In This Article

- Why Speed and Compliance Pull in Opposite Directions

- What MSPs Do Differently for Mortgage Origination

- Five Capabilities That Remove the Speed-Compliance Tradeoff

- The MSP Supply Chain Risk Most Lenders Ignore

- Choosing the Right MSP for Mortgage Lending

- How ABT Delivers Both Speed and Compliance

- Frequently Asked Questions

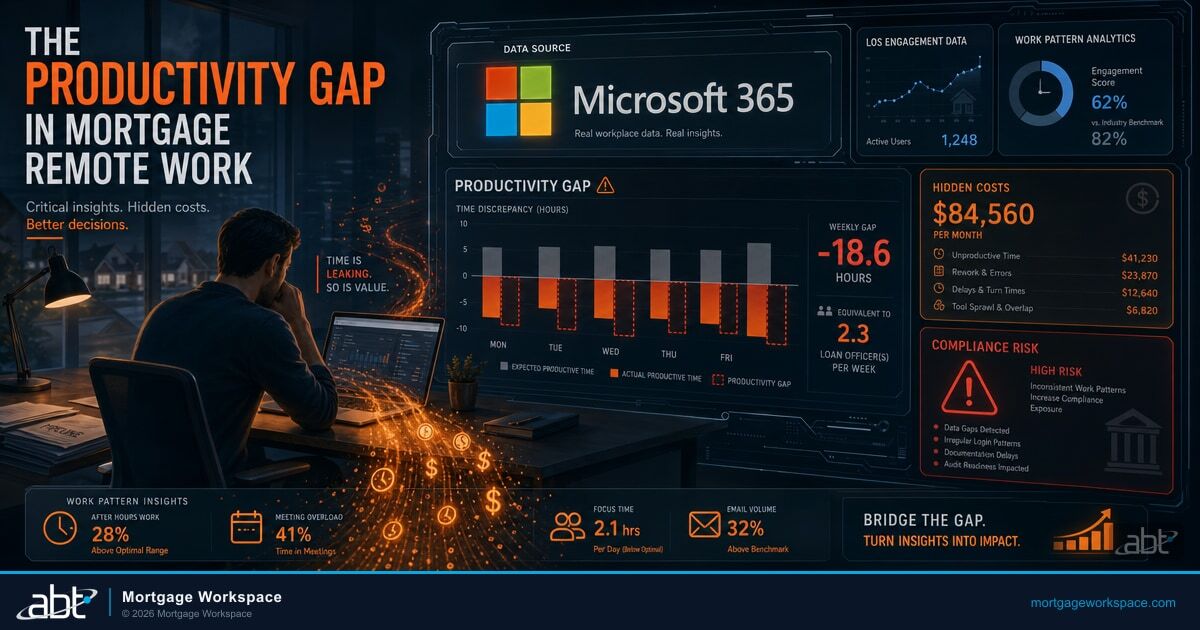

Only 34% of mortgage credit inquiries result in a completed origination, according to Experian's 2026 housing market report. Meanwhile, production costs exceed $11,000 per loan, and up to 40% of the origination process remains manual. Lenders are losing deals to slow processing and losing money to manual errors at the same time.

The problem isn't a lack of technology. Most lenders have a loan origination system, a CRM, compliance tools, and document management. The problem is that these systems don't talk to each other, rules get applied inconsistently, and compliance checks slow down workflows instead of running alongside them.

Managed service providers that specialize in mortgage technology solve this by configuring the systems lenders already own to work together. Speed and compliance stop being opposing forces when the infrastructure is designed correctly from the start. For mortgage companies, credit unions, and banks running lending operations, the right MSP turns this from a tradeoff into an architecture question. The MSPs that pull this off run a Microsoft-native stack, manage it under a Microsoft 365 Direct-Bill Cloud Solution Provider relationship, and overlay a financial-services operating model on top.

Lenders using automated compliance monitoring detected regulatory violations 68% faster than those relying on quarterly manual audits, and reduced remediation costs by an average of $340,000 annually per institution.

Why Speed and Compliance Pull in Opposite Directions

Every mortgage loan involves a tension. Borrowers want fast approvals. Regulators want documented proof that every step followed the rules. When lenders prioritize speed, compliance gaps appear. When they prioritize compliance, borrowers leave for faster competitors.

The numbers illustrate the pressure. TRID requires Loan Estimates within three business days. Fannie Mae requires cybersecurity incident reporting within 36 hours. State-level regulations keep adding requirements. Each one adds a step, a check, or a documentation requirement to the origination process. How Microsoft 365 helps lenders stay ahead of regulatory changes walks through how the M365 surface absorbs new rules without retooling the workflow.

Speed-First Approach (Risk)

- Compliance checks skipped under deadline pressure

- Manual workarounds bypass automated safeguards

- Audit trail gaps appear during examinations

- Regulatory fines and repurchase demands

Compliance-First Approach (Cost)

- Processing times extend beyond borrower patience

- Manual review bottlenecks at every handoff

- Deals lost to faster-moving competitors

- Higher cost per loan from redundant checks

At the same time, borrower expectations keep accelerating. Fintech lenders promise digital-first experiences with minimal friction. Experian's data shows that 50% of prospective borrowers say understanding what they could qualify for would be the most helpful step in their homeownership journey. The lenders who answer that question fastest win the deal.

The traditional approach treats this as a binary. Either you move fast and accept compliance risk, or you add manual review steps and accept slower processing. MSPs with mortgage expertise reject that premise. They configure systems so that compliance runs in the background while borrowers experience speed.

What MSPs Do Differently for Mortgage Origination

A generic MSP manages your servers and resets passwords. A mortgage-specialized MSP configures your entire technology stack around the specific requirements of lending compliance. The difference is significant and measurable.

Mortgage MSPs understand which compliance checks can run automatically (data validation, fee tolerance calculations, deadline tracking) and which require human judgment (underwriting decisions, exception handling). They build workflows that route the automatic checks through software and the judgment calls to the right person at the right time. Reducing loan origination costs for credit unions covers the operational gains that follow when those handoffs become automated.

The Integration Gap Most Lenders Live With

Your LOS needs to talk to your CRM, your document management system, your credit reporting vendor, your title company integrations, and your compliance monitoring tools. When these systems are siloed, staff re-enter data manually. Manual re-entry introduces errors. Errors cause compliance findings. A specialized MSP eliminates those manual handoffs through API integrations, middleware connectors, and automated data flows that run on the same Microsoft Entra ID identity layer used for sign-in.

The MSP's role is to make the technology do what lenders assumed it already did when they bought it. Borrower data entered during pre-qualification flows automatically to underwriting without anyone retyping it. Compliance rules fire automatically at each stage gate. Audit trails write themselves in the background, captured by Microsoft Purview Audit and bound to mailboxes, SharePoint sites, OneDrive accounts, and Teams channels through Purview retention policies.

Five Capabilities That Remove the Speed-Compliance Tradeoff

Automated Rule Engines

When regulations change, manual updates to loan workflows create bottlenecks. A properly configured rule engine lets compliance teams update business rules centrally without modifying the underlying application. When CFPB adjusts QM thresholds, the rule engine picks up the new values. Every loan processed after that point uses the correct thresholds without developer intervention. Power Automate flows within the Microsoft 365 environment handle these rule updates natively when configured by an MSP that understands both the technology and the regulation.

Real-Time Compliance Monitoring

Instead of finding compliance failures during quarterly audits, monitoring tools watch origination systems continuously. If a system skips a mandatory income verification step, the alert fires immediately. If a Loan Estimate deadline approaches without delivery, the team gets notified before the deadline passes. This catches problems in hours instead of months. ABT's M365 Guardian monitoring layer extends this principle to the Microsoft 365 tenant itself, watching for compliance drift in the Conditional Access, Defender, and Microsoft Purview policies that protect borrower information.

System Integration and Data Flow

Borrower data should enter the system once and flow through every step automatically. MSPs connect the LOS, CRM, credit bureaus, appraisal management companies, and compliance tools through APIs and middleware. This eliminates the data re-entry errors that cause fee mismatches between Loan Estimates and Closing Disclosures. When the entire stack runs on Microsoft 365, those integrations benefit from single sign-on through Microsoft Entra ID, unified data loss prevention through Microsoft Purview, and consistent audit trails written to Purview Audit Premium.

Standardized Decision Logic

When multiple team members handle loan files, inconsistency creeps in. Rule-based decision engines apply the same criteria every time. If a DTI exceeds 43%, the system flags it regardless of who is processing the file. If a property type doesn't match program eligibility, the system catches it before the file reaches underwriting. Consistent logic means faster processing and fewer compliance exceptions.

Background Audit Trails

Every action in the origination process must be traceable. But if logging slows down the workflow, teams start skipping steps. MSPs configure audit trails that run in the background, recording who accessed what data, when documents were generated, and which decisions were made. The compliance team gets a complete record. The origination team sees no friction. M365 Guardian's monitoring layer adds a second audit dimension, tracking the Microsoft 365 tenant activity that sits underneath the origination workflow: file access in SharePoint and OneDrive, external sharing events flagged by Microsoft Purview DLP, sign-in patterns captured by Microsoft Entra ID, and incident timelines aggregated in Microsoft Sentinel.

The reason this configuration actually holds together at a mortgage lender is the operating model behind it. Microsoft 365 Direct-Bill Cloud Solution Provider status is Microsoft's top program tier for partners. A Direct-Bill partner transacts directly with Microsoft, holds dedicated Microsoft support engineers, and is operationally accountable to Microsoft for how customer tenants are configured. That accountability is what lets an MSP manage Microsoft 365 tenants under delegated admin instead of just reselling licenses. ABT layers M365 Guardian, its lending-specific operating model, on top of that Direct-Bill relationship. Guardian configures and monitors Microsoft Entra ID Conditional Access for branch geographies and registered representatives, Microsoft Intune for borrower-data device compliance, Microsoft Defender for Office 365 for the email channel that handles most customer correspondence, and Microsoft Purview Audit, DLP, retention, and Communication Compliance for the books-and-records side that auditors actually grade.

The MSP Supply Chain Risk Most Lenders Ignore

Here's a question most lenders never ask their MSP: what third-party platforms does your MSP depend on?

The answer matters because MSP platform breaches have become a pattern:

Nation-state supply chain attack affected 18,000+ organizations through a trusted software update channel

REvil exploited zero-day vulnerabilities in the MSP platform, hitting 1,500+ organizations through their MSP relationships

Critical authentication bypass vulnerability exploited in the wild, giving attackers access to managed endpoints

These aren't edge cases. They're the platforms that most MSPs run their entire operations on. When your MSP depends on ConnectWise or Kaseya, your lending environment inherits that supply chain risk. A breach at the MSP platform level can give attackers access to every client the MSP manages. For mortgage lenders handling borrower Social Security numbers, income data, and account information, that exposure is a Fannie Mae InfoSec compliance problem. Beyond Microsoft Secure Score: building a mortgage operations security program covers how M365 Guardian translates a clean Microsoft baseline into the kind of program examiners reference.

The question isn't whether your MSP has been breached. The question is whether your MSP's tooling has been breached, and whether you'd even know.

The alternative is an MSP that runs a pure Microsoft stack. Microsoft's security infrastructure (Microsoft Entra ID, Microsoft Defender, Microsoft Intune, Microsoft Purview, Microsoft Sentinel) is the technology that financial regulators already trust and reference in examination guidance. When the MSP's own tooling is Microsoft-native, there is no third-party platform layer adding supply chain risk between the MSP and your environment.

Choosing the Right MSP for Mortgage Lending

Not all MSPs are equal in the mortgage context. Four areas separate the specialists from the generalists:

Can the MSP explain the difference between TRID tolerance categories? Do they understand Fannie Mae's cybersecurity supplement? Have they configured Microsoft Purview DLP policies for mortgage data types like borrower NPI and loan-level files? Generic IT providers can't answer these questions.

Is the MSP a Microsoft 365 Direct-Bill Cloud Solution Provider with direct Microsoft support access? Or do they buy licenses through a distributor and rely on community forums when something breaks at 2 AM?

Ask what platforms the MSP uses internally. If the answer includes ConnectWise, Kaseya, or SolarWinds, understand that you're accepting their supply chain risk. An MSP running Microsoft-native tooling doesn't carry that exposure.

How many mortgage lenders does the MSP serve? How many financial institutions total? Mortgage compliance has specific requirements that general-purpose MSPs learn by making mistakes on their clients.

How ABT Delivers Both Speed and Compliance

Access Business Technologies is a cloud-first MSP and a Microsoft 365 Direct-Bill Cloud Solution Provider dedicated to financial services. ABT manages Microsoft 365 tenants for more than 750 financial institutions, including mortgage companies, credit unions, and banks. ABT runs a pure Microsoft technology stack. No ConnectWise. No Kaseya. No SolarWinds. When MSP platforms get breached, ABT-managed clients have zero exposure to the breached vendor.

ABT configures Microsoft 365 and the full Microsoft security stack specifically for lending requirements through its M365 Guardian operating model. That means:

- M365 Guardian hardening: Microsoft Entra ID Conditional Access policies, Microsoft Intune device compliance, and identity baseline configuration tuned to financial services requirements from day one

- Microsoft Purview policies for borrower data: Purview sensitivity labels and data loss prevention rules configured specifically for NPI, loan documents, and underwriting files; Purview Audit Premium retention extended to one year and (with the add-on) up to ten to satisfy mortgage recordkeeping expectations

- Compliance monitoring: M365 Guardian's continuous tenant health checks catch configuration drift before examiners do, and route findings into a Microsoft Sentinel incident timeline that doubles as evidence for Fannie Mae cybersecurity reporting

- Power Automate workflows: TRID deadline tracking, document routing, and compliance checkpoint automation built into the Microsoft 365 environment your team already uses

The approach eliminates the speed-compliance tradeoff. Compliance rules run in the background through automated checks. Origination teams see faster workflows because manual re-entry and manual compliance checks are replaced with integrated, automated systems. One partner handles licensing, configuration, security, compliance, and integration. That is what it means to be both a full-service MSP and a Microsoft 365 Direct-Bill Cloud Solution Provider in a single relationship.

The Direct-Bill relationship matters operationally because it shortens the path from a frontline issue at 2 AM to a Microsoft engineer. ABT escalates directly into Microsoft support without a distributor in the middle, and the Microsoft 365 tenant remains the lender's tenant, managed under delegated admin through Granular Delegated Administrative Privileges (GDAP) so vendor oversight under amended SEC Regulation S-P and Fannie Mae third-party expectations is satisfied by the same configuration that runs day-to-day operations.

Stop Choosing Between Speed and Compliance

ABT's AI Readiness Scan evaluates your Microsoft 365 environment in minutes. See where your origination infrastructure stands on security, compliance, and data governance before your next examination, with M365 Guardian and Microsoft Purview gaps surfaced against your current tenant baseline.

Frequently Asked Questions

MSPs configure automated rule engines that apply compliance checks in the background while borrowers experience faster processing. They integrate loan origination systems with CRMs, document management, and compliance tools through APIs so data flows automatically without manual re-entry. This eliminates the errors that cause compliance findings while reducing the steps that slow down loan processing. The MSPs that hold this together at a mortgage lender run on Microsoft 365 and manage the tenant under a Microsoft 365 Direct-Bill Cloud Solution Provider relationship, with audit trails captured in Microsoft Purview Audit and identity controlled by Microsoft Entra ID Conditional Access.

Most MSPs operate on third-party platforms like ConnectWise, Kaseya, or SolarWinds. When these platforms are breached, every MSP client inherits the exposure. For mortgage lenders handling borrower SSNs, income data, and account information, this creates compliance risk under Fannie Mae's InfoSec requirements. MSPs running a pure Microsoft stack avoid this third-party platform layer entirely, eliminating that supply chain risk vector and keeping the security boundary inside Microsoft Defender, Microsoft Purview, Microsoft Intune, Microsoft Entra ID, and Microsoft Sentinel.

Evaluate four areas: regulatory knowledge of mortgage-specific requirements like TRID and Fannie Mae cybersecurity rules, Microsoft certification depth including Microsoft 365 Direct-Bill Cloud Solution Provider status with direct Microsoft support access, technology stack transparency to understand supply chain risk from third-party MSP platforms, and industry track record measured by the number of financial institutions served and the operating model the MSP layers on top of the Microsoft baseline.

A pure Microsoft stack uses Microsoft Entra ID, Microsoft Defender, Microsoft Intune, Microsoft Purview, and Microsoft Sentinel for security instead of third-party MSP platforms. When ConnectWise or Kaseya experiences a breach, lenders on Microsoft-native infrastructure have zero exposure to the breached vendor. Microsoft's security tools are already trusted by financial regulators and align with frameworks like NIST that Fannie Mae's cybersecurity supplement references. The MSP that manages those tools under a Microsoft 365 Direct-Bill relationship is operationally accountable to Microsoft for how the tenant is configured.

M365 Guardian is ABT's operating model for Microsoft 365 environments at regulated financial institutions. It hardens tenant configurations across Microsoft Entra ID, Microsoft Intune, Microsoft Defender, and Microsoft Purview, monitors for compliance drift continuously, delivers security and productivity insights to the lender's IT and compliance leadership, and coordinates incident response through Microsoft Sentinel. For mortgage lenders, M365 Guardian ensures that the Microsoft 365 environment underlying loan origination workflows meets regulatory expectations for data protection, access controls, and audit trail completeness, with Microsoft Purview Audit Premium providing the time-stamped recordkeeping evidence that Fannie Mae cybersecurity oversight and state mortgage examinations expect.