In This Article

- Where Mortgage Operations Stand in 2026

- MortgageWorkSpace: ABT's Productized Microsoft 365 Mortgage Platform

- Automation and Workflow Engines

- AI in Underwriting and Document Processing

- Cloud Infrastructure for Mortgage Companies

- The Data Spine: MortgageExchange, Microsoft 365 Copilot, and M365 Guardian

- Security Technology That Matters

- How to Adopt Without Disruption

- Frequently Asked Questions

AI adoption in mortgage lending jumped from 15% in 2023 to 38% in 2024. Lenders using AI report operational cost reductions of 30-50% and loan closures 2.5 times faster than industry averages. The mortgage industry spent decades resisting technology changes. That resistance is now a competitive liability.

This is not about replacing loan officers with algorithms. It is about eliminating the manual processes that consume 60% of a mortgage professional's day: data entry, document chasing, status updates, and compliance checks that a system should handle automatically.

This guide covers the specific technologies reshaping mortgage operations, what they cost, what they deliver, and how mortgage companies of any size can adopt them without disrupting their current business. Access Business Technologies operates Microsoft 365 tenants for 750+ financial institutions, including independent mortgage banks, mortgage brokers, and the mortgage divisions inside community banks and credit unions.

Where Mortgage Operations Stand in 2026

The mortgage industry has a technology gap. A 2025 Cognizant-HFS study of 257 non-bank lenders found that 42% are ready for real-time integration with ecosystem partners. The rest are still playing catch-up. Legacy constraints and tech debt are the primary blockers. See also our breakdown of The Benefits of Mortgage Management with MISMO Certified Partners.

The gap shows up in four areas.

Manual processes that should be automated. Loan officers still manually key borrower data from PDFs into their LOS. Processors still email underwriters asking for status updates. Closers still re-enter data that already exists in the origination file.

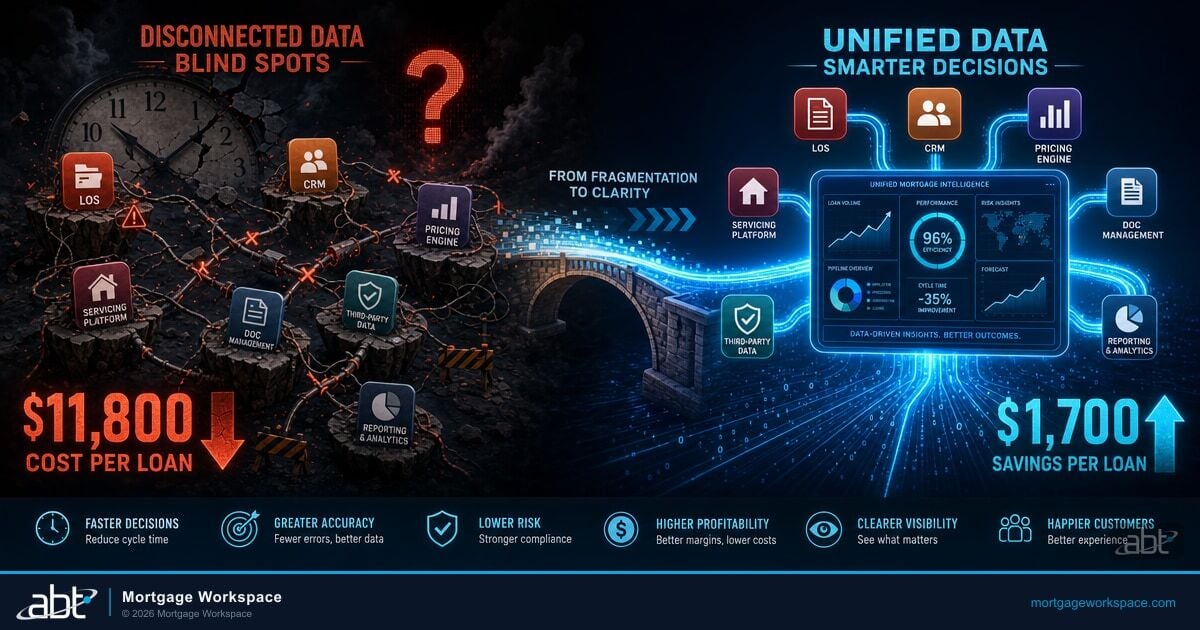

Disconnected systems. The average mortgage company uses a LOS, a CRM, an accounting system, a document management platform, and an email system. Few of them talk to each other. Data gets entered multiple times, creating inconsistencies and compliance risk.

Security lagging behind threats. Many mortgage companies still run endpoint antivirus as their primary security layer. Meanwhile, attackers use AI-generated phishing emails that bypass traditional detection. The threat model has changed. The defenses have not kept pace.

Borrower expectations outpacing capability. Consumers can apply for a credit card in 3 minutes on their phone. They expect a similar experience from their mortgage lender. Traditional mortgage processes take 47 days on average to close. That gap creates frustration and lost business.

MortgageWorkSpace: ABT's Productized Microsoft 365 Mortgage Platform

The technology fix for the four-part gap above is not a single product. It is an opinionated stack tuned to how mortgage operations actually work. ABT productized that stack as MortgageWorkSpace, the mortgage-vertical brand under which Access Business Technologies manages Microsoft 365 tenants, hosts mortgage workloads in Azure, and delivers the security and integration layer purpose-built for independent mortgage banks, brokers, and bank mortgage divisions. MortgageWorkSpace is not a feature inside Microsoft 365. It is the dual-brand mortgage-industry productization of the Microsoft 365 + Azure platform, configured for LOS connectivity, NPI handling, FFIEC and GLBA examination readiness, and the document workflows that actually move loans from application to closing. Where vendor-default Microsoft 365 leaves a mortgage company to figure out which controls to apply, MortgageWorkSpace ships the configuration ABT has refined across 750+ FIs and applies it through a single managed-tenant relationship.

Automation: Eliminating Manual Work from the Loan Lifecycle

Automation in mortgage is not a single tool. It is a layer that sits on top of existing systems and handles the repetitive work.

Document Processing Automation

Intelligent Document Processing (IDP) uses optical character recognition and machine learning to extract data from scanned documents. Instead of a processor manually reading a W-2 and typing the numbers into the LOS, IDP reads the document, extracts the fields, and populates the system.

Rocket Mortgage's Rocket Logic system processes 1.5 million documents per month with 70% auto-identification, saving over 5,000 underwriter hours monthly. That is not theoretical. That is production volume at the largest mortgage originator in the country.

Workflow Routing

Automated workflow engines move loan files between departments based on rules. When a processor marks initial review complete, the file routes to underwriting automatically. When an underwriter issues conditions, the processor receives a task list without anyone sending an email.

The 2025 mortgage technology trend research from Consolidated Analytics identified workflow modernization as one of the top priorities for lenders heading into 2026, specifically citing the elimination of "stare and compare" tasks through rule engines and automated routing. We cover The Role of Predictive Analytics in Mortgage Risk Assessment in a companion piece.

Communication Automation

Power Automate and similar tools trigger notifications based on loan events. A rate lock expiration in 3 days. A document uploaded by a borrower. A condition cleared by underwriting. Each event sends the right notification to the right person without manual effort.

AI in Underwriting and Document Processing

AI goes beyond automation by making decisions based on patterns in data.

AI-Powered Underwriting

Freddie Mac estimated in 2025 that lenders fully utilizing AI-powered underwriting tools could save up to $1,500 per loan. AI underwriting analyzes borrower data against thousands of approval patterns, identifies risk factors that humans miss, and provides consistent decisions across every application.

The STRATMOR Group's 2024 Technology Insight Study showed AI and machine learning adoption among mortgage lenders growing rapidly, with the technology moving from experimental to foundational. Lenders reported using AI for income calculation, asset verification, and automated condition generation.

Intelligent Document Recognition

AI document processing goes beyond OCR. It understands context. It knows that a number in the top-right corner of a W-2 is an employer ID, not a Social Security number. It identifies missing pages, detects alterations, and flags inconsistencies between documents that a processor might miss.

Financial institutions using AI document processing report an 85% reduction in document verification time. For a mid-sized lender processing 500 loans per month, that translates to hundreds of hours reclaimed for higher-value work.

Fraud Detection

AI fraud detection analyzes borrower data in real time, comparing applications against known fraud patterns. It flags suspicious income documentation, identifies synthetic identities, and catches misrepresentation before a loan reaches underwriting.

Lenders using AI fraud detection report a 50% reduction in fraud cases. The technology pays for itself by preventing even a single fraudulent loan from closing.

Cloud Infrastructure for Mortgage Companies

Cloud is not a trend for mortgage companies. It is a requirement. A McKinsey report found that cloud adoption in financial institutions can reduce operational costs by up to 30%.

Why Cloud Matters for Mortgage

Scalability. When rates drop and applications surge, cloud infrastructure scales automatically. No emergency hardware purchases. No capacity planning that assumes normal volume.

Remote access. Loan officers work from borrower homes, real estate offices, and their own dining tables. Cloud systems work from any location with an internet connection.

Automatic updates. Cloud platforms patch security vulnerabilities automatically. On-premise systems wait for an IT admin to schedule downtime and apply updates manually.

Disaster recovery. Cloud providers replicate data across multiple geographic regions. If a data center goes offline, your systems fail over automatically. Financial institutions report a 62.8% reduction in recovery time objectives after moving to cloud.

Microsoft 365 as the Foundation

For mortgage companies, Microsoft 365 is the logical cloud foundation. It provides email (Exchange Online), collaboration (Teams), document management (SharePoint), and security (Defender, Intune, Conditional Access) in a single platform designed for regulated industries. Microsoft 365 includes built-in compliance tools for FFIEC, GLBA, and SOC frameworks. As a Tier-1 Microsoft Cloud Solution Provider, ABT manages those Microsoft 365 tenants under delegated admin, configures them specifically for mortgage company requirements, and operates them as part of MortgageWorkSpace. Our guide to Document Security for Remote Mortgage Teams goes deeper on this.

The Data Spine: MortgageExchange, Microsoft 365 Copilot, and M365 Guardian

What turns MortgageWorkSpace from a managed Microsoft 365 environment into a mortgage operating platform is the combination of three ABT-operated layers sitting on top of Microsoft. MortgageExchange is the data spine, the custom integration product that connects an LOS (Encompass, Calyx, OpenClose, BytePro) to the core banking system or general ledger that closes the loan, so application data, conditions, fees, and funding instructions move once and stay synchronized across every system that needs them. Microsoft 365 Copilot is the AI layer on top of that synchronized data, embedded in Outlook, Word, Excel, and Teams where loan officers, processors, and underwriters already work, surfacing borrower context, drafting condition responses, summarizing email threads, and pulling pipeline reports without anyone leaving their inbox. M365 Guardian is the governance layer, ABT's operating model on top of Microsoft Entra ID, Defender, Purview, Intune, and Sentinel that keeps NPI inside the tenant, blocks copy-paste of borrower data into consumer AI, holds the audit trail FFIEC and GLBA examiners expect, and produces evidence on demand. Together, MortgageExchange supplies the data, Microsoft 365 Copilot uses it, and M365 Guardian protects it. Each layer is configured once at the MortgageWorkSpace level and applied across every mortgage tenant ABT operates.

Security Technology That Matters for Mortgage

Mortgage companies are high-value targets. They handle Social Security numbers, bank account details, and financial documents for thousands of borrowers. Here is what the security stack should include.

Zero Trust architecture. Never trust, always verify. Every login, every device, every access request is authenticated and authorized. This replaces the old model of "inside the firewall equals trusted."

Endpoint Detection and Response (EDR). Microsoft Defender for Endpoint monitors every device for suspicious behavior. It does not just scan for known viruses. It detects unusual patterns like a processor's workstation suddenly exfiltrating data at 2 AM.

Email protection. Microsoft Defender for Office 365 blocks phishing attacks, malware attachments, and business email compromise attempts. AI-powered detection catches sophisticated attacks that rule-based filters miss.

Identity protection. Microsoft Entra ID Conditional Access policies restrict login based on location, device compliance, and risk level. If a loan officer's credentials appear for sale on the dark web, the system forces a password reset before the next login.

Continuous monitoring. Security is not a project. It is an ongoing operation. M365 Guardian, ABT's 24/7 managed security overlay on Microsoft Sentinel and the Defender suite, monitors your environment around the clock, investigates alerts, and responds to threats before they become breaches.

How to Adopt New Technology Without Disrupting Operations

The biggest mistake mortgage companies make with technology adoption is trying to change everything at once. The second biggest is waiting until the current system fails.

Start with the foundation. Get your cloud foundation right first. Move to a managed Microsoft 365 tenant under a Tier-1 Cloud Solution Provider. Configure security baselines. Train your team. This is the platform everything else builds on, and it is the MortgageWorkSpace starting point.

Add automation layer by layer. Start with document processing automation because the ROI is fastest. Then add workflow routing through MortgageExchange to connect your LOS to your core. Then add Microsoft 365 Copilot for the AI productivity layer. Each step compounds the efficiency gains of the previous one.

Evaluate AI where it matters most. Underwriting automation and fraud detection deliver the clearest ROI. Start there. Evaluate results after 90 days before expanding to other AI applications.

Choose partners over products. A tool without implementation expertise is shelfware. ABT, the Tier-1 Microsoft CSP that operates MortgageWorkSpace for 750+ financial institutions, deploys, configures, and manages the entire stack (Microsoft 365, MortgageExchange, Microsoft 365 Copilot, and M365 Guardian) as a single managed relationship.

Talk to a Mortgage IT Specialist

Technology transformation does not start with buying software. It starts with understanding where your current operations are losing time, money, and competitive position. A 30-minute conversation with ABT maps your current Microsoft 365 and LOS footprint, identifies the integration gaps MortgageExchange would close, and outlines what MortgageWorkSpace with Microsoft 365 Copilot and M365 Guardian would cover. No commitment, no quote, no obligation.

Frequently Asked Questions

AI in mortgage lending is used for automated document processing that extracts data from tax returns, pay stubs, and bank statements; AI-powered underwriting that analyzes borrower risk patterns and generates approval recommendations; fraud detection that identifies synthetic identities and misrepresentation in real time; and workflow automation that routes loan files between departments based on completion status and priority rules. Inside MortgageWorkSpace, Microsoft 365 Copilot delivers the conversational AI layer (drafting condition responses, summarizing pipelines, surfacing borrower context) directly inside Outlook, Word, Excel, and Teams where mortgage staff already work.

Costs vary by scope. Microsoft 365 Business Premium starts at approximately $22 per user per month, and Microsoft 365 Copilot Business adds on top of that. LOS platform subscriptions range from five figures to six figures annually depending on loan volume and features. AI document processing tools are typically priced per document or per loan. MortgageExchange (ABT's LOS-to-core integration product) is sized to the lender's volume and the number of systems integrated. The total investment depends on company size, but lenders implementing the MortgageWorkSpace stack report operational cost reductions of 30-50% that typically offset the technology investment within the first year.

AI replaces tasks, not roles. It automates data entry, document verification, and routine compliance checks. Loan officers spend more time advising borrowers, building referral relationships, and handling complex loan scenarios that require human judgment. The Cognizant-HFS 2025 study found that lenders expect a 9% increase in full-time employees despite automation gains, indicating a shift toward tech-augmented roles rather than job elimination. Microsoft 365 Copilot inside MortgageWorkSpace is built to augment the loan officer's day, not replace it.

Start with the cloud foundation. Move to a managed Microsoft 365 tenant under a Tier-1 Cloud Solution Provider so the security, compliance, and collaboration baseline is set correctly from day one. Configure compliance tools for FFIEC, GLBA, and state requirements. Once the foundation is stable, add automation layers: MortgageExchange for LOS-to-core integration first because the operational ROI is fastest, then Microsoft 365 Copilot for the AI productivity layer, then M365 Guardian for the 24/7 security and audit overlay. Working with a managed IT partner that specializes in mortgage technology (MortgageWorkSpace operates this stack for 750+ financial institutions) accelerates adoption and reduces risk.

MortgageWorkSpace is ABT's productized Microsoft 365 mortgage platform. It is the mortgage-vertical brand under which Access Business Technologies manages Microsoft 365 tenants for mortgage lenders, hosts mortgage workloads in Azure, and delivers the integration and security layer purpose-built for independent mortgage banks, mortgage brokers, and bank mortgage divisions. Inside MortgageWorkSpace, MortgageExchange is the LOS-to-core data spine, Microsoft 365 Copilot is the AI productivity layer, and M365 Guardian is the 24/7 security and compliance operating model. The combination is the mortgage-industry productization of the Microsoft 365 plus Azure platform that vendor-default Microsoft 365 alone does not deliver.