What You'll Learn

- How Predictive Analytics Works in Mortgage Lending

- Default Prediction and Early Warning Models

- LLM-Powered Risk Models: The 2025-2026 Shift

- AI-Powered Fraud Detection

- Speed and Accuracy Gains for Underwriting

- Regulatory Compliance for AI Risk Models

- Prepayment and Refinance Risk Modeling

- The Data Foundation: Why Predictive Models Stall Without Clean LOS Integration

- Real-Time Market Data Integration

- Building a Predictive Analytics Strategy

- Frequently Asked Questions

An April 2026 arXiv benchmark on the full Home Mortgage Disclosure Act dataset (5.84 million loan records) put gradient-boosted decision trees at 97.9% balanced accuracy for mortgage default classification, with an analog-optical research baseline reaching 94.6%. A February 2025 study had already pushed structured mortgage risk models past 90% accuracy on comprehensive borrower datasets. Machine learning has moved from supplementing underwriting to setting its accuracy ceiling.

Predictive analytics is reshaping how mortgage lenders assess risk. Not by replacing human judgment, but by giving underwriters and risk managers data-driven confidence in every decision. Here's what that looks like in practice.

Since this article was first published in October 2024, the regulatory backdrop for AI-driven mortgage decisions has moved twice. On May 12, 2025, the CFPB withdrew Circular 2023-03 (and Circular 2022-03 alongside it) in a Federal Register notice covering 67 interpretive documents, but the underlying ECOA and Regulation B Section 1002.9(a)(2) requirement to give specific adverse-action reasons remains binding. The OCC's interagency Quality Control Standards for Automated Valuation Models final rule now requires AI-powered property valuations to meet five quality control standards. The Federal Reserve continues to apply SR 11-7 model risk management to all AI and machine learning models used in lending decisions. And starting June 30, 2026, Colorado SB 24-205 layers a state-level AI disclosure regime on top of federal lending law. Every predictive model in your mortgage operation now sits inside this stack.

How Predictive Analytics Works in Mortgage Lending

Predictive analytics uses historical data, statistical algorithms, and machine learning to forecast future outcomes. In mortgage lending, that means analyzing thousands of variables per loan to estimate probability of default, prepayment risk, and fraud likelihood.

Modern models go far beyond FICO scores and LTV ratios. They incorporate employment stability trends, geographic economic indicators, payment behavior patterns, and market condition data. The models learn from millions of historical loans and improve as they process more data. For a deeper look at how Microsoft's AI stack now sits inside this workflow for mortgage lenders, see how Microsoft AI is revolutionizing mortgage underwriting.

Fannie Mae's most recent lender sentiment data showed 55% of mortgage lenders planning to pilot or expand AI and machine learning tools, with the majority targeting underwriting and risk assessment as their first use case. That's not a coincidence. Risk is where predictive analytics delivers the clearest ROI.

Current leading models use XGBoost, LightGBM, Random Forest, and deep learning neural networks. The choice between them depends on your explainability requirements. Gradient boosting models (XGBoost, LightGBM) offer strong accuracy with reasonable interpretability through SHAP values. Deep learning models achieve the highest accuracy but are harder to explain to regulators.

Not sure where your AI risk strategy stands?

Access Business Technologies supports 750+ financial institutions with the Microsoft AI deployment work that sits underneath every mortgage risk model. The AI Readiness Scan benchmarks your tenant in under ten minutes.

Default Prediction and Early Warning Models

The core application of predictive analytics in mortgage risk is default prediction. The MBA's most recent National Delinquency Survey reported the residential mortgage delinquency rate at 3.99% of all outstanding loans, with the FHA delinquency rate at 10.78% and FHA seriously delinquent loans up nearly 50 basis points year over year. For servicers, catching early signs of distress can mean the difference between a workout and a foreclosure.

Predictive models identify borrowers at elevated risk by analyzing:

- Payment behavior trends: Not just whether payments are current, but whether the pattern is deteriorating

- Employment and income stability: Job changes, industry risk factors, and income volatility signals

- Local market conditions: Property values, unemployment rates, and economic indicators in the borrower's MSA

- Credit utilization changes: Rising credit card balances or new account openings that suggest financial stress

Early warning models give servicers time to offer loss mitigation options before loans become seriously delinquent. That's better for borrowers, better for investors, and better for your default rates. For the operational side of integrating AI into existing servicing platforms, see the Microsoft Copilot deployment guide for mortgage operations.

"Lenders who integrate AI-driven predictive analytics into their workflows gain decisive competitive advantages through superior risk assessment, faster approvals, and better portfolio performance."

Finsolutia, Predictive Analytics in Mortgages Report, 2025LLM-Powered Risk Models: The 2025-2026 Shift

Traditional predictive models process structured data: credit scores, income numbers, LTV ratios. Large language models change that equation by analyzing unstructured data that traditional models can't touch.

LLM-powered risk assessment adds new data dimensions to mortgage risk models:

- Document analysis at scale: LLMs read and interpret complex legal documents, title commitments, and appraisal narratives, flagging inconsistencies that structured models miss

- Borrower communication patterns: Analyzing the content and tone of borrower correspondence to detect early distress signals before they appear in payment data

- Market narrative processing: Ingesting regional economic reports, housing market commentary, and employment trend narratives to inform geographic risk adjustments

- Regulatory change tracking: Monitoring GSE bulletins, CFPB guidance, and state regulatory updates to flag compliance implications for existing portfolio positions

The combination of structured prediction models (XGBoost, Random Forest) with LLM-driven unstructured analysis creates risk assessments that capture both the quantitative and qualitative dimensions of mortgage default probability. Lenders implementing these hybrid approaches report more accurate early-warning detection, particularly for borrowers who maintain current payments while showing stress signals in other data. The tradeoff: every additional model in the stack is another artifact your SR 11-7 governance program has to validate, monitor, and document.

The three ABT products that sit underneath every production mortgage risk model are MortgageExchange, Mortgage BI, and Microsoft Purview. MortgageExchange is the custom interface layer that connects the loan origination system (Encompass, Calyx, Mortgage Cadence, MeridianLink) to core banking and to the data lake the risk models actually train on. Clean LOS-to-core data flow is the prerequisite for any XGBoost or LightGBM model that aims for the 97.9% accuracy band, since incomplete or duplicated loan records are the largest single source of model error in real production environments. Mortgage BI is the business intelligence layer where the model outputs land, where pipeline performance is monitored, and where the portfolio-level views examiners ask for during cycle exams are produced. Microsoft Purview Audit Premium retains the underlying decision logs for 12 months by default and 10 years on request, satisfying the regulator-asks-for-the-evidence test under both ECOA Section 1002.9(a)(2) and SR 11-7 model risk governance. Access Business Technologies manages the Microsoft 365 tenant the lender uses for these workloads and operates the connective tissue between them.

Source: ABT MortgageExchange and Mortgage BI product documentation; Microsoft Learn, Microsoft Purview Audit retention configuration reference (2026)

AI-Powered Fraud Detection

Machine learning models excel at fraud detection because they process thousands of data points simultaneously. Human underwriters reviewing an application might catch obvious red flags. Algorithms catch subtle ones.

Current AI fraud detection capabilities include:

- Document anomaly detection: Identifying altered pay stubs, tax returns, and bank statements based on formatting patterns, font inconsistencies, and metadata analysis

- Identity verification: Cross-referencing application data against multiple databases to detect synthetic identities

- Collusion pattern recognition: Identifying networks of related applications that suggest organized fraud rings

- Occupancy fraud signals: Analyzing data patterns that indicate a property will be used as an investment rather than a primary residence

The ROI on AI fraud detection is straightforward. One prevented fraudulent loan can save $100,000 or more. The technology pays for itself after catching a single case. The flip side is the model-risk governance overhead noted in the previous section: a fraud-detection ML model that's lifting your loss-avoidance numbers is also a model your SR 11-7 program now owns. For a balanced view of what mortgage automation gets wrong when governance lags, see the hidden risks in mortgage automation.

Speed and Accuracy Gains for Underwriting

Predictive analytics doesn't just improve accuracy. It makes the entire underwriting process faster. AI-powered risk assessment tools can pre-screen applications in seconds, routing low-risk loans to streamlined processing and flagging complex cases for experienced underwriters.

The speed advantage matters in competitive markets. When borrowers are shopping rates and lenders are competing on turn times, the ability to provide a preliminary risk assessment within minutes rather than days changes outcomes. A Freddie Mac Loan Product Advisor study found AI-assisted underwriting produced a five-day shorter loan production cycle, a 40% reduction in defect rate, and a 14% per-loan origination cost reduction compared to conventional workflows. Lenders implementing AI report operational expense reductions of 30 to 50%, with some achieving loan closures 2.5 times faster than industry averages.

For borrowers, faster assessments mean quicker approvals. They can lock favorable rates and close on properties before competing offers beat them. For lenders, faster processing means higher pull-through rates and lower cost per loan.

The percentage of fully automated loan decisions is expected to climb from today's single digits to 30-40% of volume as models mature and regulatory frameworks catch up. Low-risk conforming loans with clean documentation are the first candidates for full automation. Exception-heavy files will continue to require experienced human underwriters for the foreseeable future.

Regulatory Compliance for AI Risk Models

Deploying predictive analytics in mortgage risk assessment creates regulatory obligations that didn't exist when you were using traditional scorecards. Every model that influences a lending decision falls under regulatory scrutiny. The federal stack changed twice in 2025; the state stack is changing again in 2026.

CFPB Adverse Action Requirements

On May 12, 2025, the CFPB withdrew Circular 2023-03 along with Circular 2022-03 as part of a 67-document withdrawal published in the Federal Register (notice 2025-08286). The Bureau explicitly stated those documents "should not be enforced or otherwise relied upon by the Bureau while this review is ongoing." That does not, however, take the underlying law off the table. ECOA and Regulation B Section 1002.9(a)(2) still require specific and accurate reasons for every adverse credit action. If your model declines a borrower, you still need to explain exactly why in terms the borrower can understand. Broad categories like "credit risk score" remain insufficient under the statute. Lenders should plan for compliance against the black-letter law rather than the withdrawn interpretive guidance.

SR 11-7 Model Risk Management

The Federal Reserve's SR 11-7 guidance, jointly issued with the OCC, continues to apply to all AI and machine learning models used in lending decisions. The guidance requires model governance, independent validation, and effective challenge. For community banks and mortgage companies, the OCC's Spring 2025 Semiannual Risk Perspective reiterated that institutions can tailor their model risk management practices to their size, but the core requirements remain. Every predictive model needs documentation, periodic validation, and a clear escalation path when model performance degrades. For lenders subject to GSE oversight, see the Freddie Mac AI mandate compliance checklist.

Fair Lending and Explainability

A January 2025 CFPB supervisory highlights report flagged disproportionately high adverse outcomes from AI models using more than a thousand variables. Models that overfit on large variable sets can create fair lending risk even when protected classes are excluded from inputs. The remedy: use explainable model architectures (SHAP, LIME) that can demonstrate which variables drive each decision, and regularly test for disparate impact across protected classes. For a worked example on managing AI vendor risk inside that fair lending posture, see FHFA drops Anthropic: what AI vendor risk means for mortgage lenders.

Colorado SB 24-205 and State AI Overlays

Colorado's AI Act (SB 24-205) takes effect June 30, 2026 after a delay from its original February 2026 date. The law applies to "high-risk" AI systems making consequential decisions, which includes credit and lending. Mortgage lenders with Colorado borrowers will need to provide disclosures about AI use in decisioning, conduct impact assessments, and meet specific notice requirements. Other states are following Colorado's pattern, and federal preemption is not currently on the table. Lenders should treat state AI laws as an additional compliance layer on top of ECOA, SR 11-7, and CFPB enforcement, not an alternative to them.

Prepayment and Refinance Risk Modeling

For lenders and servicers who hold or service mortgage-backed securities, prepayment risk directly affects portfolio performance. Predictive models forecast which borrowers are likely to refinance based on rate differentials, remaining term, and borrower characteristics.

This modeling helps with:

- Hedging decisions: More accurate prepayment forecasts improve hedge performance

- Portfolio valuation: Better prepayment models lead to more accurate mark-to-market pricing

- Retention strategies: Identifying borrowers at high refinance risk lets servicers proactively offer competitive retention options

The MBA Weekly Applications Survey for the week ending May 1, 2026 showed refinance applications down 5% week over week but up 29% year over year, with the 30-year fixed rate at 6.45% and refinance share holding at 42% of total applications. Forecasts cluster in the 6.0 to 6.4% band through 2026, which suggests steady incremental refi activity rather than a 2020-style wave. Lenders with strong prepayment models will navigate that environment more profitably than those relying on broad assumptions.

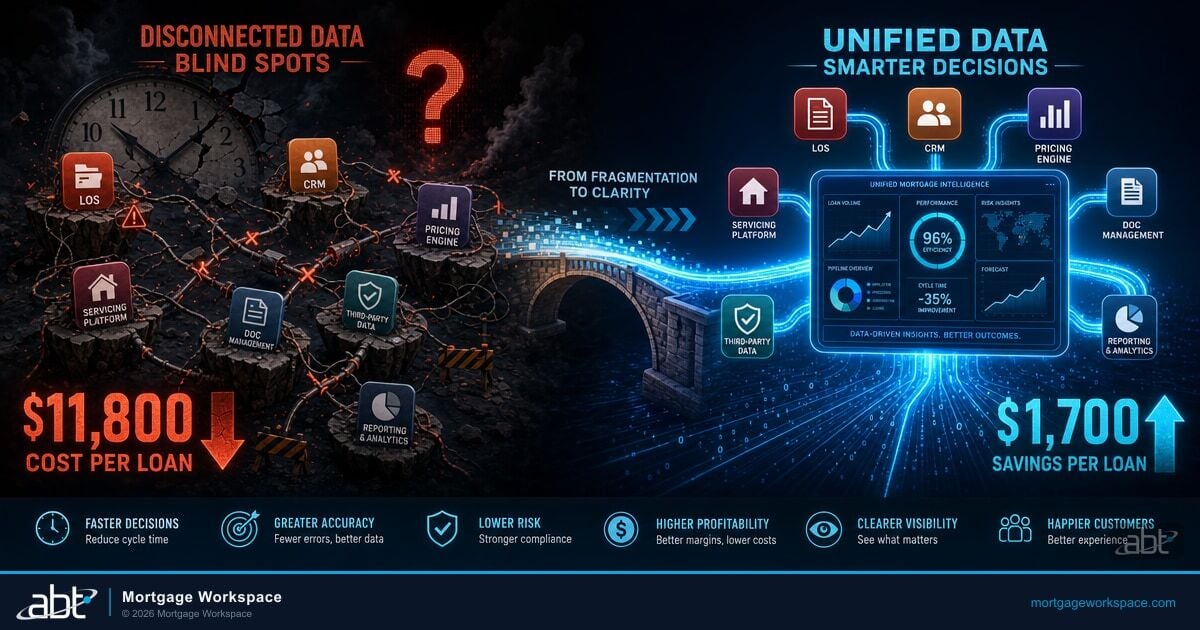

The Data Foundation: Why Predictive Models Stall Without Clean LOS Integration

Most lenders who launch a predictive analytics initiative discover, somewhere between months two and four, that the bottleneck is not the model. It is the data. A risk model that aims for the 97.9% accuracy band on HMDA-style benchmarks needs continuous, clean, fully reconciled records flowing from the loan origination system into the analytics environment. Encompass, Calyx, Mortgage Cadence, and MeridianLink each emit data in different shapes. Servicing systems hold the post-close payment history in yet another shape. Core banking owns the deposit-side income signals. When those streams arrive duplicated, mismatched on borrower identifier, or missing entire loan stages, the model performs worse on real borrowers than it did on the training sample. The work to reconcile those streams is rarely glamorous, but it is the work that decides whether the model is a portfolio asset or a model-risk liability.

MortgageExchange is the layer that does that reconciliation work for ABT's mortgage clients. It moves loan data between LOS, servicing, and core, applies the matching logic that keeps a single borrower and a single loan correctly identified across every system that touches it, and lands the result in a shape Mortgage BI can read. Mortgage BI then produces the dashboards and portfolio-level views that risk managers, compliance leads, and chief credit officers actually use to act on what the predictive models surface. Microsoft Purview Audit Premium runs on top of all of it as the time-stamped evidence trail that ECOA Section 1002.9(a)(2) adverse-action explanations and SR 11-7 model validation cycles both require. When examiners ask why a model declined a loan or how the model has performed over the last 12 months, the answer is one query away rather than three weeks of spreadsheet work. The data foundation is the unglamorous part of the predictive analytics story, but it is the part that makes the model count.

Real-Time Market Data Integration

Static risk models that recalculate quarterly are becoming obsolete. The shift toward real-time data integration means predictive models now ingest live market feeds and adjust risk scores continuously.

Real-time data sources changing mortgage risk assessment include:

- Live property value feeds: Automated valuation models pull comparable sales data daily rather than relying on appraisals that are 30-60 days old at closing

- Employment verification APIs: Direct connections to payroll providers verify employment status in real-time rather than relying on static VOE letters

- Economic indicator streams: Regional unemployment data, consumer spending patterns, and housing starts feed directly into risk models

- Rate environment monitoring: Prepayment models adjust in real-time as rate markets move, improving hedge accuracy

The OCC's interagency Quality Control Standards for Automated Valuation Models final rule requires that AI-driven property valuations meet five specific standards: confidence score reporting, nondiscrimination testing, model validation, data integrity checks, and compliance with FIRREA. Lenders using real-time AVM feeds need to ensure their data pipelines meet these standards before the next examination cycle.

Building a Predictive Analytics Strategy

Implementing predictive analytics for risk assessment requires three things: clean data, the right models, and people who know how to act on the results.

- Start with data quality. Predictive models are only as good as the data they consume. Invest in data standardization and cleansing before building models. For ABT clients, MortgageExchange does this work between LOS, servicing, and core banking systems

- Choose models that fit your use case. Default prediction, fraud detection, and prepayment modeling each require different approaches. XGBoost and LightGBM offer the best balance of accuracy and explainability for most mortgage applications

- Build explainable models. Regulators require that lending decisions be explainable. Black-box models that cannot articulate why they flagged a loan create compliance risk. Use SHAP or LIME for model interpretability

- Surface the outputs through a BI layer your risk team will actually use. Mortgage BI dashboards turn model probabilities into pipeline views, portfolio segments, and exception queues that risk officers and chief credit officers can act on

- Train your team. The best model in the world is worthless if your underwriters don't trust or understand its output

- Validate continuously. SR 11-7 requires periodic model validation. Set up automated model performance monitoring that flags accuracy degradation before it becomes a compliance issue

- Retain decision logs in a tamper-evident audit trail. Microsoft Purview Audit Premium retains the per-decision evidence trail for 12 months by default and up to 10 years on request, which satisfies both ECOA adverse-action documentation and SR 11-7 validation requirements

- Test for fair lending impact. Run disparate impact analysis across protected classes before deployment and on a regular schedule after. Document everything for regulatory examination

Access Business Technologies serves 750+ financial institutions with the MortgageExchange, Mortgage BI, and Microsoft Purview stack that makes the technical side of this list operational. The mortgage technology partners who can connect predictive analytics tools with your existing LOS and servicing platforms, retain the decision evidence for regulatory examination, and surface the model outputs through dashboards your team will actually use are the ones who turn a predictive analytics pilot into a production risk capability.

Get the AI risk foundation right before you scale models

ABT's 4-Phase AI Journey gives mortgage lenders a tenant-level readiness benchmark, an SR 11-7 governance starter pack, MortgageExchange data integration between LOS and core, Mortgage BI dashboards for risk and compliance teams, and a Microsoft Purview Audit configuration tuned to capture the evidence regulators ask for. We do this for 750+ financial institutions on the Microsoft cloud.

Frequently Asked Questions

Predictive analytics improves mortgage risk assessment by analyzing thousands of variables per loan application using machine learning algorithms. These models incorporate payment behavior trends, employment stability data, local market conditions, and credit utilization patterns to produce default probability scores that are significantly more accurate than traditional underwriting methods relying on a few standard metrics.

Common machine learning models for mortgage default prediction include XGBoost, LightGBM, Random Forest, deep learning neural networks, and logistic regression ensembles. An April 2026 arXiv benchmark on the full HMDA dataset (5.84 million records) reported XGBoost reaching 97.9% balanced accuracy, with an analog-optical research baseline at 94.6%. Model selection depends on explainability requirements, since ECOA and Regulation B require lenders to provide specific reasons for adverse lending decisions.

AI detects mortgage fraud during underwriting by analyzing document metadata for alterations, cross-referencing application data against identity databases, recognizing collusion patterns across related applications, and identifying occupancy fraud signals. Roughly 85% of mortgage lenders now use AI for fraud detection, with industry-wide accuracy improvements estimated at 50% over rule-based methods. Machine learning processes thousands of data points simultaneously, catching subtle inconsistencies that human reviewers typically miss.

Mortgage lenders need loan origination data, borrower credit and employment history, payment behavior records, property valuation data, local economic indicators, and secondary market performance data. Data quality and standardization are prerequisites for accurate models. Most lenders start by connecting their loan origination system data through APIs before adding external data feeds for market conditions and economic indicators. The MortgageExchange interface ABT operates handles the LOS-to-core data reconciliation that predictive risk models depend on.

AI risk models in mortgage lending must comply with the Federal Reserve's SR 11-7 model risk management guidance, which requires model governance, independent validation, and effective challenge. ECOA and Regulation B require specific and accurate adverse action reasons (the CFPB withdrew the related Circular 2023-03 in May 2025, but the underlying statute remains in force). The OCC mandates quality control standards for automated valuation models. Colorado SB 24-205 layers state-level AI disclosure requirements on top of federal rules effective June 30, 2026. Lenders must also conduct regular fair lending testing to ensure AI models do not produce disparate impact across protected classes. Microsoft Purview Audit Premium retains the per-decision evidence trail for 12 months by default and up to 10 years on request.

Traditional predictive models process structured data like credit scores and LTV ratios. Large language models analyze unstructured data that traditional models cannot process, including legal documents, appraisal narratives, borrower correspondence, and regional economic reports. The combination of structured prediction models with LLM-driven unstructured analysis creates risk assessments that capture both quantitative metrics and qualitative signals, improving early-warning detection for borrower distress. Every LLM layer added is another artifact your SR 11-7 governance program needs to validate and monitor.

Yes. On May 12, 2025, the CFPB published Federal Register notice 2025-08286 withdrawing 67 interpretive rules, policy statements, and advisory opinions, including Circular 2023-03 and the earlier Circular 2022-03 on adverse action notification requirements for complex algorithms. The withdrawal removed the Bureau's specific interpretive guidance but did not change the underlying law. ECOA and Regulation B Section 1002.9(a)(2) still require specific and accurate reasons for adverse credit actions, including those generated by AI or machine learning models. Mortgage lenders should align compliance work to the statute and regulation directly rather than the withdrawn guidance documents.