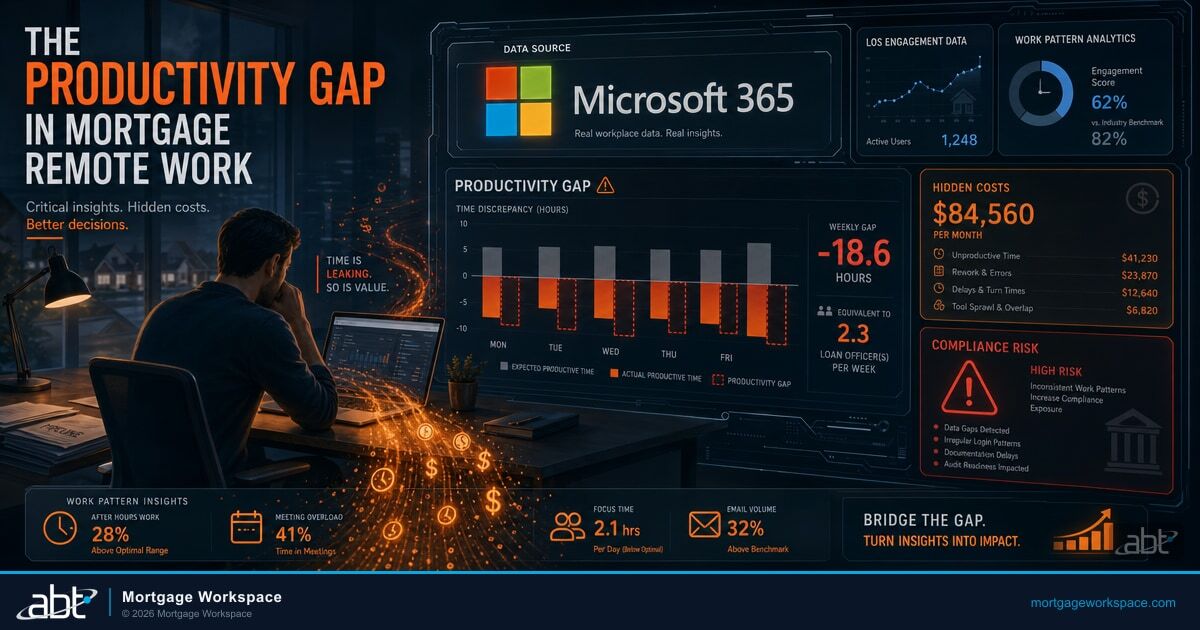

In This Article

The loan origination system (LOS) market is projected to reach $9.1 billion by 2030, growing at 10.5% annually. The driving force behind that growth is not new features. It is the shift from desktop-installed software to cloud-based platforms that let loan officers, processors, underwriters, and closers work from the same data in real time.

Traditional mortgage workflows were built around handoffs. A loan officer collects the application, hands it to a processor, who hands it to underwriting, who sends conditions back down the chain. At every handoff, information gets lost, delayed, or misinterpreted.

Cloud-based loan origination eliminates the handoff model. Everyone works from the same loan file, sees the same updates, and communicates within the same system. This guide covers how that works in practice and what mortgage teams gain from making the switch.

In This Article

Why Traditional LOS Workflows Create Collaboration Problems

Desktop-based loan origination systems were designed when everyone worked in the same building. They solved the problem of the 1990s: getting loan data into a computer instead of a filing cabinet. They did not solve the problem of the 2020s: getting five people in three locations to work on the same loan simultaneously. Our guide to Transforming Your Secure Score Into a Cybersecurity Roadmap goes deeper on this.

Siloed Departments

In a traditional setup, each department sees its own slice of the loan. The processor has their checklist. The underwriter has their conditions. The closer has their documents. Nobody has a complete, real-time picture of where the loan stands unless they pick up the phone or send an email.

A STRATMOR Group study found that mortgage lenders are increasingly investing in automation and AI as foundational technologies precisely because these silos create measurable inefficiency. The data exists. It is just trapped in separate systems.

Slow Communication Loops

Email is the default communication tool for most mortgage teams. It was not designed for real-time collaboration on a shared document. A processor emails an underwriter about a missing bank statement. The underwriter responds four hours later. The processor was working on a different file by then. The follow-up takes another day.

These delays compound. Five loans, each with two unnecessary email delays per week, adds up to 10 lost days of processing time per month across a small team.

Limited Remote Access

Desktop LOS installations require VPN connections or specific hardware. When a loan officer is at a borrower's kitchen table, they cannot pull up the latest conditions list without calling the office. When a processor works from home, they deal with VPN lag that turns every click into a 3-second wait.

Compliance Tracking Gaps

When different teams track compliance in different systems, inconsistencies develop. The processor marks a disclosure as sent. The compliance system does not reflect it. During an audit, those gaps create findings that take hours to reconcile.

What Cloud-Based Loan Origination Actually Changes

Single Source of Truth

A cloud-based LOS stores the loan file in one place. Every team member accesses the same record. When a processor uploads a pay stub, the underwriter sees it immediately. When an underwriter clears a condition, the closer sees it in their queue within seconds.

There is no version confusion. No "I was looking at an old copy." No reconciliation between what the processor thinks happened and what the underwriter's system shows.

Real-Time Updates Across Locations

Cloud platforms reflect changes instantly. A loan officer updates a borrower's income figure at 2:14 PM. The underwriter reviewing that same file at 2:15 PM sees the current number, not yesterday's version.

This matters for compliance too. Disclosure timing, rate lock expirations, and regulatory deadlines all depend on accurate timestamps. A cloud LOS applies those timestamps automatically and consistently.

Access from Any Device

Modern cloud LOS platforms are 100% browser-based. No VPN. No specific hardware. A loan officer can check a loan status from a tablet at a real estate closing. A processor can clear conditions from a laptop at home. An underwriter can review a file from any location with an internet connection. For ABT's fuller take, see Modern Loan Origination Systems Redefining Mortgage Efficiency.

Automated Workflow Routing

Cloud platforms automate the handoffs that create delays in traditional workflows. When a processor marks a file complete, it routes to the underwriting queue automatically. When an underwriter issues conditions, the processor gets notified and the conditions appear in their task list. No email required.

Benefits of Cloud LOS by Role

Loan Officers

Loan officers spend less time chasing status updates and more time with borrowers. Automated document collection reduces the back-and-forth on missing items. Real-time pipeline visibility lets them give borrowers accurate timelines instead of guessing.

The business impact is direct. Faster processing means more closings per month. Better communication means higher referral rates from realtors and past clients.

Processors

Processors gain the most from cloud LOS adoption. Automated task routing replaces the manual checklist. Integrated document management eliminates the file-hunting that consumes hours each week. Real-time condition tracking shows exactly what is outstanding without asking anyone.

Underwriters

Underwriters access complete loan files with full documentation from the moment a file hits their queue. No waiting for a processor to email missing documents. No re-requesting items that were uploaded but saved in the wrong folder.

Cloud platforms also support rule-based automation for straightforward compliance checks, allowing underwriters to focus their expertise on the decisions that require judgment.

Closers and Post-Closing Teams

Closing teams see the final conditions, funding requirements, and document checklists in one view. Integration with title companies and e-signature platforms reduces the manual coordination that creates last-minute delays.

Security and Compliance in Cloud-Based LOS

Security is the first objection most mortgage executives raise about cloud systems. That objection made sense in 2010. It does not hold up in 2026.

Data encryption. Cloud LOS platforms encrypt data in transit (TLS 1.2+) and at rest (AES-256). This is stronger than the encryption on most on-premise servers running in mortgage company closets.

Role-based access control. Each user sees only the data their role requires. A loan officer cannot access underwriting decision notes. A processor cannot modify compliance settings. Access permissions are granular and auditable. We cover Using Loan Origination Software Encompass and Calyx for Mortgage Success in a companion piece.

Compliance monitoring. Built-in compliance engines track disclosure timing, TRID tolerances, and state-specific requirements automatically. When a deadline approaches, the system flags it before it becomes a violation.

Audit trails. Every action on every loan file is logged with a timestamp and user ID. Regulators can see exactly who did what, when. This audit trail is more reliable than manual logs because it cannot be altered after the fact.

What to Look for in a Cloud LOS Platform

The cloud LOS market includes platforms like Encompass by ICE Mortgage Technology, LendingPad, Calyx PointCentral, and MeridianLink Mortgage. Each has different strengths. Here is what matters most for collaboration.

Real-time multi-user editing. Can two people work on the same loan file simultaneously? LendingPad supports this natively. Encompass handles it through workflow routing.

Integration ecosystem. How many credit bureaus, appraisal vendors, and title companies connect directly? Encompass leads with 500+ marketplace integrations.

Compliance automation. Does the platform handle disclosure timing, QM calculations, and regulatory reporting? This is table stakes for mortgage companies.

Mobile access. Can loan officers access the system from a phone or tablet at a borrower's home? Browser-based platforms handle this. Desktop-installed platforms require workarounds.

IT partner support. Your LOS vendor handles the software. Your IT partner handles the infrastructure, security configuration, and integration with your broader technology stack. Mortgage Workspace provides managed IT services specifically for mortgage companies running cloud LOS platforms, covering everything from Microsoft 365 integration to endpoint security.

Talk to a Mortgage IT Specialist

Moving to a cloud-based LOS is a technology decision and an operations decision. Getting both right requires a partner who understands mortgage workflows as well as cloud infrastructure. Contact Mortgage Workspace to discuss your current LOS environment and what a cloud migration would look like for your team.

Frequently Asked Questions

Is Your Loan Origination Built for the Way Teams Work Now?

Cloud-based loan origination lets processors, underwriters, and loan officers collaborate on the same file in real time instead of trading versions. MortgageWorkspace modernizes your LOS so collaboration is the default, not the exception.

A cloud-based loan origination system is a mortgage processing platform hosted on remote servers and accessed through a web browser. Unlike desktop-installed LOS software, cloud platforms store loan data centrally, enable real-time collaboration across teams and locations, and update automatically without manual IT maintenance. Examples include Encompass, LendingPad, and MeridianLink Mortgage.

Cloud LOS improves collaboration by giving every team member access to the same loan file in real time. Processors, underwriters, and closers see the same data without waiting for email updates or manual handoffs. Automated workflow routing moves files between departments instantly, and built-in communication tools replace email threads with in-context messaging tied directly to each loan.

Modern cloud LOS platforms use encryption standards (TLS 1.2+ in transit, AES-256 at rest) that exceed what most on-premise mortgage servers provide. They include role-based access controls, automated compliance monitoring, and immutable audit trails that log every action with timestamps. Cloud platforms also receive security patches automatically, eliminating the delayed update cycles common with desktop installations.

A typical cloud LOS migration takes three to six months depending on data volume, the number of integrations, and staff training requirements. The process includes data migration, integration configuration with third-party vendors, security setup, user training, and parallel running of old and new systems. Working with an IT partner experienced in mortgage technology shortens the timeline and reduces the risk of disruption.