In This Article

- The Interface Problem in Mortgage Lending

- MortgageWorkSpace: ABT's Pre-Built Microsoft Mortgage Workflow

- Interface Design Patterns That Accelerate Closings

- Embedding Compliance Into the Mortgage Workflow

- Borrower-Facing Interface Design That Reduces Abandonment

- MortgageExchange: The LOS-to-Core Bridge Behind a Cleaner Workflow

- Mortgage BI: Measuring the Cycle-Time Impact You Just Bought

- ROI Framework for Interface Modernization

- Frequently Asked Questions

A major Alberta credit union replaced a 28-year-old mortgage system with a redesigned interface. Application times dropped from 60 minutes to under 15. User satisfaction reached 90 percent. Adoption was immediate because the system was built around the workflows staff actually use, not the workflows a vendor imagined.

That case study, published by Lantern Studios, captures the core problem in mortgage interface design. The technology exists to move fast. Most lenders run fragmented systems that force staff to re-enter data, toggle between applications, and manually track compliance requirements. The interface itself creates the delays.

An EY survey found that 63 percent of consumers prefer using an online mortgage process, with 58 percent saying online application availability affects which lender they choose. Borrowers want speed. Regulators want accuracy. Your interface has to deliver both. Below is the architecture that actually delivers, the pre-built Microsoft platform Access Business Technologies ships for mortgage operations, and the dashboards that prove the cycle-time impact after rollout.

Why ABT Runs This Workflow for Mortgage Companies

- MortgageWorkSpace packages the connected Microsoft mortgage workflow as a managed service. The architecture in this article is what ships in the box, not a six-month consulting engagement to wire up six Microsoft products yourself.

- MortgageExchange closes the LOS-to-core integration gap Microsoft does not solve. Funded loan data flows from Encompass, Byte, LoanSoft, or Mortgage Cadence to Fiserv DNA, Symitar Episys, Jack Henry SilverLake, or Corelation KeyStone without re-entry.

- Mortgage BI publishes the Power BI dashboard set ABT pre-builds for mortgage operations, so cycle-time, turn-time, pull-through, and compliance scorecards work the day you go live, not three months into a custom build.

Access Business Technologies manages Microsoft 365 tenants for more than 750 financial institutions, including community banks, credit unions, and independent mortgage banks. ABT is the largest Tier-1 Microsoft Cloud Solution Provider primarily dedicated to financial services. The three ABT capabilities that turn the design patterns below into a working operation are MortgageWorkSpace, MortgageExchange, and Mortgage BI, layered on top of a Microsoft 365 tenant ABT manages as a Tier-1 Direct-Bill Cloud Solution Provider.

The Interface Problem in Mortgage Lending

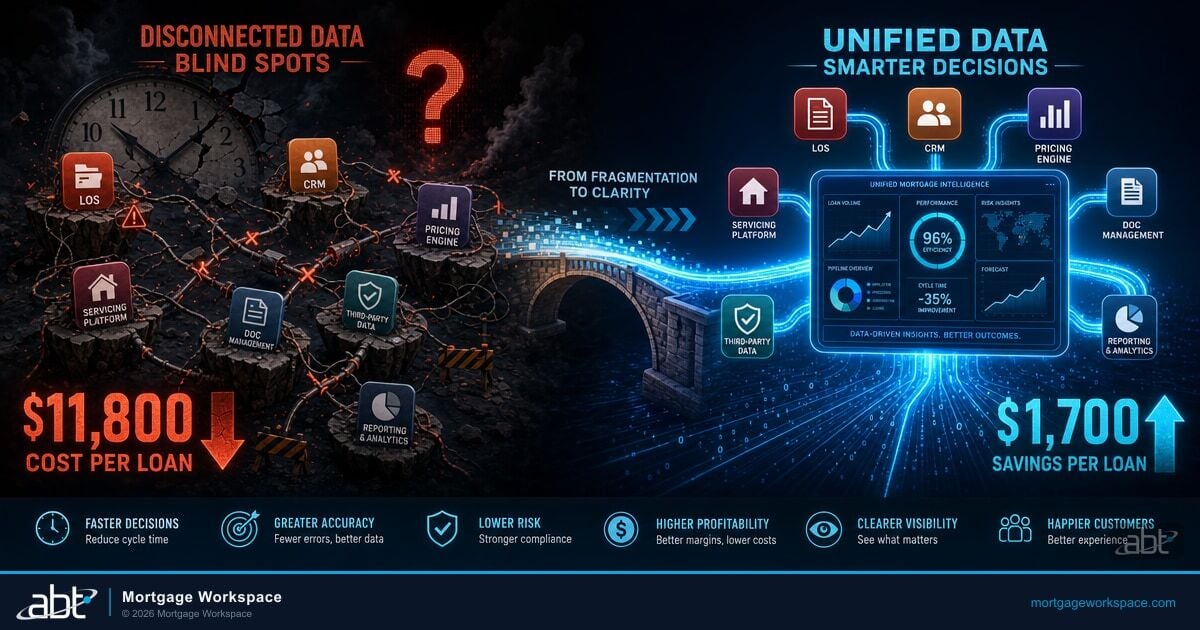

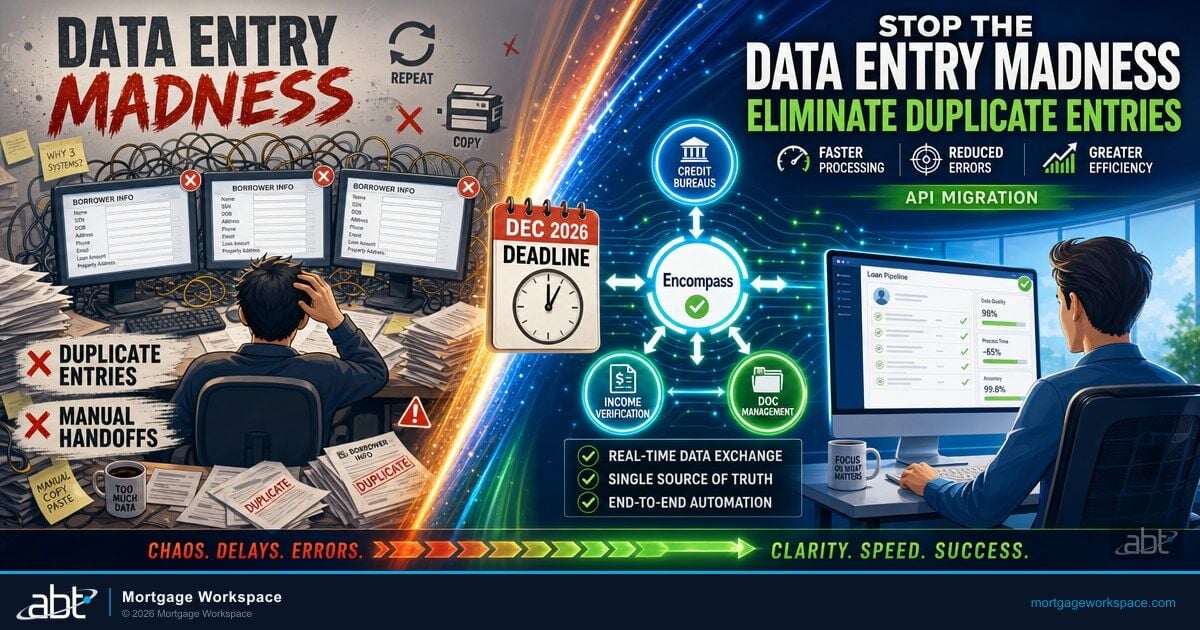

Most mortgage workflows suffer from the same structural flaw: systems that do not talk to each other. The loan origination system holds loan data. The document management platform holds files. The CRM holds borrower communications. The compliance tool tracks disclosures. Staff toggle between all four, manually transferring information and hoping nothing falls through.

Sourcepoint's analysis nails the diagnosis: the industry has digitized the front end while leaving the back office in chaos. Borrowers see a polished application form. Behind it, processors manually route files, underwriters hunt for documents across systems, and compliance teams discover TRID violations the workflow should have prevented.

The fix is not better-looking software. It is a connected workspace where every interface, from the borrower portal to the processing queue, shares the same data layer and enforces the same rules. When the loan origination system, document platform, and compliance tools operate on the same data, manual handoffs disappear and error rates drop.

MortgageWorkSpace: ABT's Pre-Built Microsoft Mortgage Workflow

MortgageWorkSpace is ABT's productized Microsoft 365 platform for mortgage operations. The architecture described throughout this article ships pre-configured: a Microsoft 365 tenant set up for mortgage work, integrated to the loan origination system, layered with mortgage-specific Microsoft Teams channels and Microsoft SharePoint sites, secured by the M365 Guardian operating model, and supported by ABT engineers who have done this for hundreds of lending shops.

A mortgage company that licenses MortgageWorkSpace gets the integrated stack as a managed service. Microsoft Teams channels are organized per loan officer and per loan, not as a blank tenant your team has to design from scratch. SharePoint document libraries carry mortgage-specific metadata columns (loan type, property type, condition status, lock expiration). Microsoft Power Automate flows route documents between Teams, SharePoint, and the loan origination system without manual handoffs. Microsoft Entra ID Conditional Access policies enforce MFA for loan officers and processors. Microsoft Purview retention policies bind to the seven-year floor under most state mortgage broker recordkeeping rules. Microsoft Defender for Office 365 watches the email surface where wire fraud and business-email-compromise attempts target closing funds.

The point of the platform is not that Microsoft sells these products. They are licensed in any reasonably configured Microsoft 365 tenant. The point is that someone has to configure them against a mortgage-specific baseline, integrate them to the loan origination system, and operate them every day. That work is what MortgageWorkSpace packages. The article The Blueprint for a Fully Connected Microsoft Mortgage Workflow walks through the stage-by-stage architecture in depth. This article focuses on the interface design patterns that turn the architecture into a measurable cycle-time win.

Interface Design Patterns That Accelerate Closings

Single Data Layer Architecture

Speed comes from design that treats data as an asset, not something to be re-entered. When every system in your mortgage workflow reads from and writes to the same data layer, updates happen once and propagate everywhere. Loan officers see verified borrower data without re-keying it. Processors see document status without checking a separate system. Underwriters see the complete file without requesting transfers. Inside a MortgageWorkSpace deployment, that data layer is Microsoft Dataverse and SharePoint Online, with Microsoft Power Automate flowing data into and out of the loan origination system through MortgageExchange.

Role-Based Interface Design

Loan officers, processors, underwriters, and compliance staff each need different views of the same data. A well-designed mortgage workspace gives each role exactly the information and actions they need, nothing more. This reduces cognitive load, speeds decision-making, and prevents errors from information overload. Microsoft Power Apps inside the MortgageWorkSpace deployment delivers the per-role screens without forcing a custom development engagement for every change.

The Alberta credit union case study proved this approach. By designing screens around actual user workflows rather than system architecture, they reached 95 percent interface approval and eliminated the training barrier that killed previous implementations.

Micro-Interaction Design for Borrowers

Borrowers abandon applications when the interface asks for too much at once. Break the process into small, completable steps. Show progress. Provide instant feedback on every input. When a borrower uploads a document, confirm receipt within seconds and tell them exactly what happens next.

Research from Ocrolus shows borrowers compare the mortgage process to universally disliked experiences. The frustration stems from opacity: borrowers do not know where their application stands or why they are being asked for the same information again. Transparency at every step fixes the experience.

Automated Workflow Routing

Manual routing is where loans stall. A smart workflow engine automatically routes files to the next person in the pipeline based on loan type, complexity, and team capacity. Exceptions get flagged and escalated. Routine files move without human intervention. Microsoft Power Automate inside MortgageWorkSpace is the routing engine, with Microsoft Teams notifications driving the human in the loop.

Embedding Compliance Into the Mortgage Workflow

Make compliance invisible by building it into the interface. The system should prevent invalid actions rather than flag them after the fact.

That means TRID timing requirements are tracked by the system, not by a spreadsheet. Disclosure delivery deadlines trigger automated actions. Required fields prevent file advancement until they are complete. Compliance checks run in the background at every stage, and the interface simply will not let a file move forward with unresolved issues. Microsoft Purview Audit logs preserve the time-stamped trail, and Microsoft Purview retention policies bind tamper-evident retention to the mailboxes, sites, and channels where mortgage records live.

The result is fewer audit findings, faster closings, and less time spent on manual compliance reviews. Deloitte's research shows AI-driven automation reduces compliance errors to below 2 to 3 percent, compared to 10 to 15 percent with manual processes.

For operations managers, this approach transforms compliance from a bottleneck into a speed advantage. Files that pass embedded compliance checks move faster through underwriting because they arrive clean. Files with issues get caught early, when fixes are simple, rather than at closing, when they cause delays. See Always Audit-Ready: Using Encompass and Calyx to Keep Compliance Locked Down for the loan-origination-system-side controls that pair with the Microsoft tenant work above.

Borrower-Facing Interface Design That Reduces Abandonment

The mortgage application abandonment rate sits between 75 and 80 percent. Most of that abandonment happens because the interface creates friction the borrower cannot resolve.

Effective borrower-facing interfaces share common patterns:

Show only what is needed at each step. Do not present 20 fields when 5 will move the borrower forward.

Flag errors as they happen, not after submission. If a Social Security number is wrong, say so immediately.

Ask for specific documents based on the borrower's profile. A W-2 employee does not need to see business income documentation requests.

Borrowers start on desktop and finish on mobile. State preservation across devices is not optional.

Build language options into the interface, not as an afterthought. Borrower-facing platforms with embedded multilingual support expand your addressable market.

Borrowers should see what step they are on, what is pending, and what the next decision point looks like. Hidden status is the largest single predictor of abandonment.

Industry research shows that 79 percent of mortgage professionals rate platforms that consolidate escrow-related tasks into one system as extremely valuable. That same consolidation principle applies to borrower interfaces: fewer systems, fewer logins, fewer places where the process can break.

MortgageExchange: The LOS-to-Core Bridge Behind a Cleaner Workflow

A clean interface depends on data that has already been reconciled across systems. The integration most mortgage companies stumble on is the bridge between the loan origination system and the core banking platform. Your loan origination system holds the loan in progress. Your core holds the borrower as a depositor or member, the funded loan as an asset on the balance sheet, and the servicing record. Without a bridge between the two, mortgage operations and retail banking operations are still two separate systems your staff reconciles by hand.

MortgageExchange is ABT's custom interface product that closes that gap. It pushes funded-loan data from the loan origination system into the core as a new loan record, creates the borrower-as-member or depositor link, and flows servicing data back to the loan origination system for refinance and cross-sell opportunities. Inside a MortgageWorkSpace deployment, MortgageExchange is part of the platform.

| Loan origination system | Core banking platform | What MortgageExchange handles |

|---|---|---|

| ICE Mortgage Technology Encompass | Fiserv DNA, Symitar Episys, Jack Henry SilverLake, Corelation KeyStone | Pushes funded-loan data to the core as a new loan record, creates the borrower-as-member or depositor link, and flows servicing data back for refinance and cross-sell opportunities. |

| Byte Software ByteSoftware | Fiserv DNA, Symitar Episys, FIS Horizon | Maps loan codes between Byte and the core, syncs payment history once the loan is on the books, and feeds delinquency and prepayment signals back to the loan officer. |

| LoanSoft, Mortgage Cadence | Multiple cores supported | Bidirectional sync of borrower demographics, loan product attributes, funding status, and servicing data, with mortgage-specific field mapping the generic loan-origination-system-to-core connectors do not handle. |

The reason this matters for interface design: without the LOS-to-core bridge, the loan officer working in the mortgage workspace cannot see whether the borrower is already a depositor at the same institution, and the retail banker cannot see whether the depositor is taking a mortgage with the same institution. The cross-sell conversation never happens. The data ABT customers report most often as the eye-opener after a MortgageWorkSpace deployment is how many mortgage borrowers were already members or depositors and how many cross-sell opportunities were sitting in plain sight, invisible to both sides. The article Integrating LOS and CRM Platforms Without Breaking Your Data Stack covers the data-stack consequences of getting that integration wrong.

Mortgage BI: Measuring the Cycle-Time Impact You Just Bought

An interface redesign is only as credible as the dashboards that measure its impact. Two months after rollout, the CFO will ask whether the cycle-time gains stuck. The chief lending officer will ask which loan officers are using the new flow and which are working around it. The compliance officer will ask whether disclosure deadlines are being hit more reliably than before. None of those questions get answered without a reporting layer that watches the pipeline in real time.

Mortgage BI is the Microsoft Power BI semantic model and dashboard pack ABT publishes as part of MortgageWorkSpace. It ships pre-built against the mortgage data model so working reporting is live on day one rather than three months into a custom build. The pre-built dashboards include:

- Pipeline view. Every active loan by stage, loan officer, product type, and expected closing date. Color-coded indicators flag loans approaching rate lock expiration or compliance deadlines.

- Turn-time analysis. Average days in each stage by loan officer, product type, and branch. Identifies which stages slow down and whether the bottleneck is people, process, or technology. This is where the cycle-time win from your interface redesign shows up as a measurable number.

- Pull-through rates. What percentage of applications become funded loans, broken down by source channel. Shows which referral partnerships and marketing campaigns actually produce revenue.

- Compliance scorecard. Document completion rates, condition clearance times, and disclosure timing. A red, yellow, green view gives compliance officers immediate visibility into potential audit findings before the examiner arrives.

The dashboards refresh automatically from live Microsoft Dataverse and loan origination system data. The Business Intelligence for Mortgage Companies practical implementation guide covers the data-model decisions in depth, and Maximizing Profitability Through Mortgage Business Intelligence explains how the resulting dashboards change branch and loan-officer accountability conversations after rollout.

ROI Framework for Interface Modernization

Track these metrics inside Mortgage BI to build the business case and prove the impact of the redesign:

- Processing time reduction. Connected interfaces typically cut cycle times 30 percent or more. The Alberta credit union case study showed a 75 percent reduction in application time alone.

- Application abandonment. Target 25 to 40 percent reduction through better borrower-facing design.

- Manual touches per loan. Count data re-entry events. Each one adds cost and error risk. Target 50 to 60 percent reduction.

- Compliance findings per quarter. Embedded compliance checks reduce audit findings by 50 percent or more.

- Staff satisfaction. Track NPS or satisfaction scores for internal users. The Alberta credit union reached 90 percent satisfaction, up from widespread frustration with the old system.

Example calculation. If your team processes 2,000 loans per year and interface improvements save six hours of labor per loan at $60 per hour, that is $720,000 in annual labor savings alone, before counting compliance cost avoidance and reduced abandonment.

Your interfaces define your speed. Fragmented systems force manual workarounds. A connected workspace lets your team focus on lending instead of fighting technology.

Key Takeaway

The lenders closing fastest in 2026 are not running better individual tools. They run integrated workspaces where every system shares data, every interface matches its user, compliance happens automatically, and dashboards prove the cycle-time impact in real time. ABT packages that integrated workspace as MortgageWorkSpace, with MortgageExchange handling the loan-origination-system-to-core integration and Mortgage BI handling the measurement layer, on top of a Microsoft 365 tenant ABT manages as a Tier-1 Direct-Bill Cloud Solution Provider.

Build Your Connected Mortgage Workflow With ABT

Designing screens around the people who use them, embedding compliance into the workflow, and proving the cycle-time impact requires expertise in the Microsoft stack and in mortgage operations. ABT manages Microsoft 365 tenants for more than 750 financial institutions and packages the connected mortgage workflow as MortgageWorkSpace, with MortgageExchange and Mortgage BI included. A 30-minute conversation maps your current loan origination system, core, and Microsoft 365 footprint and outlines what a MortgageWorkSpace deployment would cover for your shop. No commitment, no quote, no obligation.

Frequently Asked Questions

Connected interfaces eliminate the manual data transfers between systems that cause most delays. When the loan origination system, document platform, and compliance tools share a single data layer, staff stop re-entering information and start processing loans. Role-based views give each team member exactly what they need. Automated routing moves files without manual handoffs. One Alberta credit union cut application time from 60 minutes to 15 through interface redesign alone, and most lenders running a MortgageWorkSpace-style architecture report 30 percent or better cycle-time improvements within the first two quarters after rollout.

A mortgage workspace is an integrated environment where all lending tools share a common data layer and enforce consistent business rules. A loan origination system is one component. The workspace connects the loan origination system to document management, CRM, compliance tools, and borrower portals through APIs and shared data, creating a unified platform where information flows without manual intervention between systems. MortgageWorkSpace is ABT's productized Microsoft 365 platform for that integrated workspace, with MortgageExchange handling the loan-origination-system-to-core bridge and Mortgage BI handling the reporting layer.

Embedded compliance builds regulatory requirements into the interface itself. The system tracks TRID disclosure timelines, prevents files from advancing with incomplete data, and runs compliance checks at every stage. This catches issues early when fixes are simple rather than at closing when they cause delays. Inside a MortgageWorkSpace deployment, Microsoft Purview Audit preserves the time-stamped trail and Microsoft Purview retention policies hold the records under the seven-year floor most state mortgage broker rules expect. Lenders running embedded compliance report 50 percent fewer audit findings compared with manual review processes.

Abandonment rates of 75 to 80 percent stem from interface friction. Borrowers quit when forms ask for too much at once, when they cannot see application status, when they receive vague document requests, or when progress is lost switching between devices. Effective interfaces use progressive disclosure, real-time validation, specific document requests, and cross-device continuity to reduce abandonment by 25 to 40 percent. A Microsoft Power Apps borrower portal inside MortgageWorkSpace can deliver each of those patterns without a custom development engagement for every change.

A clean interface depends on data that has already been reconciled across systems. Without the loan-origination-system-to-core bridge, the loan officer working in the mortgage workspace cannot see whether the borrower is already a depositor at the same institution, and the retail banker cannot see whether the depositor is taking a mortgage with the same institution. MortgageExchange is ABT's custom interface product that connects Encompass, Byte, LoanSoft, or Mortgage Cadence to cores including Fiserv DNA, Symitar Episys, Jack Henry SilverLake, and Corelation KeyStone, so funded loan data flows to the core and servicing data flows back without manual re-entry. Inside MortgageWorkSpace, that integration is part of the platform.

The dashboards are how. Mortgage BI is the Microsoft Power BI dashboard set ABT pre-builds for mortgage operations as part of MortgageWorkSpace. It ships against the mortgage data model so working reporting is live on day one, with pipeline view, turn-time analysis by stage and loan officer, pull-through rates by source channel, and a compliance scorecard. Two months after a redesign, the CFO can look at turn-time analysis and see whether the cycle-time gains stuck, the chief lending officer can see which loan officers are using the new flow, and the compliance officer can see whether disclosure deadlines are hit more reliably than before.