In This Article

Fannie Mae's Desktop Underwriter API now processes eligibility decisions in under 10 minutes. That single integration cut what used to take days down to seconds. If your mortgage operation still relies on manual handoffs between disconnected systems, you're losing deals to competitors who don't.

API-driven mortgage software connects your LOS, CRM, pricing engine, and compliance tools into one continuous data flow. No re-keying. No waiting. No hoping someone didn't fat-finger a Social Security number.

Here's how mortgage lenders are using APIs to build faster, more accurate client experiences in 2026.

What Is API-Driven Mortgage Software?

An API (Application Programming Interface) lets two software systems exchange data without human intervention. In mortgage lending, APIs connect your loan origination system to credit bureaus, document platforms, pricing engines, and compliance databases. This connects closely to Breaking Down Barriers.

Instead of exporting a file from one system and importing it into another, an API transfers that data in real time. A borrower uploads income verification to your portal. The API sends that document to your underwriting platform within seconds. No manual upload. No duplicate entry. Our guide to Scaling Pains or Scaling Gains? IT Metrics That Predict Mortgage Growth goes deeper on this.

ICE Mortgage Technology moved its entire Encompass platform to API-first architecture in 2025, replacing legacy SDK integrations with Developer Connect and Partner Connect APIs. That shift signals where the industry is heading: open, connected, automated.

Integration products like MortgageExchange are built on this foundation, connecting LOS platforms to core banking systems, CRMs, and compliance tools through standardized API layers. Instead of building custom connections from scratch, lenders plug into a pre-built integration framework that handles data mapping, validation, and error recovery.

Five Ways APIs Improve Mortgage Operations

1. Faster Loan Processing

Lenders using AI-powered APIs report 2.5x faster loan closures compared to industry averages. Cloudvirga's API platform generates underwriter-ready loan files in under 10 minutes. That speed translates to more closed loans per month with the same staff.

When your pricing engine, AUS, and doc prep system all talk through APIs, the time between application and clear-to-close shrinks from weeks to days.

2. Fewer Data Entry Errors

Manual re-keying is the top source of mortgage data errors. A single transposed digit in an income figure can trigger a compliance flag, delay closing, or produce an inaccurate disclosure.

APIs eliminate re-keying by passing validated data directly between systems. Freddie Mac's Loan Product Advisor (LPA) uses API-connected data to reduce non-acceptable quality rates by 40% among heavy users compared to low-usage lenders.

3. Lower Cost to Originate

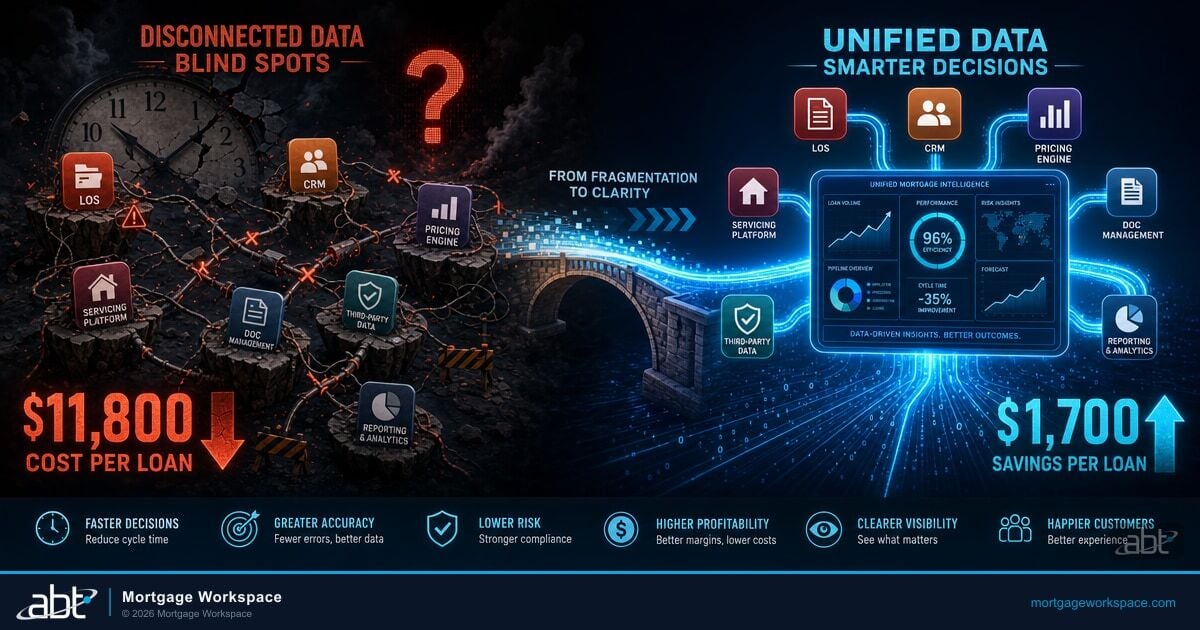

The average cost to originate a mortgage loan hit $11,800 in Q2 2025, according to Freddie Mac's cost-to-originate study. Lenders who adopted digital tools including API integrations saved up to $1,700 per loan.

At 100 loans per month, that's $170,000 in monthly savings. APIs don't just save time. They save money that compounds with every loan you close.

4. Real-Time Compliance Checks

CFPB enforcement actions and state-level regulations require lenders to validate disclosures, fees, and timelines at every stage. APIs connect your LOS to compliance engines that run these checks automatically.

When a regulation changes, the compliance API updates. Your team doesn't need to memorize new rules or manually audit every file. The system flags issues before they reach underwriting.

5. Better Borrower Communication

Borrowers expect status updates without calling their loan officer. APIs connect your CRM to your LOS so milestone notifications fire automatically. Application received. Appraisal ordered. Clear to close.

60% of borrowers engage in mortgage activities via mobile devices. API-connected portals let them upload documents, e-sign disclosures, and track progress from their phone.

Real-World API Use Cases in Mortgage Lending

Open Banking APIs for Income Verification

Open banking APIs pull bank statements and payroll data directly from the borrower's financial institution. No more chasing borrowers for pay stubs. No more waiting for PDFs to arrive by email.

These APIs verify income and assets in seconds, cutting verification time from 48 hours to under 4 hours for most loan types.

Automated Appraisal Ordering

APIs connect your LOS to appraisal management companies. When a loan hits the right milestone, the appraisal order fires without anyone clicking a button. The completed report flows back into the file the same way.

Credit Pull Integration

Tri-merge credit reports from Equifax, Experian, and TransUnion pull through a single API call. The data populates your LOS, feeds your AUS, and updates your pricing engine simultaneously.

What to Look for in an API-Ready Mortgage Platform

Not every mortgage platform handles APIs well. Here's what separates the good from the frustrating:

- Published API documentation: If the vendor won't share their API docs before you sign, walk away

- RESTful architecture: REST APIs are the industry standard. SOAP-based systems signal legacy architecture

- Webhook support: Webhooks push data when events happen instead of requiring you to poll for updates

- Rate limiting transparency: Know how many API calls you can make per minute before you hit a wall

- Sandbox environment: A testing environment where your team can build and test integrations without touching production data

Mortgage technology providers serving 750+ financial institutions build their platforms with these capabilities from the start. MortgageExchange was designed for exactly this environment, connecting Encompass, Calyx, and other LOS platforms to the broader lending ecosystem through RESTful APIs with full sandbox support. They've seen what breaks at scale and engineered around it. See also our breakdown of The Hidden Costs of Poor Integration for Credit Unions.

Is Your Software Stack Built for the Client Experience You Want?

API-driven mortgage software is what lets your systems talk so borrowers get a smooth experience instead of repeated requests. MortgageWorkspace connects your platforms so the client experience reflects how modern lending should feel.

Frequently Asked Questions

An API (Application Programming Interface) in mortgage lending is a software connection that lets your loan origination system, CRM, pricing engine, and compliance tools exchange data automatically. APIs eliminate manual data entry between systems, reduce errors, and speed up loan processing from application through closing.

Freddie Mac's 2025 cost-to-originate study found that lenders using digital tools including API integrations saved up to $1,700 per loan. With the average cost to originate at $11,800 per loan, that represents a 14% reduction in per-loan expenses through automated data exchange and fewer manual processing steps.

APIs connect your loan origination system to compliance engines that automatically validate disclosures, fee calculations, and regulatory timelines at every stage of the loan process. When regulations change, the compliance API updates without requiring manual staff retraining, reducing the risk of violations and CFPB enforcement actions.

ICE Mortgage Technology phased out legacy SDK integrations for Encompass in 2025, replacing them with Developer Connect and Partner Connect APIs. SDKs required local installation and version-specific code. The newer REST APIs are cloud-based, platform-independent, and allow real-time data exchange without local software dependencies.

Talk to a Mortgage IT Specialist

Building an API-connected mortgage operation takes the right platform, the right integrations, and a team that knows how mortgage technology works at scale. Talk to a mortgage IT specialist about connecting your systems with MortgageExchange and other API-driven tools for faster closings and fewer errors.