In This Article

- Why BI Matters More Than Ever for Mortgage Risk

- Catching Fraud Before It Costs You

- Building Smarter Borrower Risk Profiles

- Pipeline Visibility and Early Warning Systems

- How Guardian Ties BI Data to Tenant Security

- Using Market Intelligence to Anticipate Shifts

- Getting Started with Mortgage BI

- Frequently Asked Questions

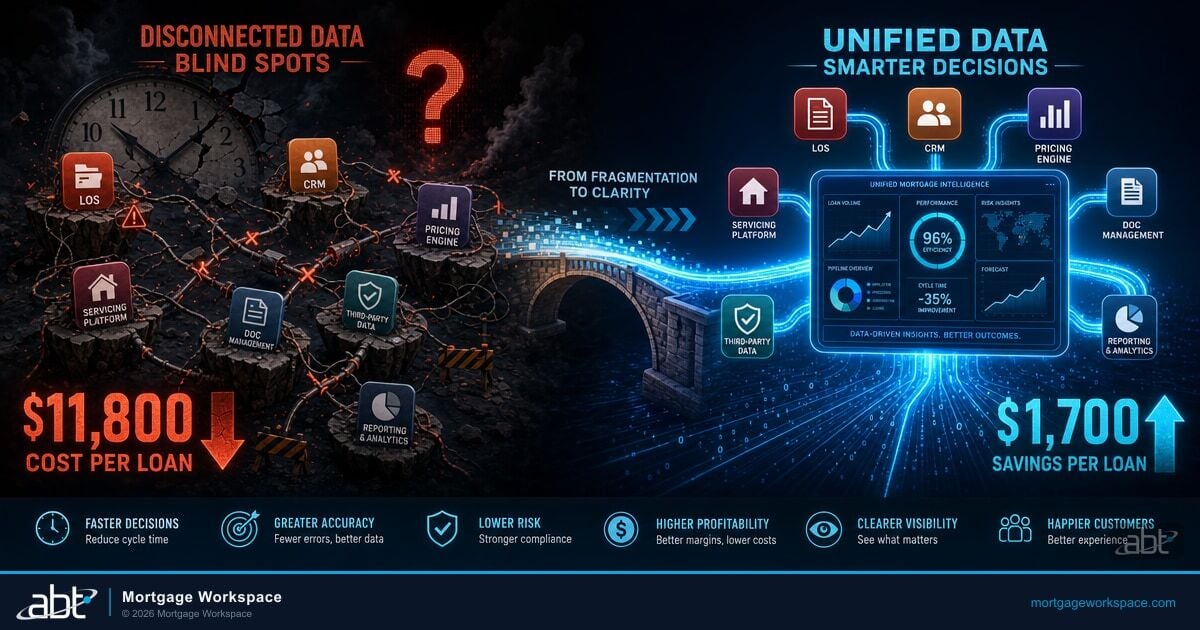

Mortgage lenders generate more data per loan than at any point in the industry's history. Application records, credit pulls, appraisal reports, rate locks, compliance documents, servicing data. But for most organizations, that data sits in disconnected systems where risk hides in the gaps between them.

Business intelligence changes that equation. BI platforms pull data from your LOS, CRM, servicing system, and secondary market feeds into a single analytical layer. Risk patterns that were invisible across silos become obvious in a unified dashboard. The question is no longer whether your organization has the data. The question is whether you can see what it's telling you.

For mortgage companies, credit unions, and banks running lending operations, the stakes keep rising. The Mortgage Bankers Association reported that total mortgage delinquency rates reached 3.97% of all outstanding loans in Q3 2025, with seriously delinquent loans at 1.6%. Lenders without real-time portfolio visibility are the last to notice when those numbers climb.

Why BI Matters More Than Ever for Mortgage Risk

The mortgage industry produces massive volumes of data daily. Loan applications, credit pulls, appraisal reports, rate locks, and compliance documentation all generate data points that need to connect. Without a way to link them, risk teams operate on partial information and gut instinct. We cover Maximizing Profitability Through Mortgage Business Intelligence in a companion piece.

Modern BI platforms like Power BI and mortgage-specific analytics tools solve this by aggregating data across systems. They convert raw numbers into dashboards showing delinquency trends, concentration risk, and portfolio health in near-real-time. Microsoft Power BI integrates natively with the M365 stack that most financial institutions already run, which means BI deployment doesn't require bolting on another vendor relationship.

Why This Matters for Lenders in 2026

CFPB examination priorities for 2026 explicitly call out data governance and risk monitoring practices. Regulators are asking whether institutions have the analytical infrastructure to identify emerging risks before they become losses. BI isn't a back-office project anymore. It's an examination topic.

For lenders working with a managed service provider like ABT, the BI layer connects directly to the security and compliance infrastructure already in place. When your Guardian-hardened Microsoft 365 tenant generates security signals, and your BI platform tracks lending risk signals, you get a picture of operational risk that neither system provides alone.

Catching Fraud Before It Costs You

Mortgage fraud cost the industry an estimated $1.2 billion in 2025 according to CoreLogic. BI tools are one of the strongest defenses against it because they analyze borrower data across multiple dimensions simultaneously.

Here's what BI-powered fraud detection looks like in practice:

- Income verification anomalies: BI flags applications where stated income doesn't match employment data or tax records

- Property value outliers: Automated comparison of appraisal values against comparable sales data and market benchmarks

- Application velocity tracking: Monitoring for borrowers submitting multiple applications across lenders within short timeframes

- Document consistency checks: Cross-referencing data points across forms to catch fabrication or alteration before files reach underwriting

A borrower submits an application listing annual income of $145,000 with employment at a small business. Three weeks later, a different application from the same SSN lists $192,000 with a different employer.

Cross-system velocity tracking flags the duplicate SSN and income discrepancy within minutes. The underwriting team receives an alert before either file reaches conditional approval. Without BI aggregation, each application looks normal in isolation.

The shift from reactive to proactive fraud detection is measurable. Instead of discovering fraud after closing, BI tools flag suspicious patterns during underwriting. That's the difference between a write-off and a prevented loss.

Building Smarter Borrower Risk Profiles

Traditional risk assessment relies heavily on credit scores and debt-to-income ratios. Those metrics matter, but they tell an incomplete story. A borrower with a 720 FICO and a 38% DTI looks identical whether they work in a stable government job or a volatile startup that just laid off 30% of staff.

BI platforms pull in broader data sets to create multidimensional borrower profiles. Payment history trends, employment stability indicators, geographic risk factors, and market conditions all feed into the analysis. The result is a risk profile that reflects the borrower's actual situation rather than a two-number summary.

| Risk Factor | Traditional Assessment | BI-Enhanced Assessment | Impact |

|---|---|---|---|

| Income Stability | Current stated income only | 3-year income trend + employer volatility index | Catches declining income patterns |

| Geographic Risk | Property appraisal | MSA unemployment trends + local market velocity | Flags concentration in declining markets |

| Payment Behavior | Credit score snapshot | Payment velocity trends + seasonal patterns | Identifies deteriorating behavior early |

| Fraud Indicators | Manual document review | Cross-system pattern matching + velocity checks | Detects coordinated fraud rings |

Fannie Mae's 2025 Technology Survey found that 58% of mortgage lenders plan to expand their use of AI and machine learning tools by the end of 2026. Most of those implementations focus on borrower risk modeling. The lenders who adopt these tools early gain a measurable advantage in default prediction accuracy and portfolio quality.

For institutions where ABT manages the M365 environment, Power BI dashboards connect directly to the data sources already governed by Guardian policies. Sensitivity labels, DLP rules, and access controls apply to BI data the same way they apply to email and documents. Risk analytics and data governance aren't separate projects. This connects closely to The Role of Predictive Analytics in Mortgage Risk Assessment.

Pipeline Visibility and Early Warning Systems

One of the most practical BI applications in mortgage risk management is pipeline monitoring. A well-configured dashboard shows your entire loan pipeline with color-coded risk indicators. Problems that used to surface in monthly reports now show up in real time.

Key metrics to track:

- Days in stage: Loans sitting too long in processing or underwriting signal bottlenecks or problems that will affect pull-through rates

- Lock expiration risk: Rate locks approaching expiration represent direct financial exposure, especially in volatile rate environments

- Condition clearing velocity: How fast borrowers return requested documents indicates engagement and likelihood to close

- Pull-through rates by source: Which lead sources produce loans that actually close versus fall out of the pipeline

These aren't vanity metrics. When pull-through rates drop for a specific loan officer or branch, you investigate before the numbers hit your P&L. When lock expirations cluster around a particular product type, you adjust pricing strategy before extension costs accumulate.

Pipeline visibility isn't about having more dashboards. It's about knowing which loan is going to blow up before it does.

How Guardian Ties BI Data to Tenant Security

BI gives you visibility into lending risk. Guardian gives you visibility into technology risk. When both operate on the same Microsoft 365 infrastructure, the overlap creates intelligence that neither system produces alone.

Consider the data flows. Your loan officers access borrower NPI through the LOS, email, Teams, and SharePoint. Guardian's Security Insights monitors those access patterns, sign-in anomalies, MFA compliance, and external sharing. Meanwhile, your BI platform tracks which loans those same officers are processing, their volume trends, and their exception rates.

Security Insights

Sign-in anomalies, MFA gaps, external sharing exposure, risky user behavior patterns across the M365 tenant

Productivity Insights

License utilization, collaboration patterns, application adoption rates, cost optimization signals

Lending Risk Signals

Pipeline velocity, pull-through rates, fraud indicators, concentration risk, delinquency trends from the BI layer

Compliance Posture

DLP policy violations, retention compliance, audit trail completeness, data classification coverage

A loan officer who starts accessing files outside normal hours, from an unfamiliar location, while processing an unusually high volume of loans in a specific geographic area tells a story that neither system sees independently. Guardian catches the security anomaly. BI catches the lending pattern. Together, they surface a risk that manual review would miss entirely.

This is the advantage of working with a managed service provider that handles both the Microsoft 365 governance layer and understands the lending technology stack. ABT's Guardian lifecycle, from hardening through monitoring through insights, creates the security foundation. The BI layer adds operational intelligence on top of it.

Using Market Intelligence to Anticipate Shifts

Risk management isn't only about individual loans. Market-level risk determines portfolio performance. BI tools that incorporate external data feeds give lenders visibility into trends affecting their entire book of business. For ABT's fuller take, see The Benefits of Mortgage Management with MISMO Certified Partners.

The 2026 mortgage market presents a specific challenge. Interest rates have stabilized but affordability constraints persist in many markets. Purchase activity varies significantly by metro area. Lenders using BI to monitor local market conditions can adjust risk appetite by geography, product type, and borrower segment before problems materialize.

For example, if BI data shows rising unemployment in a specific MSA where your portfolio has significant concentration, you tighten underwriting guidelines for new originations in that area before defaults climb. If refinance volume spikes in a region where property values have flattened, you adjust LTV requirements before the next appraisal comes in below expectations.

Key Takeaway

Market-level risk adjustments require connected, current data. Monthly reports and spreadsheets can't keep pace with markets that shift week to week. BI dashboards monitoring real-time feeds from Freddie Mac, local MLS data, and Bureau of Labor Statistics employment numbers give lenders the lead time to adjust before defaults appear in their portfolio.

Getting Started with Mortgage BI

Implementing BI for risk management doesn't require replacing your existing systems. Most modern BI platforms, including Power BI, connect to the tools you already use through APIs and data connectors.

A practical starting point:

- Identify your data sources. Your LOS, CRM, servicing system, and secondary market platform are the core feeds. If you're on Microsoft 365, Power BI can connect to most of these natively.

- Define your key risk metrics. Start with delinquency rates, pull-through rates, fraud flags, and concentration risk. Avoid the temptation to dashboard everything. Five well-chosen metrics beat fifty ignored ones.

- Build dashboards for different audiences. Executives need portfolio-level views. Risk teams need granular, borrower-level drill-downs. Loan officers need their own pipeline health indicators.

- Set automated alerts. Don't wait for someone to check the dashboard. Configure alerts that fire when metrics breach thresholds, the same way Guardian alerts fire when security policies drift.

- Connect BI governance to tenant governance. The same sensitivity labels and DLP policies that protect borrower NPI in email should apply to the BI layer. ABT's Guardian hardening includes configuring these controls across the entire M365 environment, including Power BI workspaces.

ABT serves over 750 financial institutions, including mortgage companies, credit unions, and banks. As the largest Tier-1 Microsoft Cloud Solution Provider dedicated to financial services, ABT configures both the BI platform and the security infrastructure around it. The tools are mature. The data is already flowing through your systems. The question is whether your organization has the governance and analytics in place to see what the data is telling you.

See Where Your Data Governance Stands

ABT's AI Readiness Scan evaluates your Microsoft 365 environment and data governance posture in minutes. Find out whether your BI infrastructure meets the security and compliance standards your examiners expect.

Frequently Asked Questions

Mortgage business intelligence for risk management uses data analytics platforms to aggregate loan data from multiple systems, identify patterns in borrower behavior and portfolio performance, and generate real-time dashboards and alerts. These tools help mortgage companies, credit unions, and banks detect fraud, monitor delinquency trends, and make data-driven decisions to reduce financial exposure across their lending operations.

BI platforms detect mortgage fraud by analyzing borrower data across multiple dimensions simultaneously. They flag income verification anomalies, compare appraisal values against market benchmarks, track application velocity across lenders, and cross-reference document data points. This proactive approach identifies suspicious patterns during underwriting rather than after closing, turning potential write-offs into prevented losses.

Mortgage lenders should track days in stage for processing bottlenecks, rate lock expiration risk for financial exposure, condition clearing velocity for borrower engagement signals, and pull-through rates by source to identify which channels produce loans that close. Automated alerts on threshold breaches provide early warning before pipeline problems affect profitability.

Guardian is ABT's control layer for Microsoft 365 environments. It monitors tenant security, compliance drift, and user behavior. When BI platforms track lending risk signals on the same M365 infrastructure, the two systems create overlapping intelligence. Security anomalies from Guardian combined with lending pattern data from BI surface risks that neither system identifies independently, such as unusual access patterns correlating with high-volume loan processing.

Small mortgage lenders benefit significantly from BI tools because they often lack dedicated risk teams to manually monitor portfolio health. Power BI is included with Microsoft 365 Business Premium licensing, connects to existing loan origination systems through APIs, and requires minimal infrastructure investment. Working with a managed service provider like ABT means the BI environment is configured, secured, and governed from day one.