging on-premise hardware. ABT designs the Azure tenancy, sizes the compute and storage to match the lender's actual loan volume, configures the network and identity controls, and runs the environment as the operating partner. MortgageExchange is the data spine inside that environment. It is the custom interface layer ABT built specifically to move mortgage data between Loan Origination Systems and core banking platforms, with field-level mapping that already knows how Encompass talks to Fiserv DNA, how Calyx talks to Symitar Episys, and how MortgageBot talks to Jack Henry. The combination matters because most mortgage migrations fail not on the data move itself but on the integrations the data was feeding. Azure carries the workloads. MortgageExchange carries the integrations. Together they are the path mortgage lenders take when they want the move done once, validated end to end, and ready to run.

How ABT Manages the Tenant and Governs the Migration

ABT is a Tier-1 Microsoft Direct-Bill Cloud Solution Provider that manages Microsoft 365 tenants for 750+ financial institutions. The Direct-Bill designation means ABT transacts directly with Microsoft, holds dedicated support engineers, and is operationally accountable to Microsoft for how customer tenants are configured. For a mortgage lender moving to the cloud, that distinction matters because the migration sits on top of identity, device, and compliance controls inside Microsoft 365 that have to be configured correctly before any data moves. ABT manages those controls under delegated administration. ABT does not host Microsoft 365, because Microsoft does. ABT manages the tenant. The lender keeps tenant ownership and the regulatory relationships. The combination on top of the Azure environment is what ABT calls M365 Guardian, the operating model for the Microsoft Entra ID, Microsoft Purview, Microsoft Defender, Microsoft Intune, and Microsoft Sentinel stack that protects mortgage data once it lands in the cloud and produces the audit evidence that regulators and investors will ask for. Guardian governs the migration the same way it governs steady-state operations, with Conditional Access policies enforced during the cutover, Purview retention bound to the moved records at the moment they arrive, Defender detections active across the new environment, and Sentinel keeping the incident timeline if anything anomalous happens during the cutover window. For 750+ financial institutions, including community banks, credit unions, mortgage companies, and broker-dealers, that is the operating model that has produced repeatable, low-disruption migrations.

Get a Mortgage Migration Readiness Review

ABT runs the Microsoft Azure migration and MortgageExchange interface pattern described in this article for mortgage lenders moving from on-premise systems to a cloud environment that connects the Loan Origination System to the core banking platform. A 30-minute conversation maps your current environment, surfaces the integrations that need to be carried through the move, and outlines the timeline, validation steps, and operating model the move would follow. No commitment, no quote, no obligation.

Key Takeaway

Mortgage data migration is repeatable when the partner running the move has done it hundreds of times. The combination of Microsoft Azure as the hosted environment, MortgageExchange as the integration spine between the Loan Origination System and the core banking platform, M365 Guardian as the operating model on top of Microsoft Entra ID, Purview, Defender, Intune, and Sentinel, and Tier-1 Microsoft Direct-Bill Cloud Solution Provider status for the partner relationship, is the path mortgage lenders take when they want the move done once, validated end to end, and ready to run. ABT runs that path for 750+ financial institutions.

Frequently Asked Questions

Most mortgage data migrations take 10 to 12 weeks from initial assessment through final verification when the target environment is a Microsoft Azure tenancy and the integrations move through MortgageExchange. The timeline depends on the volume of loan files, the number of source systems, and regulatory requirements. Phased approaches with validation checkpoints between each wave reduce risk and produce better outcomes than compressed timelines.

Compliance data receives the highest priority during migration. Automated validation confirms that every regulated record transfers accurately with full audit trails. Encryption protects data in transit and at rest inside Microsoft Azure. Microsoft Purview retention policies bind to the moved records when they arrive in the new environment, so regulatory retention schedules are continuous through the cutover and the firm's compliance posture does not have a gap.

Yes. Phased migrations schedule high-volume data moves during off-peak hours and maintain read-only access to legacy systems during transition windows. MortgageExchange runs in dual-write mode during cutover so the Loan Origination System and the core banking system stay in sync. Failover routing keeps users connected to backup systems if the primary is temporarily unavailable. Most mortgage operations experience less than two hours of planned downtime per migration wave.

No. A data cleansing phase before migration identifies records to migrate, archive, or purge. Active loan files and compliance-required documents move to the new Microsoft Azure environment. Closed loans within retention windows go to cost-effective archive storage. Duplicate records and data past retention requirements get purged, reducing storage costs and producing cleaner Microsoft Purview retention policies on the records that actually need to be preserved.

ABT manages the Microsoft 365 tenant under delegated administration. Microsoft owns the Microsoft 365 infrastructure and hosts the service. ABT, as a Tier-1 Microsoft Direct-Bill Cloud Solution Provider, configures, monitors, and runs the customer's tenant under that delegated relationship. For the Microsoft Azure side, ABT hosts the lender's Azure environment, meaning the subscription is customer-controlled cloud infrastructure that ABT operates as the partner of record. The combined statement is straightforward: ABT manages your Microsoft 365 tenant and hosts your Azure environment.

MortgageExchange is the custom interface ABT built to move data between Loan Origination Systems and core banking platforms. It already knows how Encompass talks to Fiserv DNA, how Calyx talks to Symitar Episys, and how MortgageBot talks to Jack Henry, with field-level mapping that has been refined across hundreds of mortgage deployments. During a migration, MortgageExchange runs the LOS-to-core data flow inside the new Microsoft Azure environment so the integrations that depend on the moved data come back online with the data itself. Most mortgage migrations fail not on the data move itself but on the integrations the data was feeding. MortgageExchange is how ABT eliminates that failure mode.