In This Article

MISMO published Reference Model Version 3.6.2 on October 30, 2025. Wolters Kluwer earned MISMO certification for its eOriginal eVault and ClosingCenter platforms on November 12, 2025. The MISMO Mortgage Compliance Dataset (MCD) reached Version 2.0 in late 2025 and is now live and ready for use across state regulatory examinations. Those milestones matter in 2026 because the compliance calendar is tightening: UAD 3.6 becomes mandatory for new UCDP appraisals on November 2, 2026, ULDD Phase 5 fatal-edit enforcement is already live at Fannie Mae and Freddie Mac, and state regulators are aligning examination templates to the MCD baseline.

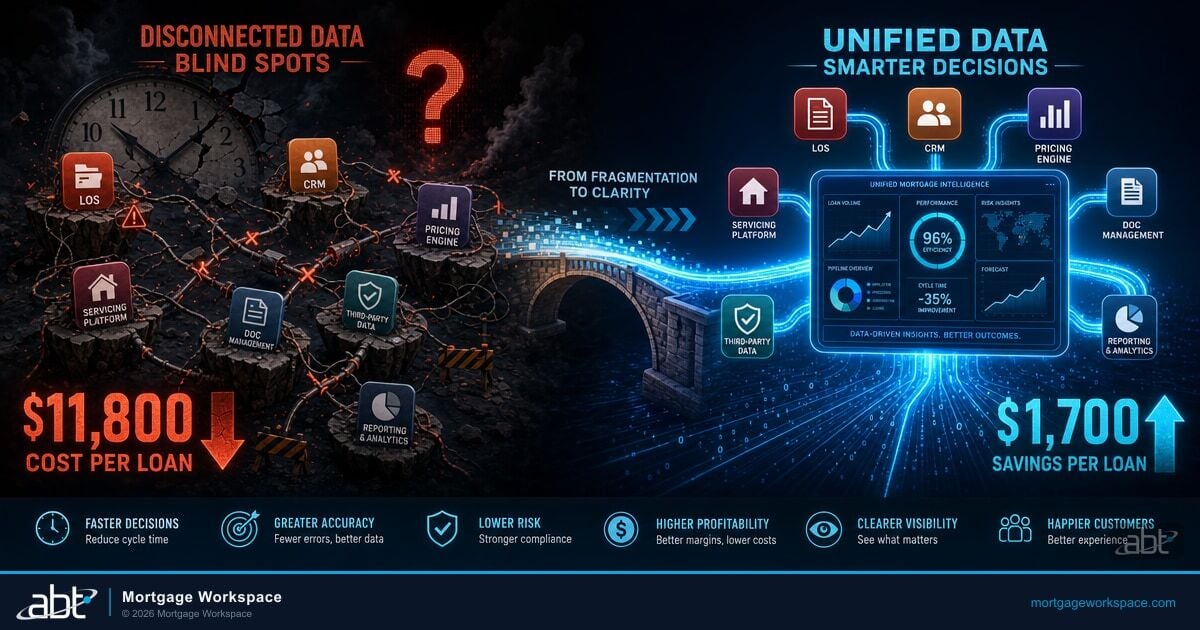

The Mortgage Bankers Association reported the average cost to originate a loan hit $11,109 in Q3 2025, more than $3,300 above the long-run historical average of $7,799. A meaningful share of that excess sits inside avoidable integration work: data reformatting between systems, exception handling on rejected GSE deliveries, and manual reconciliation of fields that should have flowed cleanly from origination to closing.

MISMO, the Mortgage Industry Standards Maintenance Organization, sets the standards for how mortgage data moves between systems. When your technology partners follow those standards, data flows from application through closing to the secondary market without translation layers. When they do not, your team spends hours reconciling mismatched fields and reformatting files. This article explains what MISMO certification means in 2026, what the current deadline calendar requires, and how it connects to your broader technology strategy.

What MISMO Certification Actually Means

MISMO is a subsidiary of the Mortgage Bankers Association. It develops and maintains the data standards that govern how information moves between mortgage technology systems. Fannie Mae, Freddie Mac, Ginnie Mae, the FHA, and the CFPB all reference MISMO standards in their guidance and operational specifications.

MISMO certification comes in two practical forms that buyers see most often:

- Certified MISMO Standards Professional (CMSP). Individual certification for professionals who demonstrate advanced knowledge of MISMO standards and implementation practices.

- System and product certifications. Firm-level evaluations that test specific platforms against MISMO compliance criteria, including the Remote Online Notarization, eClosing System, and eVault System certifications listed on mismo.org. Wolters Kluwer earned eVault and ClosingCenter certifications for its eOriginal platforms on November 12, 2025, after independent third-party evaluation.

When a technology partner holds MISMO certification, it has been vetted for the ability to implement data standards correctly. That matters because a poorly implemented standard is worse than no standard at all. It creates a false sense of compatibility, and the resulting integration failures are expensive to detect because they look like data quality problems instead of architectural problems.

Why the MISMO Version Matters Right Now

MISMO published Reference Model Version 3.6.2 on October 30, 2025, a backward-compatible additive release. Version 3.6.1 (May 2025) added reverse mortgage data; Version 3.6.2 added new data points, containers, and enumerations and includes a MISMO Unique ID matrix to simplify implementation. Lenders implementing 3.6.2 do not need to rebuild systems already aligned to 3.6.x. The bigger pressure is the surrounding standards stack: Uniform Appraisal Dataset 3.6 entered Broad Production on January 26, 2026 and becomes mandatory for new UCDP appraisals on November 2, 2026. Lenders aligned to MISMO 3.6.x are already positioned for UAD 3.6; lenders running older versions face a forced migration on a deadline.

Why System Connectivity Depends on Standards

A mortgage operation runs on multiple systems. Your LOS handles origination. Your core banking platform manages servicing for credit unions and banks running depositary servicing. Your pricing engine pulls investor rates. Your compliance tools check regulatory requirements. Your document management system stores and retrieves files. Your secondary marketing tools deliver loans to the GSEs.

Every handoff between these systems is a potential failure point. When systems use the same data format, handoffs work. When they do not, someone on your team manually translates data from one format to another, which is where most cost-per-loan creep comes from in operations that grew through acquisitions or that bolted on best-of-breed point solutions over time.

What MISMO standards actually cover:

- ULDD (Uniform Loan Delivery Dataset) Phase 5. The data format required for delivering loans to Fannie Mae and Freddie Mac. Phase 5 became mandatory on July 28, 2025, with fatal-edit enforcement on the XML submission. Phase 5 added the Universal Loan Identifier, Enterprise Credit Score data, and Credit Reports Initiative fields, and aligned property data with UAD 3.6.

- UCD (Uniform Closing Dataset) v2.0. Standardizes Closing Disclosure data for GSE delivery. The transition to v2.0 began September 29, 2025 with production environments now accepting compliant XML. Mandate dates are expected in Q3 2026 or later.

- SMART Doc. Specifications for secure, tamper-evident electronic documents, including eNotes that satisfy ESIGN Act and UETA requirements.

- RON (Remote Online Notarization). Standards for remote notarization that support fully digital eClose workflows. As of 2026, more than 47 U.S. states have permanent RON laws on the books, though the federal SECURE Notarization Act still has not passed.

- MISMO Reference Model 3.6.2. The current backward-compatible release covering loan application data, property information, borrower details, and transaction records. Version 3.6.x is the working baseline most LOS, closing, and servicing platforms target.

- Mortgage Compliance Dataset (MCD) v2.0. A joint MISMO and Conference of State Bank Supervisors initiative that reached Version 2.0 public comment in November 2025. The dataset standardizes compliance examination data so state regulators across jurisdictions can run risk-based, technology-driven exams against the same baseline.

When your LOS, closing platform, secondary marketing tools, and servicing system all speak MISMO 3.6.x, data moves between them without manual intervention.

Real-Time Data Exchange and Its Business Impact

Overnight batch processing was the standard for years. Your LOS would send a file to the core system at midnight. If something failed, you would not know until the next morning.

MISMO-compliant integrations support real-time data exchange. Loan status updates, condition clearances, and closing data move between systems immediately instead of waiting for an end-of-day window.

Business impact of real-time exchange:

- Faster lock-to-close timelines. When underwriting conditions clear in the LOS, the closing team sees the update instantly instead of waiting for a batch sync.

- Fewer errors from stale data. Real-time sync eliminates the window where two systems show different information for the same loan.

- Better borrower communication. Loan officers can give borrowers accurate status updates because the data they see is current.

- Reduced exception handling. Most data mismatches between systems trigger manual reviews. Real-time sync prevents most of those mismatches from occurring in the first place.

- Faster GSE delivery. ULDD Phase 5 fatal edits caught at origination instead of at delivery save round-trip rework that delays settlement.

Real-time data exchange is not a nice-to-have once cost-per-loan sits north of $11,000. The savings show up in three places: fewer rejected GSE deliveries, fewer hours spent reconciling field-level mismatches between the LOS and the core, and lower borrower abandonment when loan officers can answer status questions immediately.

Credit unions, banks, and mortgage companies that operate on MISMO-compliant integrations report measurable improvements in processing time and error rates compared to peers running custom field mapping or middleware translation layers. The exact savings depend on loan volume and existing integration quality, but the direction is consistent.

Wondering whether your existing integrations actually carry MISMO data end-to-end, or whether they translate it through middleware that introduces errors? Talk to an ABT mortgage IT specialist about an integration audit that maps your real data flow against MISMO 3.6.x and ULDD Phase 5.

MISMO Standards and Regulatory Compliance

Regulators reference MISMO standards in their guidance and in many of the data formats they require. Fannie Mae and Freddie Mac require ULDD Phase 5 and UCD v2.0 compliance for loan delivery. State regulators are aligning examination procedures with the MISMO Mortgage Compliance Dataset through the joint CSBS initiative. The CFPB references MISMO data definitions in its industry guidance, although CFPB HMDA filing itself uses CFPB's own pipe-delimited LAR format rather than MISMO XML directly.

For mortgage lenders, MISMO alignment simplifies compliance in three ways:

| Compliance area | What MISMO alignment delivers | Anchor reference |

|---|---|---|

| Consistent data definitions | Every system uses the same field names and data formats, so regulatory reports pull clean data without manual mapping. CFPB HMDA filing still uses pipe-delimited LAR, but lenders can collect HMDA fields in MISMO 3.6.x and translate at submission. | CFPB HMDA Filing Instructions Guide 2026 |

| Audit-ready records | MISMO-formatted data creates a standardized audit trail that examiners can follow across systems. The MCD v2.0 from MISMO and CSBS extends this to state-level mortgage compliance exams. | MISMO Mortgage Compliance Dataset (MCD) v2.0, November 2025 |

| Reduced rework during GSE delivery | Loans formatted to ULDD Phase 5 and UCD v2.0 standards at origination do not need reformatting before delivery. Phase 5 fatal edits at the EarlyCheck stage prevent late-stage rejections. | Fannie Mae ULDD Phase 5.1.0 Specification, mandatory July 28, 2025 |

| Examination consistency across states | The CSBS/MISMO MCD lets state regulators run risk-based, technology-driven examinations against a consistent baseline rather than each state defining its own data format. | MISMO Mortgage Compliance Dataset, live as of late 2025 |

The MCD initiative passed an important threshold when Version 2.0 reached public comment in November 2025 and the dataset became live and ready for use. Multiple state-level supervisors have signaled they will adopt the MCD baseline as it stabilizes, which means lenders aligned to MISMO standards now will already be aligned to the dataset state examiners ask for next.

RON adoption status, May 2026

More than 47 U.S. states have permanent Remote Online Notarization laws on the books as of 2026. The federal SECURE Notarization Act, which would create a national RON standard, has not passed. Banks, credit unions, and mortgage companies operating in multiple states should treat RON as a state-by-state checklist rather than relying on federal preemption.

Choosing MISMO-Aligned Technology Partners

Not every technology vendor claiming MISMO compliance has actually tested their implementation against the current reference model. Ask vendors specific questions before signing or renewing:

- Which MISMO Reference Model version do you support? Version 3.6.2 published October 2025 is current.

- Have your integrations been tested against the MISMO reference implementation, and do you maintain a Logical Data Dictionary alignment report?

- Do your data exports comply with ULDD Phase 5 and UCD v2.0 fatal-edit requirements?

- How do you handle MISMO version updates between minor releases like 3.6.1 to 3.6.2?

- Have you mapped your closing data path to UAD 3.6, given the November 2, 2026 mandatory transition?

Your managed IT partner plays a role here too. The infrastructure that hosts your LOS, manages your Microsoft 365 environment, and maintains your integrations has to be operated by a team that understands mortgage data standards. Your integration architecture should be assessed by people who can read MISMO XML and who understand what an ULDD edit failure looks like in production.

Access Business Technologies has managed Microsoft 365 tenants and Azure environments for credit unions, banks, and mortgage companies for more than two decades and serves more than 750 financial institutions today. ABT manages the Microsoft 365 tenants that wrap MISMO-compliant LOS, closing, and servicing platforms with Microsoft Entra ID conditional access for identity, Microsoft Defender for Office 365 for email security on lender-borrower communications, Microsoft Purview for retention and audit on closing documents, and Microsoft Intune for device management on the loan officer fleet. The Microsoft 365 layer is what keeps the data inside MISMO-compliant systems governed, encrypted, and examiner-ready.

If your existing partners are still talking about MISMO 3.4 or unable to answer ULDD Phase 5 questions concretely, that is a sign that the integration risk is not fully covered. Refer to building a compliant IT framework for the broader context of how MISMO alignment fits a full compliance posture.

How Microsoft 365 Supports MISMO-Compliant Operations

MISMO standards govern the data inside the LOS, the closing platform, and the connections between them. Microsoft 365 governs the people, identities, devices, and documents that surround that data. When ABT manages both layers together, loan officers access LOS data from any enrolled device, condition clearances reach the closing team without a batch-sync delay, and the audit trail builds automatically in the background. The security controls and examination-ready records are a byproduct of the same configuration that makes the team faster.

Specific Microsoft 365 components that support MISMO-compliant workflows:

- Microsoft Entra ID Conditional Access enforces multi-factor authentication on every loan officer, processor, and underwriter who touches MISMO-formatted data inside the LOS or the closing platform. Conditional Access policies block sign-ins from risky locations and unmanaged devices, which closes a common audit finding for mortgage operations.

- Microsoft Purview Audit and Information Protection retain audit-quality logs on every action against borrower data and apply sensitivity labels to closing documents so they cannot be sent outside the organization without explicit override. Purview retention policies satisfy SEC Rule 17a-4, FINRA 4511, and the documentation requirements that attach to MISMO-formatted closing records.

- Microsoft Defender for Office 365 protects the email channel that lenders, title agents, warehouse lenders, and GSE delivery partners use to confirm closing data and reconcile exception handling. Anti-phishing and Safe Links protect against business email compromise on the funding-day email thread.

- Microsoft Intune manages the laptops and mobile devices that loan officers use in the field, ensuring that even unmanaged endpoints meeting Conditional Access requirements have current encryption, screen-lock policies, and remote wipe configured.

- Microsoft 365 Copilot for Lending adds AI assistance that operates within the same Microsoft 365 governance boundary, so summarized loan files, document review tasks, and disclosure generation respect the same retention, sensitivity, and audit controls that govern the underlying data.

Microsoft 365 does not replace MISMO standards. But MISMO-formatted data without the surrounding Microsoft 365 controls is clean at the field level and exposed at the access and retention level. Mortgage companies, banks, and credit unions running both layers correctly produce evidence packages that hold up to OCC, NCUA, FDIC, and state mortgage regulator examinations without scrambling on examination week.

Decision Lens

If a vendor cannot answer "which MISMO version do you support" with a specific 3.6.x answer, the integration risk is higher than it looks. If a vendor supports MISMO but your Microsoft 365 environment is not configured for the surrounding controls, the audit risk is higher than it looks. Both layers need to be current. Automated compliance using Power Automate can stitch the two layers together for evidence collection.

Map your real MISMO and Microsoft 365 footprint before the next examination

Most mortgage operations think they are MISMO-aligned because their LOS vendor said so on the contract. The audit reality lives in the integrations that connect the LOS to the closing platform, the secondary market, the core, and the document-of-record. ABT manages the full stack for more than 750 financial institutions and can show you exactly where your MISMO data flows cleanly and where it gets translated.

Frequently Asked Questions

MISMO certification validates that a professional or system has demonstrated advanced knowledge and implementation experience with Mortgage Industry Standards Maintenance Organization data standards. It matters because MISMO standards govern how loan data moves between origination systems, closing platforms, compliance tools, and the secondary market. Partners with certification have been vetted for correct implementation, reducing the risk of integration failures that cause data errors and processing delays.

The Uniform Loan Delivery Dataset Phase 5 became mandatory on July 28, 2025 and standardizes loan-level data submitted with each mortgage delivery to Fannie Mae and Freddie Mac, including the new Universal Loan Identifier and Enterprise Credit Score data. The Uniform Closing Dataset v2.0 transition began September 29, 2025 and standardizes Closing Disclosure data for GSE delivery. Loans that do not conform to these formats are rejected by the GSEs, requiring manual correction and resubmission that delays settlement and increases cost per loan.

MISMO Reference Model 3.6.2, published October 30, 2025, is a backward-compatible additive release that builds on 3.6 and 3.6.1 with new data points, containers, enumerations, and a Unique ID Matrix. Systems that implement Version 3.6.x can exchange data without custom field mapping or manual translation. This reduces integration development time, eliminates data format mismatches between systems, and supports real-time data exchange instead of overnight batch processing. Lenders implementing 3.6.2 do not need to rebuild systems already aligned to earlier 3.6 releases.

The MISMO Mortgage Compliance Dataset (MCD) is a joint MISMO and Conference of State Bank Supervisors initiative that standardizes the data state regulators use for residential mortgage origination compliance examinations. MCD Version 2.0 reached public comment in November 2025 and is now live and ready for use. The dataset enables risk-based, technology-driven examinations, pre-exam compliance testing for mortgage originators, and a consistent baseline across jurisdictions, which is meaningful for credit unions, banks, and mortgage companies licensed in multiple states.

A managed IT provider maintains the infrastructure that MISMO-compliant systems depend on, including LOS hosting, integration monitoring, security configuration, and compliance controls. When MISMO version updates require system changes, the IT provider coordinates testing and deployment across all connected platforms. The provider also ensures that data flowing between MISMO-compliant systems remains encrypted, access-controlled, and audit-logged per regulatory requirements, typically using Microsoft Entra ID for identity, Microsoft Purview for retention, and Microsoft Defender for Office 365 for email security on lender-borrower communications.

MISMO's SMART Doc standard provides specifications for tamper-evident electronic documents including eNotes that satisfy ESIGN Act and UETA requirements. The Remote Online Notarization standards define how notarization sessions are conducted, recorded, and stored electronically. As of 2026, more than 47 U.S. states have permanent RON laws, although the federal SECURE Notarization Act has not passed. Together, the SMART Doc and RON standards enable fully digital closings where borrowers sign documents remotely and the resulting electronic records are accepted by the GSEs, title insurers, and warehouse lenders.