Consolidated Analytics called it in late 2025: the mortgage industry is shifting from moving faster to working smarter. AI is no longer a pilot program. It is core infrastructure baked into underwriting, pricing, document review, and quality control. For mortgage companies running platforms built five years ago, that shift creates a hard deadline. Upgrade or fall behind.

In This Article

A Brief History of Mortgage Interface Evolution

Mortgage tech is a newer story than most people realize. Loan agreements in early America were settled with handshakes and handwritten ledgers. Federal programs like the FHA and GI Bill formalized the process by the mid-20th century, but the real technology shift came later.

The 1970s introduced securitization. The 1980s brought adjustable-rate products that required smarter tools. By the 1990s, digital banking pushed workflows from back-office systems to borrower-facing interfaces.

Then came the Loan Origination System. Platforms like Encompass and Calyx Gateway gave lenders the power to digitize nearly the entire loan lifecycle. That was the foundation. What is being built on top of it today looks nothing like 2010.

Key Innovations Reshaping Mortgage Interfaces

Digital and Mobile Application Platforms

Applications that once took hours in an office now complete in minutes from a kitchen table. According to Fannie Mae, 90% of homebuyers in 2024 reported interest in a more or fully digital mortgage process. Lenders who fail to deliver frictionless mobile experiences lose share to competitors who do.

AI and Machine Learning in Mortgage Underwriting

AI-driven underwriting models now analyze 10,000+ data points, including alternative data like utility payments, rental history, and cash flow patterns. A mid-sized US lender recently cut document verification time from 48 hours to under 4 hours after deploying AI-powered processing. Fannie Mae reports that 73% of lenders have adopted AI or machine learning tools for compliance reviews and anomaly detection.

The Consumer Financial Protection Bureau has made clear that existing fair lending laws apply to AI-driven credit decisions. Lenders must provide specific denial reasons even when algorithms make the call. Balancing speed with regulatory compliance is the defining challenge of 2026 mortgage technology. For ABT's fuller take, see How Mortgage POS Interfaces Speed Up Pre-Qualification in 2026.

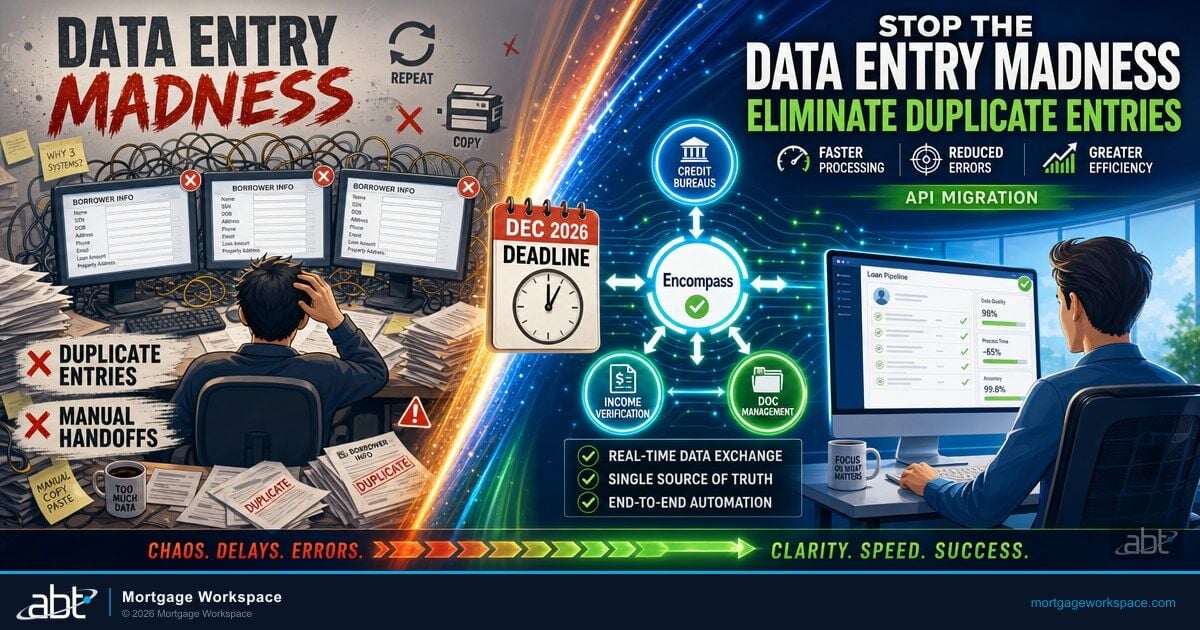

Mortgage Workflow Automation

Modern LOS platforms automate document collection, credit pulls, and compliance checks. Loan officers spend less time on data entry and more time on complex cases. Industry data shows automation has reduced mortgage processing errors by 35% across lenders who deploy it properly.

Tools like App Pilot take this further by guiding borrowers through each step of the application process with built-in validation. Fewer incomplete submissions. Less back-and-forth. Faster pipelines.

Integrated Compliance Tools

Regulations change fast. The CFPB continues updating mortgage data collection requirements. State-level rules from agencies like NYDFS add another layer. The best mortgage interfaces bake regulatory logic directly into the platform, auto-flagging data anomalies and tracking audit trails in real time.

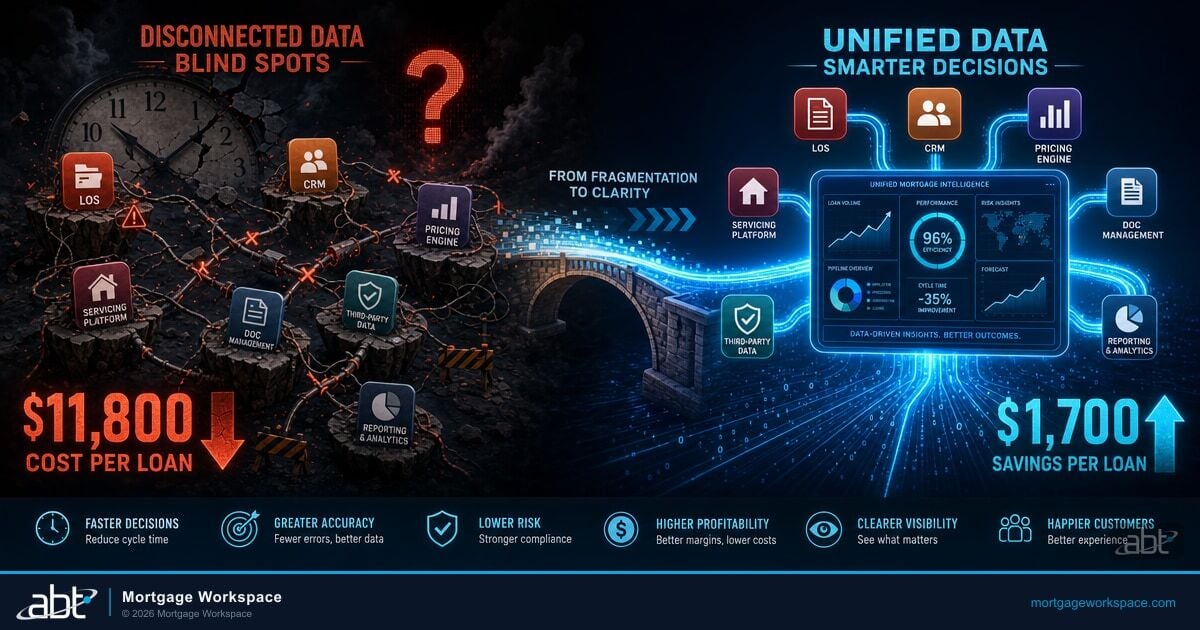

Data Analytics and Pipeline Visualization

Mortgage analytics dashboards spot application bottlenecks, monitor pipeline health, and flag conversion drop-off points. Lenders using integrated data-driven platforms have reduced operational cycle times by three days and increased gross profit per loan by $1,056, according to ICE Mortgage Technology. See also our breakdown of Mortgage Workflow Interface Design.

Guardian Productivity Insights adds another dimension to this picture, giving mortgage operations leaders visibility into how staff actually use technology across the lending workflow. When you can see where tools go underused and where bottlenecks form, you make targeted improvements instead of guessing.

The Mortgage Interface of 2030 Starts Now

Interfaces are evolving from processing tools into intelligent ecosystems designed to anticipate needs and reduce friction. Here is what mortgage companies should prepare for.

AI as Core Infrastructure

By 2030, AI will not just speed up underwriting. It will function as a co-pilot that analyzes borrower data in real time, flags risks before they reach underwriting, and adapts to new regulations without full system overhauls. Industry projections suggest fully automated loans will grow from single digits today to 30-40% of total volume. Complex cases will still require human review, but the ratio is shifting fast.

Real-Time Data and Open Banking

Open banking protocols and secure APIs will feed real-time financial data from bank accounts, tax returns, and payroll systems directly into the mortgage file. Document collection friction drops. Risk assessment accuracy goes up. The global digital mortgage market is projected to grow from $108.87 billion in 2024 to $747.69 billion by 2033 at a 23.12% CAGR, and API-driven workflows are the engine behind that growth.

Products like MortgageExchange already operate in this space, connecting LOS platforms to core banking systems, CRMs, and third-party data providers through standardized interfaces. As open banking matures, these integration layers become the connective tissue between every system in the lending stack. This connects closely to Interface Security Best Practices for Mortgage Application Platforms.

Blockchain for Security and Transparency

Blockchain-enabled interfaces promise tamper-proof records, clear audit trails, and instant verification of property data. Early adopters are piloting blockchain for eNotes and digital closings, cutting costs and reducing document fraud.

Mobile-First Experience

60% of borrowers already engage in mortgage-related activities via mobile devices. Expect mobile-first interfaces optimized for e-signatures, push notifications, and document uploads. The experience will feel as seamless as mobile banking.

Modular, API-First Platforms

The future belongs to LOS platforms that offer modular architecture with customizable integrations. ICE Mortgage Technology has set a December 2026 deadline for lenders to migrate from SDK-based customizations to API-driven workflows. Lenders who have already transitioned report an average benefit of $149 per loan from reduced latency and lower maintenance costs.

Cybersecurity as a Default Feature

Growing digital complexity brings increased risk. AI-driven threat detection, role-based access controls, encrypted document storage, and zero-trust architecture will become standard. Roughly half of all mortgage firms still do not regularly test their IT infrastructure for security weaknesses. That gap is shrinking as regulators tighten requirements.

Encompass, Calyx, and the LOS Landscape

Encompass by ICE Mortgage Technology focuses on full-suite digital origination, giving lenders a single platform from application to closing. Its growing marketplace of modular integrations and the push toward API-first architecture future-proofs the investment.

Calyx provides flexible LOS and product pricing engines, offering strong value for small to mid-sized lenders who prioritize scalability and compliance without enterprise-level complexity.

Neither system is static. Both are rolling out features for open banking, mobile-first experiences, and AI-driven underwriting. Choosing the right LOS, or fine-tuning the one you have, directly impacts your competitiveness for the next five years.

How to Prepare for the Mortgage Interface Revolution

Mortgage companies face both risk and opportunity. A wait-and-see approach means falling behind competitors with smarter tools. Start with these steps:

- Audit your current LOS, integrations, and compliance tools. Identify every SDK dependency before the December 2026 API migration deadline.

- Pilot AI-powered document processing and underwriting tools. Start with high-volume, repetitive tasks where the ROI is clearest.

- Require API compatibility in all new vendor relationships. Disconnected point solutions will fall behind integrated systems.

- Train staff on evolving compliance and data privacy requirements. CFPB, GLBA, FTC Safeguards Rule, and state regulations like NYDFS all apply.

- Build analytics and reporting into your pipeline. Track cycle times, conversion rates, and bottlenecks.

- Partner with an IT provider who understands both compliance and mortgage operations. Technology decisions made without regulatory context create risk.

Build Your Mortgage Technology Roadmap

The next five years will redefine what is possible in mortgage lending. Interfaces are now drivers of business reputation, compliance standing, and borrower loyalty. Companies that align their technology stack with the trends outlined here will close faster, serve borrowers better, and stay ahead of regulatory changes.

Talk to a mortgage IT specialist to map out your technology roadmap. Mortgage Workspace serves 750+ financial institutions with managed IT, Microsoft 365 governance, and deep mortgage technology integration including MortgageExchange, App Pilot, and Guardian Productivity Insights.

Is Your Interface Strategy Ready for Where Mortgage Is Headed?

The interfaces connecting your LOS, CRM, and core decide how fast you can adapt as the industry changes through 2030. MortgageWorkspace helps you build a roadmap that holds up instead of locking you into yesterday's stack.

Frequently Asked Questions

AI adoption, API-first architecture mandates from ICE Mortgage Technology, open banking protocols, and tightening regulatory requirements from the CFPB and state agencies are driving mortgage interface changes. Lenders face a December 2026 deadline to migrate SDK-based integrations to API-driven workflows, making interface modernization urgent rather than optional.

AI-powered underwriting analyzes thousands of data points including alternative data like rental payments and cash flow patterns to assess borrower risk faster than manual review. Lenders deploying AI document processing have reduced verification times from 48 hours to under 4 hours while improving accuracy and reducing processing errors by up to 35 percent.

Look for API-first architecture, modular integrations, automated compliance workflows, real-time data access, and mobile-first borrower interfaces. Platforms like Encompass and Calyx offer these capabilities, but the key differentiator is how well the LOS integrates with your CRM, document management, and analytics tools to create a connected ecosystem.

Open banking APIs enable real-time financial data to flow directly from bank accounts, tax records, and payroll systems into the mortgage file. This eliminates manual document collection, reduces verification delays, and improves risk assessment accuracy. Over 90 percent of financial institutions now rely on APIs to enhance customer experiences in lending workflows.