A 2025 Forrester study found that organizations using Microsoft Purview DLP achieved a 30% reduction in data breach likelihood. For mortgage lenders handling Social Security numbers, bank statements, and tax returns on every loan file, that number translates directly into fewer regulatory investigations and lower insurance premiums.

The global DLP market is growing at 22.3% CAGR through 2030, driven by cloud adoption, generative AI risk, and regulatory expansion. In 2025, over 3,158 publicly disclosed breaches exposed more than 1.7 billion records. The average breach cost hit $4.88 million, the highest IBM has ever recorded.

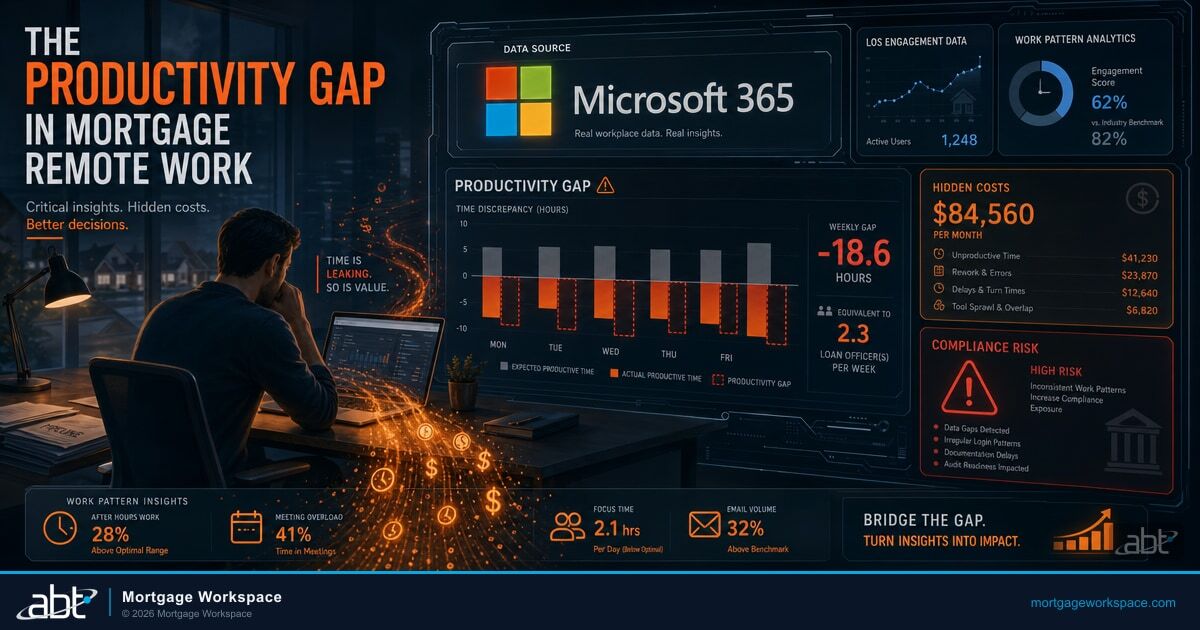

Mortgage lenders sit at the intersection of every factor driving that growth. This guide covers how DLP works in mortgage compliance, the technologies that support it, and what lenders need to do now.

In This Article

How Compliance Affects Mortgage Lending Operations

Every mortgage loan file contains data that falls under multiple regulatory frameworks. Here are the compliance pressures shaping daily operations:

- Data privacy regulations: GLBA requires financial institutions to protect customer information. California's updated CCPA amendments now mandate annual cybersecurity audits and automated decision-making disclosures. These aren't optional checkboxes. They carry penalties.

- Loan file accuracy: The FDIC flagged 65 HMDA violations in 2024 tied to data collection errors. Most traced back to misconfigured LOS systems, not human mistakes. Technology gaps create compliance gaps.

- Cybersecurity threats: The average data breach costs $4.88 million. Mortgage institutions are high-value targets because every file contains SSNs, income data, and bank account numbers. A single breach triggers both regulatory penalties and reputational damage.

- Fair lending requirements: ECOA and HMDA demand proof that lending decisions are unbiased. New York has proposed a law requiring annual impact assessments for AI-driven underwriting tools, including bias evaluations and public disclosure.

What Is DLP and How Does It Drive Mortgage Compliance?

Data Loss Prevention is a security technology that monitors, detects, and blocks unauthorized movement of sensitive information. In a mortgage environment, DLP policies watch every channel where borrower data flows: email, file transfers, cloud storage, and endpoint devices.

Here is how DLP operates in a mortgage compliance company:

- Monitors email and file transfers: DLP scans outgoing emails and attachments for SSNs, account numbers, and other sensitive data types. If a loan officer accidentally attaches a borrower's tax return to an external email, DLP blocks the send and logs the incident.

- Enforces policies in real time: Rules run automatically. Block transfers to unapproved domains. Encrypt documents before they leave the tenant. Apply sensitivity labels to loan files based on content.

- Supports audits and investigations: Every flagged incident gets logged with timestamps, user identity, content type, and action taken. Compliance officers pull these logs for examiners without reconstructing timelines manually.

- Reduces insider threats: Content inspection and user behavior analytics detect patterns that suggest data exfiltration. Microsoft Purview's Insider Risk Management integrates directly with DLP to adjust enforcement based on user risk level.

Microsoft Purview DLP now extends protections to generative AI tools. If an employee pastes borrower data into ChatGPT or an unmanaged AI application, Purview's policies can detect and block the action. This matters as AI adoption accelerates across mortgage operations.

How Technology Is Reshaping Mortgage Compliance

Automated compliance workflows

Conditional logic and workflow engines handle regulatory reporting, data classification, and audit trail generation. Automation eliminates the clerical errors that account for most HMDA violations. It also ensures on-time submissions to regulators regardless of staff turnover or workload spikes.

Centralized data repositories

Cloud-based systems consolidate loan data, compliance records, and documentation into a single platform. Teams access the same information from any location. This eliminates the version-control problems that plague multi-office mortgage operations. We cover Navigating Compliance Challenges in Mortgage Management in a companion piece.

Intelligent risk detection

AI-driven analysis moves beyond manual quality checks. Machine learning models analyze user behavior and transaction patterns during the application process, flagging anomalies that human reviewers would miss. This catches fraud earlier in the pipeline and reduces false positives over time.

Real-time compliance dashboards

Live dashboards give compliance officers visibility into policy status, alert volumes, and performance metrics across the entire operation. Decision-making accelerates because the data is current, not stale reports assembled weekly. For ABT's fuller take, see Freddie Mac AI Mandate Compliance Checklist.

Four Technologies Powering Modern Mortgage Compliance

1. Identity and access management (IAM)

IAM controls who accesses loan origination systems, borrower data, and internal workflows. Microsoft Entra ID (formerly Azure AD) enforces MFA, Conditional Access policies, and role-based permissions. Only verified personnel touch sensitive files. Entra ID's 2025 updates include Conditional Access for AI agents and jailbreak detection in the Authenticator app, closing gaps that earlier IAM systems left open.

2. E-signature and document authentication

The Federal Reserve listed inaccurate information reporting among the top ten HMDA compliance challenges in 2024. Secure e-signature tools and automated document validation prevent mismanagement at the point of collection. They also create tamper-evident records that satisfy examiner requirements for remote closings.

3. Regulatory change management

Mortgage compliance shifts constantly. The CFPB's reduced enforcement role since early 2025 has pushed oversight to state attorneys general, creating a patchwork of new requirements. AI-powered regulatory tracking tools deliver real-time alerts on rule changes across all 50 states, so compliance teams update policies before deadlines arrive.

4. Compliance analytics platforms

With data flowing through LOS, CRM, document management, and communication tools, blind spots are inevitable without analytics. Compliance analytics platforms pull data across your tech stack to surface inconsistencies, flag violations, and deliver actionable insights before examiners find the problems. This connects closely to TRID Compliance IT Checklist for Mortgage Lenders.

Adoption Tips for Mortgage Compliance Technology

- Start with a risk assessment: Identify your highest areas of vulnerability before selecting tools. Map current gaps against GLBA, FTC Safeguards Rule, and applicable state regulations.

- Choose scalable platforms: Your compliance needs will grow with loan volume and regulatory complexity. Select tools that adapt through configuration, not custom development.

- Integrate with existing systems: New technology must connect to your LOS, CRM, and communication platforms. Siloed compliance tools create the same data gaps they're supposed to fix.

- Invest in ongoing training: Technology is only effective when people use it correctly. Regular training reduces misconfiguration risk and improves adoption rates across your team.

Securing Mortgage Compliance with DLP and Microsoft Purview

Compliance in mortgage lending tightens every year. DLP, AI-driven risk detection, and cloud-native platforms are no longer optional. They're the baseline.

Mortgage Workspace, the mortgage division of Access Business Technologies, deploys Microsoft Purview DLP as part of the Guardian operating model. Guardian wraps around your Microsoft 365 tenant to classify sensitive data, enforce DLP policies, and monitor compliance drift continuously. Serving 750+ financial institutions, we configure these tools specifically for mortgage regulatory requirements.

Talk to a mortgage IT specialist about deploying DLP and Purview across your mortgage operation.

Is Borrower Data Leaving Your Walls Without You Knowing?

Data loss prevention is the control that stops sensitive borrower information from walking out through email and shared files. MortgageWorkspace configures Microsoft 365 DLP for the way mortgage teams actually handle documents.

DLP monitors and controls how sensitive borrower data moves across email, file transfers, cloud storage, and endpoint devices. It blocks unauthorized sharing automatically and logs every incident for audit trails. Organizations using Microsoft Purview DLP achieved a 30% reduction in breach likelihood according to a 2025 Forrester study, translating to fewer regulatory penalties and lower insurance costs.

Microsoft Purview DLP extends data protection to generative AI applications. If an employee pastes borrower SSNs, income data, or account numbers into ChatGPT or an unmanaged AI tool, Purview detects the sensitive content and blocks the transfer. This prevents accidental data exposure through AI tools while allowing your team to use approved AI applications safely.

Modern DLP platforms integrate with loan origination systems, CRM tools, and document management platforms through APIs and native connectors. Microsoft Purview connects natively across Microsoft 365 services including SharePoint, Outlook, Teams, and OneDrive. Third-party connectors extend coverage to non-Microsoft applications in your compliance stack.

The average data breach costs $4.88 million according to IBM's 2025 report, the highest figure ever recorded. Mortgage lenders face additional regulatory penalties from GLBA, state privacy laws, and the FTC Safeguards Rule. DLP prevention costs typically run $15 to $50 per user annually, which is orders of magnitude less than breach remediation, legal fees, and lost customer trust.