In This Article

- What Scalable Mortgage Technology Actually Means

- Why Scaling Failures Cost More Than Downtime

- Five IT Metrics That Predict Growth Readiness

- Mortgage BI: The Visibility Layer That Surfaces Scaling Signals

- Roadblocks That Kill Scaling Before It Starts

- MortgageExchange and M365 Guardian: The Data and Governance Layers Underneath

- How ABT Builds Mortgage Infrastructure for Growth

- Frequently Asked Questions

Commercial mortgage origination volume is projected to hit $805.5 billion in 2026, a 27% jump from 2025's $633.7 billion, according to the Mortgage Bankers Association. Purchase originations are forecast to grow 5.1%, with refinances climbing 8.3%. That volume has to flow through your loan origination system, your core banking interfaces, your cloud infrastructure, and the security perimeter that protects all of it. The lenders who scaled their IT before the wave hits will capture that growth. Everyone else will drown in ticket queues, integration timeouts, and audit findings that take three weeks to clear.

Why ABT Runs Mortgage IT Scaling for 750+ Financial Institutions

- Mortgage BI dashboards tuned to scaling signals that examiners and CFOs both care about, pull-through rate, cycle time, processor capacity, and concurrent user load against the actual LOS workflow rather than vendor-default IT health widgets.

- MortgageExchange connects the loan origination system to core banking, document management, and credit pull services through a managed integration layer ABT operates, so adding a branch or onboarding a new LOS does not require six months of custom middleware work.

- M365 Guardian wraps the Microsoft 365 tenant that lenders run on with 24x7 detection across Microsoft Entra ID, Microsoft Defender, Microsoft Purview, and Microsoft Sentinel, so the security posture scales with loan volume instead of falling behind it.

Meanwhile, 67% of mortgage lenders have already moved to cloud-based loan origination platforms. The gap between lenders with scalable infrastructure and those still running on-premise legacy stacks is widening every quarter. If your IT environment cannot absorb a 27% volume increase without breaking, these numbers are not good news. They are a warning.

This article breaks down the IT metrics that predict whether your mortgage technology is ready to grow, where the common failure points hide, and how the Mortgage BI visibility layer combined with the MortgageExchange data layer and the M365 Guardian security overlay keeps the whole stack ahead of demand.

What Scalable Mortgage Technology Actually Means

Scalability is not about surviving a traffic spike. It is about the entire technology stack absorbing more users, more loan files, more integrations, and more compliance demands without degrading performance or blowing the budget. For a mortgage lender, the stack is unusually layered. The loan officer touches the loan origination system. The processor touches the doc engine. The underwriter touches automated underwriting and the credit pull. The compliance officer touches retention, audit logging, and the regulatory technology overlay. Behind all of that sits a Microsoft 365 tenant carrying email, document collaboration, identity, and the security tooling that protects every transaction.

A scalable mortgage platform handles these simultaneously:

- More borrowers and team members across multiple branches without provisioning delays or license-tier juggling

- Higher concurrent loan volume during peak origination windows when rate drops or seasonal surges hit

- New service integrations like eClosings, automated underwriting, fraud detection, and document management connected through a managed data layer rather than one-off middleware

- Tighter compliance requirements from GLBA, FTC Safeguards Rule, and state regulators like NYDFS, with audit evidence ready to hand rather than reconstructed from screenshots

If your loan officers build workarounds to get around system limitations, that is not scaling. That is technical debt compounding at interest, with the bill arriving in the next exam cycle.

Why Scaling Failures Cost More Than Downtime

Most IT leaders think about scaling in terms of uptime. The real cost shows up in places that never trigger an alert.

Lost pipeline velocity. When the loan origination system slows during a volume spike, loan officers lose 15 to 30 minutes per file on refresh cycles and resubmissions. Across 200 loans a month, that is 50 to 100 hours of lost productivity. No alert fires for that. The Mortgage BI dashboard does.

Integration brittleness. Credit pulls, automated underwriting, borrower portals, and core banking syncs all depend on data integrations performing under load. One slow integration creates a cascade. The underwriting queue backs up. Borrowers see stale status updates. Processors start making phone calls instead of trusting the system. A managed data layer like MortgageExchange catches the cascade upstream. This connects closely to The Hidden Costs of Poor Integration for Credit Unions.

Compliance exposure. Regulatory technology integration has reduced compliance risk by 42% for lenders who embed KYC and AML automation into their platforms. Lenders who scale volume without scaling their compliance tooling are increasing risk with every new loan file. The M365 Guardian operating model layers Microsoft Purview audit logging, Microsoft Defender threat detection, and Microsoft Sentinel SIEM aggregation on the same Microsoft 365 tenant the business already runs on, so the security and audit posture grows with the volume.

Five IT Metrics That Predict Growth Readiness

You cannot improve what you do not measure. These five metrics separate lenders who are ready to grow from those who will hit a wall at the worst possible time.

1. System Uptime During Peak Origination Windows

The industry benchmark is 99.9% uptime. That number is meaningless if your downtime clusters during the busiest hours. Track uptime specifically during 8 AM to 6 PM on weekdays and during the first two weeks after a rate drop announcement. A system that delivers 99.95% annual uptime but drops to 98% during peak windows is failing exactly when it matters most. ABT monitors uptime by workload pattern, not just calendar average, and surfaces the pattern inside the Mortgage BI dashboard the executive team actually reads.

2. API Response Time Under Concurrent Load

Your integrations work fine at 50 concurrent users. What happens at 200? At 500? API response time should stay under 200 milliseconds for critical workflows like credit pulls, automated underwriting decisions, and document uploads regardless of load. Track both average response time and 95th percentile latency. The average might look healthy while 5% of transactions are timing out. Those timeouts become re-submissions, which add load, which cause more timeouts. The failure loop is self-reinforcing, and the MortgageExchange integration layer is where ABT instruments the timing signals.

3. Dashboard and Workflow Load Times

If loan officers wait more than three seconds for a dashboard to render or a document to upload, productivity drops measurably. Google's research on page load times applies to internal tools too. Every additional second of wait time reduces task completion rates. Benchmark load times across your five most-used workflows, loan pipeline view, borrower profile, document upload, disclosure tracking, and reporting dashboards. If any exceed three seconds under normal load, investigate before volume increases.

4. Resource Utilization and Elastic Scaling Thresholds

CPU and memory utilization should hover between 40% and 60% during normal operations. That leaves headroom for spikes. If you are consistently above 70%, you are one rate drop announcement away from a capacity crisis. Cloud-native infrastructure solves this with auto-scaling. Over 40% of new loan origination platform deployments now use cloud architectures specifically for elastic scaling. The question is whether your infrastructure scales automatically or requires a support ticket and a 48-hour wait.

5. Security Event Rates Per Transaction Volume

As loan volume grows, the attack surface grows with it. Track security events, failed login attempts, access anomalies, MFA bypass attempts, as a ratio to transaction volume rather than as raw counts. A lender processing 100 loans per month with 50 security events has a very different risk profile than a lender processing 1,000 loans with 50 events. The ratio tells you whether your security posture is scaling with your business or falling behind. M365 Guardian normalizes the ratio against benchmark patterns ABT sees across more than 750 financial institutions.

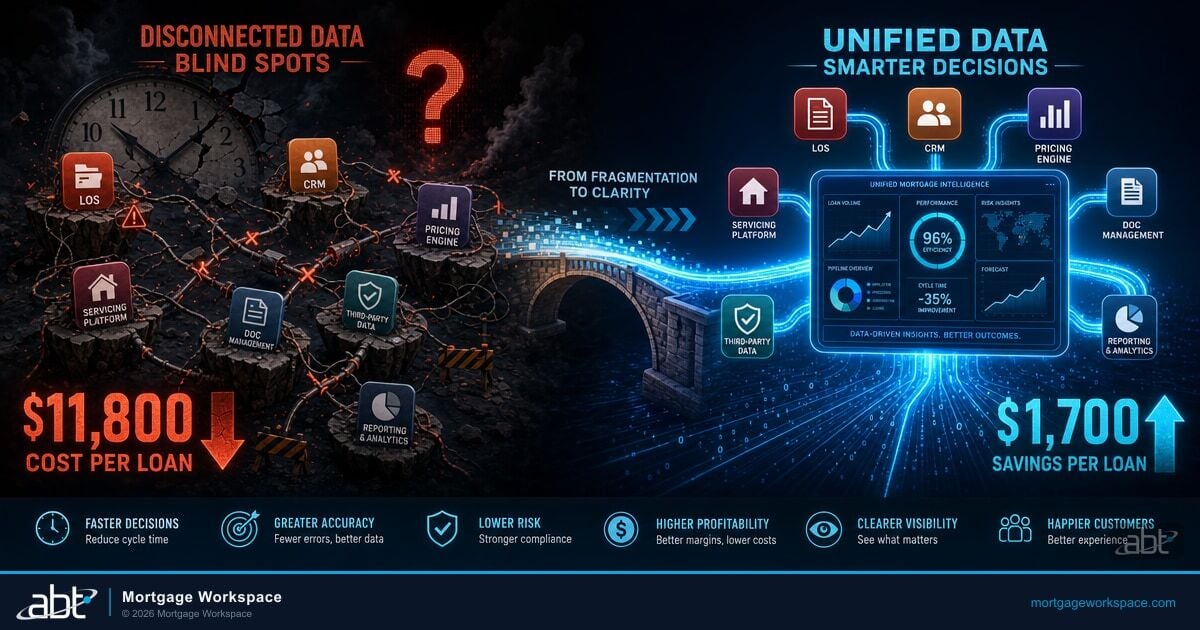

Mortgage BI: The Visibility Layer That Surfaces Scaling Signals

Mortgage BI is the business intelligence layer ABT runs for mortgage lenders. It is not a generic IT dashboard repurposed for mortgage. It is a Microsoft Power BI workspace built around the mortgage workflow, with pre-built data models that pull pull-through rate, cycle time by milestone, processor capacity, lock-to-fund ratio, concurrent active loan files, and pipeline velocity into a single view a CFO, COO, or CIO can actually read on a Monday morning. The same dashboard surfaces the IT scaling signals the five metrics above describe, system uptime by workload window, API latency at the 95th percentile, dashboard render times for the five most-used workflows, resource utilization with capacity thresholds, and security event rates per transaction volume, on top of the business signals the executive team already cares about. That is the visibility layer. Without it, scaling problems hide until they show up as missed close dates or examination findings.

Roadblocks That Kill Scaling Before It Starts

Even lenders who track the right metrics hit scaling walls when these structural problems are in the way.

Legacy Systems That Cannot Integrate

Legacy loan origination systems may still process files, but they often lack modern API connectivity. Every new integration requires custom middleware, and every custom connection becomes a maintenance liability. Technical debt from rapid technology adoption now threatens 75% of technology leaders' infrastructure by 2026, according to industry analysis. See also our breakdown of Breaking Down Barriers.

Manual Processes Hidden in Automated Workflows

Automation only works if the full chain is automated. Many lenders have automated 80% of a workflow but still require manual data re-entry at handoff points between systems. These manual steps do not scale. At low volume, a processor spends 10 minutes on re-entry per file. At high volume, that same step becomes a bottleneck that backs up the entire pipeline.

Data Silos Between Platforms

When CRM, loan origination, and compliance platforms store separate versions of borrower data, pipeline visibility collapses. Processors cannot trust the data without cross-referencing, which costs time. Managers cannot forecast accurately because reporting pulls from inconsistent sources. Clean, unified data is the foundation for scaling both operations and decision-making. Without it, every additional loan file adds friction instead of revenue.

Static Infrastructure That Requires Manual Provisioning

If adding server capacity requires a support ticket, a vendor call, and a three-day turnaround, you cannot respond to volume spikes. ABT hosts the Azure environments that mortgage lenders run on, with auto-scaling rules that eliminate the manual provisioning bottleneck entirely. The infrastructure responds to demand in minutes, not days.

Compliance Tooling That Does Not Scale with Volume

What works for 50 users often breaks at 500. Role-based access controls, audit logging, and automated compliance monitoring need to scale linearly with the user base and transaction volume. Lenders who treat compliance as a one-time configuration instead of a scaling requirement discover gaps during audits, which is the worst time to find them.

MortgageExchange and M365 Guardian: The Data and Governance Layers Underneath

The Mortgage BI dashboard is the visibility layer. What feeds it matters more than the dashboard itself. MortgageExchange is the data integration layer ABT operates between the loan origination system, the core banking platform, document management, credit pull services, and the rest of the mortgage technology ecosystem. It is the largest interface product ABT runs. Rather than custom middleware bolted on for every new integration, MortgageExchange standardizes the data pipes so adding a branch, integrating a new LOS, or onboarding a new credit vendor takes weeks instead of quarters. The same data plane feeds the Mortgage BI signals upward and feeds the audit trail Microsoft Purview captures for the compliance layer.

M365 Guardian is the security governance overlay. ABT manages the Microsoft 365 tenant the lender runs on, applies Microsoft Entra ID Conditional Access, Microsoft Intune device compliance, Microsoft Defender for Office 365 and Defender for Endpoint, Microsoft Purview retention and audit logging, and a Microsoft Sentinel SIEM tuned to mortgage attack patterns including borrower-payoff phishing, wire-instruction tampering, and registered-loan-officer impersonation. The 24x7 security operations center watches the Sentinel signals every minute of the day. That is the security and audit layer that lets the visibility and data layers scale without the security posture falling behind. Together, Mortgage BI on top, MortgageExchange in the middle, M365 Guardian wrapping the tenant the whole stack runs on, this is what ABT means when it says it scales mortgage IT for growth.

How ABT Builds Mortgage Infrastructure for Growth

Access Business Technologies is a Tier-1 Microsoft Cloud Solution Provider that manages Microsoft 365 tenants and hosts Azure environments for more than 750 financial institutions, including the mortgage lenders that run on the MortgageWorkSpace brand. With 25+ years of mortgage technology experience and SOC 2 Type II certification with NDA-available attestation, ABT builds environments that grow with the business. Our guide to How API-Driven Mortgage Software Helps You Build the Perfect Client Expe goes deeper on this.

| Layer | What ABT Operates | What the Lender Experiences |

|---|---|---|

| Visibility (Mortgage BI) | Microsoft Power BI workspace with pre-built mortgage data models for pull-through rate, cycle time, processor capacity, lock-to-fund ratio, and pipeline velocity, alongside IT scaling signals like uptime by workload, API latency, and security event rates per transaction volume. | One executive dashboard the CFO, COO, and CIO can read together, with business signals and IT scaling signals in the same view. |

| Data Plane (MortgageExchange) | Managed integration layer connecting the loan origination system to core banking platforms, document management, credit pull services, and automated underwriting through standardized data pipes ABT runs and supports. | Adding a branch, onboarding a new LOS, or integrating a new credit vendor takes weeks instead of quarters, and the audit trail flows directly into Microsoft Purview. |

| Security and Governance (M365 Guardian) | Microsoft 365 tenant managed under delegated admin, with Microsoft Entra ID Conditional Access, Microsoft Intune device compliance, Microsoft Defender for Office 365 and Endpoint, Microsoft Purview retention and audit logging, and Microsoft Sentinel SIEM tuned to mortgage attack patterns, monitored by ABT's 24x7 SOC. | The security posture scales with loan volume rather than falling behind it, and audit evidence is ready to hand when an examiner asks for the 24-month retention history across every entity in the firm's footprint. |

A rate drop hits. Volume spikes 40% in three weeks. The loan origination system slows. The processor team starts complaining. The CIO emails the LOS vendor. The vendor replies in four days. Meanwhile, three loans miss close dates, the CFO loses pipeline visibility because Mortgage BI signals are not being captured, and the security operations team is too understaffed to keep up with the elevated event rate. The next examination opens before the scaling problem is fixed.

The same rate drop hits. ABT's monitoring catches the latency creep two days before loan officers notice. The Azure environment auto-scales. MortgageExchange routes the additional load through redundant data pipes. The Mortgage BI dashboard shows pull-through holding steady and cycle time staying flat. M365 Guardian's Sentinel rules absorb the elevated event count without false-positive flooding the SOC. The lender captures the volume. The next examination opens, and the audit evidence is already in hand.

Get a Mortgage IT Scaling Readiness Review

ABT runs the Mortgage BI, MortgageExchange, and M365 Guardian operating model described in this article for mortgage lenders preparing for 2026 volume growth. A 30-minute conversation maps your current IT scaling signals, surfaces the integration brittleness and security exposure your next exam cycle will find, and outlines what an ABT-managed deployment would cover. No commitment, no quote, no obligation.

Key Takeaway

Five IT metrics predict whether mortgage technology can absorb a 27% volume increase, system uptime during peak windows, API response time under concurrent load, dashboard and workflow load times, resource utilization with elastic scaling thresholds, and security event rates per transaction volume. The Mortgage BI dashboard surfaces the signals. MortgageExchange feeds the data plane underneath. M365 Guardian wraps the Microsoft 365 tenant with the security and audit posture that scales with the business. ABT runs all three layers for more than 750 financial institutions, including the mortgage lenders that run on MortgageWorkSpace.

Frequently Asked Questions

Mortgage lenders should evaluate IT scalability metrics quarterly at minimum, with additional reviews before any planned growth event such as branch expansion, new loan origination system integration, or anticipated volume increases from rate changes. Continuous automated monitoring inside a Mortgage BI workspace provides real-time visibility between formal reviews, catching degradation trends before they become outages. ABT instruments the metrics inside the Mortgage BI dashboard alongside business signals like pull-through rate and cycle time so the executive team sees IT scaling readiness in the same view as business performance.

The clearest sign is when the team creates manual workarounds to compensate for system limitations, exporting data to spreadsheets for tracking, re-keying borrower information between platforms, or scheduling batch processes during off-hours because the system cannot handle concurrent loads during business hours. A managed data integration layer like MortgageExchange eliminates the spreadsheets and re-keying by standardizing the data pipes between the loan origination system, core banking, document management, and credit pull services.

Cloud migration removes infrastructure capacity constraints but does not automatically solve scaling problems. A poorly architected cloud deployment can be just as brittle as on-premise infrastructure. Effective cloud scaling requires auto-scaling rules, proper load balancing, integration architecture design, and ongoing monitoring to deliver real elastic scalability. ABT hosts the Azure environments that mortgage lenders run on and operates the auto-scaling rules so the infrastructure responds to volume spikes in minutes rather than days.

Mortgage platforms should target sub-200 millisecond API response times for critical workflows including credit pulls, automated underwriting decisions, and document uploads. Track both average response time and 95th percentile latency because averages can mask timeout problems affecting a significant percentage of transactions during peak volume periods. The MortgageExchange data integration layer is where ABT instruments the timing signals across credit, core banking, doc management, and LOS connections so latency creep is caught upstream rather than after the underwriting queue backs up.

ABT integrates with existing loan origination systems and core banking platforms through MortgageExchange, the managed integration layer ABT operates between the LOS, core banking, document management, credit pull services, and automated underwriting. Rather than replacing current tools, ABT connects them through standardized data pipes that include monitoring, security, and elastic scalability. The Mortgage BI dashboard sits above the data plane to surface pull-through, cycle time, and IT scaling signals in a single view, and M365 Guardian wraps the Microsoft 365 tenant the lender already runs on with continuous security monitoring and audit-ready evidence.

M365 Guardian is the operating model ABT runs on top of the Microsoft 365 tenant the mortgage lender already uses. ABT manages the tenant under delegated admin and applies Microsoft Entra ID Conditional Access tuned to branch geography and loan officer behavior, Microsoft Intune device compliance covering firm-owned and personal devices, Microsoft Defender for Office 365 and Defender for Endpoint, Microsoft Purview retention and audit logging aligned to GLBA and FTC Safeguards Rule expectations, and a Microsoft Sentinel SIEM deployment tuned to mortgage attack patterns including borrower-payoff phishing, wire-instruction tampering, and loan officer impersonation. ABT's 24x7 security operations center watches the Sentinel signals, so security event rates per transaction volume stay inside the benchmark even as loan volume climbs.