In This Article

Freddie Mac's 2025 Cost to Originate Study puts the average origination cost at $11,800 per loan for retail lenders in Q2 2025 - down from $13,400 in Q1, but still well above what most independent mortgage bankers can sustain. A significant portion of that cost traces back to disconnected workflows between systems that should be sharing data automatically.

In Part 1 of this series, we broke down three blind spots that LOS data misses: where processors lose hours, why underwriter output drops, and what stalls loan officer pipelines. This article picks up where that left off - what those blind spots actually cost, and what connecting your data looks like in practice.

The Real Cost of Data Blind Spots

Your LOS tracks what happened. How many loans closed. What's sitting in the pipeline. But it doesn't tell you why turnaround times are slipping or where your processors lose hours each day.

That gap between "what" and "why" is expensive. The waste hides in places your LOS can't see:

- Rekeyed data across LOS, CRM, and servicing platforms - every manual entry is a chance for errors that compound downstream

- Manual reconciliation when systems disagree on borrower info - staff burns hours verifying what should match automatically

- Delayed decisions because leadership can't see the full picture - by the time spreadsheets are assembled, the bottleneck has already shifted

Why the Cost Keeps Climbing

Technology now accounts for 10-18% of operating expenses at large lenders, according to the MBA's 2025 Market Outlook. But most of that spending goes to individual point solutions - not integration between them. Lenders are spending more on technology every year without solving the fundamental problem: their systems don't talk to each other.

Freddie Mac's research shows that lenders using LPA digital capabilities save approximately $1,700 per loan - a 13% increase in savings compared to 2024. That gap between digitally integrated lenders and everyone else isn't shrinking. It's widening.

How Disconnected Systems Drain Your Team

The Processor Stuck in Toggle Mode

David processes loans. His output dropped last month. The LOS shows fewer completions but doesn't explain the drop.

The real story: David spends 2 to 3 hours a day switching between Encompass, Outlook, and shared drives - fixing manual errors, tracking down documents, and double-checking compliance fields across disconnected systems. That's roughly 60 hours a month of lost productivity. Time that should go toward closing loans goes toward chasing data instead.

These delays ripple outward. Loan files stall. Underwriting backlogs grow. Borrowers who expected fast approvals start shopping elsewhere - and in a market where the average mortgage already takes 42 days from application to closing, every extra day of delay is a competitive risk.

The Underwriter Cleaning Up Upstream Mistakes

Maria is a senior underwriter. Her loan output fell 50% over three months. The numbers are visible. The cause isn't.

Maria spends most of her day correcting incomplete files - missing pay stubs, unverified borrower data, problems that should have been caught during processing. Every correction pushes back deadlines and frustrates borrowers waiting for updates.

Without visibility across the full loan workflow, leadership can't tell whether the problem started in sales, processing, or document collection. They end up guessing - and guessing wrong means investing in the wrong fix.

The Loan Officer Buried in Admin

Mark's conversion rates dropped. The LOS flags the decline but offers no context.

Mark spends hours on administrative tasks and chasing unqualified leads. Redundant processes eat into time he should spend closing deals and building borrower relationships. With disconnected systems, nobody can see how his time breaks down - or that the real problem isn't motivation but workflow friction.

Without Connected Data

- Leadership sees outcomes but not causes

- Fixes target symptoms, not root problems

- Staffing decisions based on guesswork

- Bottlenecks shift faster than reports can track

With Connected Data

- Time allocation visible by role and system

- Upstream errors traced to their source

- Capacity planning grounded in actual data

- Real-time dashboards replace stale spreadsheets

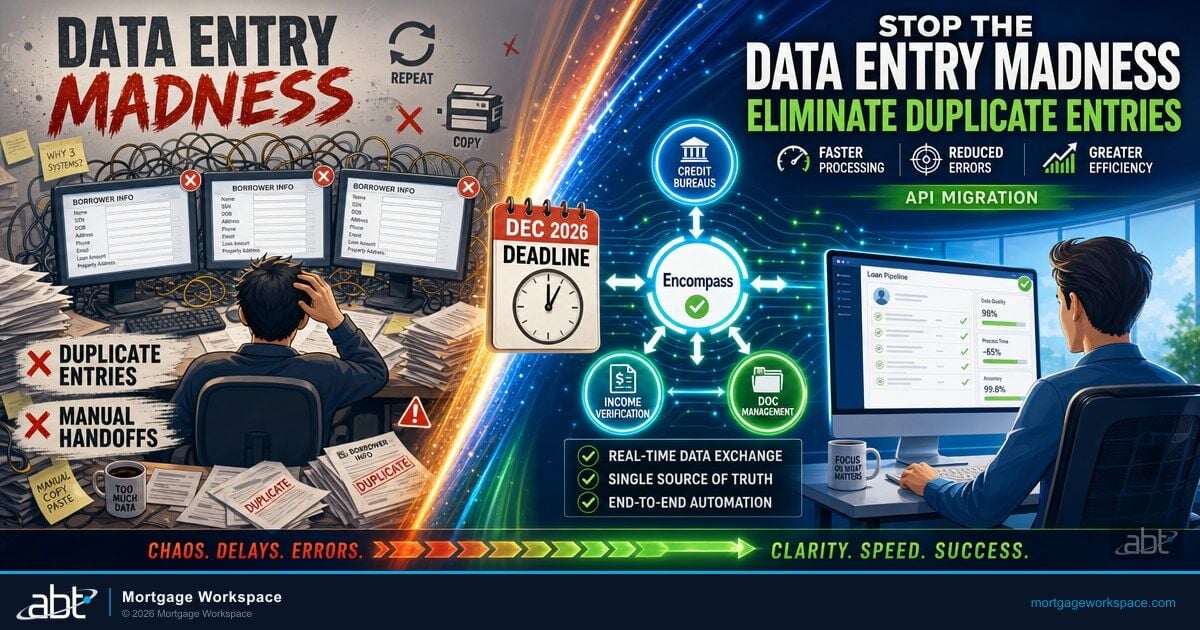

The DIY Integration Trap

When mortgage operations leaders realize their systems don't share data, the first instinct is to build a fix in-house. The IT team gets tasked with pulling data from the LOS, productivity tools, and financial systems into one central database.

This approach has a pattern that plays out the same way at lenders of every size:

The Plan

Connect the LOS, CRM, and financial systems through custom API integrations. Build dashboards that give leadership the cross-functional visibility they've been missing.

What Actually Happens

Integration takes months because each system uses different data formats and field naming conventions. Every software update breaks something. The IT team spends more time patching connections than analyzing results. By the time dashboards are usable, the original bottleneck has shifted - leadership is solving last quarter's problem with this quarter's data.

This isn't a failure of effort. It's a structural mismatch. General-purpose integration tools weren't built for the specific data relationships that mortgage operations depend on - LOS milestones mapping to processor activity, CRM touchpoints correlating with pipeline velocity, compliance requirements threading through every handoff.

That's why managed integration models exist. A mortgage-focused managed service provider already understands these data relationships and can deploy connected dashboards without the multi-month build-it-yourself timeline.

What Unified Data Actually Looks Like

Unified data doesn't mean one giant database. It means your systems share information automatically so that decisions happen faster.

Here's what changes when mortgage data flows freely:

| Capability | Before Integration | After Integration |

|---|---|---|

| Processor Visibility | See loan counts only | See time allocation across every system |

| Upstream Detection | Blame underwriters for delays | Trace delays to the specific processing step that caused them |

| Borrower Communication | Status unknown until someone checks manually | Real-time updates at every milestone |

| Compliance Readiness | Stitched-together spreadsheets for auditors | Single audit trail across all systems |

| Decision Speed | Weekly reports already stale by the time they're read | Live dashboards with drill-down by role, team, and loan type |

Freddie Mac's data confirms the impact: lenders using digital integration capabilities see shorter cycle times, reduced rework, and improved pull-through rates - with estimated savings of $1,700 per loan. That math works for credit unions, banks, and mortgage companies of every size.

The lenders who connect their data first won't just save money - they'll close faster, retain more borrowers, and make staffing decisions based on what's actually happening instead of what last month's spreadsheet suggested.

Audit-Ready Compliance

Regulators under GLBA, FTC Safeguards Rule, and state-level requirements expect data consistency across systems. Unified data creates a single audit trail instead of stitched-together spreadsheets - making compliance less of a fire drill and more of a standing capability. Tools like Power BI dashboards built for mortgage compliance turn regulatory requirements into real-time monitoring instead of quarterly scrambles.

Where to Start

You don't need to replace your LOS or rip out your tech stack. Start with three steps:

Three Steps to Connected Mortgage Data

- Map your data handoffs. Where does information move from one system to another? Every manual transfer is a potential failure point. List them all.

- Quantify the waste. Track how many hours your team spends rekeying data, reconciling mismatches, and chasing documents. Multiply by loaded labor cost. The number will be larger than you expect.

- Talk to a mortgage IT specialist. A managed service provider who understands LOS, CRM, and Microsoft 365 integration can connect your systems and deploy Mortgage BI dashboards without the multi-month build-it-yourself timeline.

Freddie Mac's Cost to Originate data makes the ROI clear: lenders using digital integration capabilities save $1,700 per loan with shorter cycle times and reduced rework. For a lender closing 1,000 loans a year, that's $1.7 million in recoverable margin - margin that's currently lost to disconnected systems.

Connect Your Mortgage Data. See the Full Picture.

Mortgage Workspace helps credit unions, banks, and mortgage companies connect their LOS, CRM, and employee data into unified dashboards - so leadership can act on causes, not just symptoms. No multi-month build. No custom API headaches.

Frequently Asked Questions

Data silos form when mortgage companies use separate systems for loan origination, document management, CRM, and servicing without integration between them. Each system stores borrower information independently, forcing staff to manually transfer data between platforms. Over time, different departments adopt their own tools, creating a patchwork of disconnected databases that cannot share information automatically.

Freddie Mac's 2025 Cost to Originate Study shows that lenders using digital integration capabilities save approximately $1,700 per loan compared to those relying on disconnected manual processes. With average origination costs at $11,800 per loan in Q2 2025, the gap between digitally integrated lenders and those still running on disconnected systems continues to widen each year.

Unified data creates a single audit trail across all systems, making it easier to demonstrate compliance with GLBA, FTC Safeguards Rule, and state-level regulations. When borrower information flows through connected platforms, lenders can track data lineage, maintain consistent records, and produce audit documentation without manually assembling reports from multiple disconnected sources.

Yes. Modern integration approaches connect existing systems through APIs and managed data pipelines rather than requiring full platform replacement. A mortgage-focused managed service provider can bridge LOS, CRM, document management, and Microsoft 365 environments. This approach preserves existing investments while eliminating manual data transfers between platforms.